- Canada

- /

- Food and Staples Retail

- /

- TSX:NWC

Discovering Undiscovered Canadian Gems In October 2024

Reviewed by Simply Wall St

As the Canadian market rides a wave of optimism fueled by recent rate cuts and AI enthusiasm, the TSX has reached all-time highs, reflecting a broader trend of rising corporate earnings and economic expansion. In this buoyant environment, discovering stocks that align with these positive fundamentals can offer promising opportunities for investors seeking to uncover hidden gems in Canada.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Mandalay Resources | 11.86% | 9.48% | 37.58% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 15.28% | 7.58% | ★★★★★★ |

| Taiga Building Products | NA | 6.05% | 10.50% | ★★★★★★ |

| Westshore Terminals Investment | NA | -2.67% | -9.77% | ★★★★★☆ |

| Grown Rogue International | 24.92% | 43.35% | 67.95% | ★★★★★☆ |

| Mako Mining | 22.90% | 38.12% | 54.79% | ★★★★★☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

| Dundee | 5.93% | -38.65% | 39.44% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Hammond Power Solutions (TSX:HPS.A)

Simply Wall St Value Rating: ★★★★★★

Overview: Hammond Power Solutions Inc. designs, manufactures, and sells transformers across Canada, the United States, Mexico, and India with a market cap of CA$1.69 billion.

Operations: Hammond Power Solutions generates revenue primarily from the manufacture and sale of transformers, amounting to CA$754.37 million.

HPS, a Canadian power solutions player, has been making waves with its robust financial health and strategic moves. The company boasts more cash than total debt, and its debt-to-equity ratio impressively dropped from 27.7% to 5% over five years. Recent earnings show a net income of C$23.59 million for Q2 2024, up from C$13.33 million the previous year, indicating solid growth momentum. Additionally, HPS's earnings growth of 12.3% outpaced the Electrical industry average of 9.3%.

- Unlock comprehensive insights into our analysis of Hammond Power Solutions stock in this health report.

Learn about Hammond Power Solutions' historical performance.

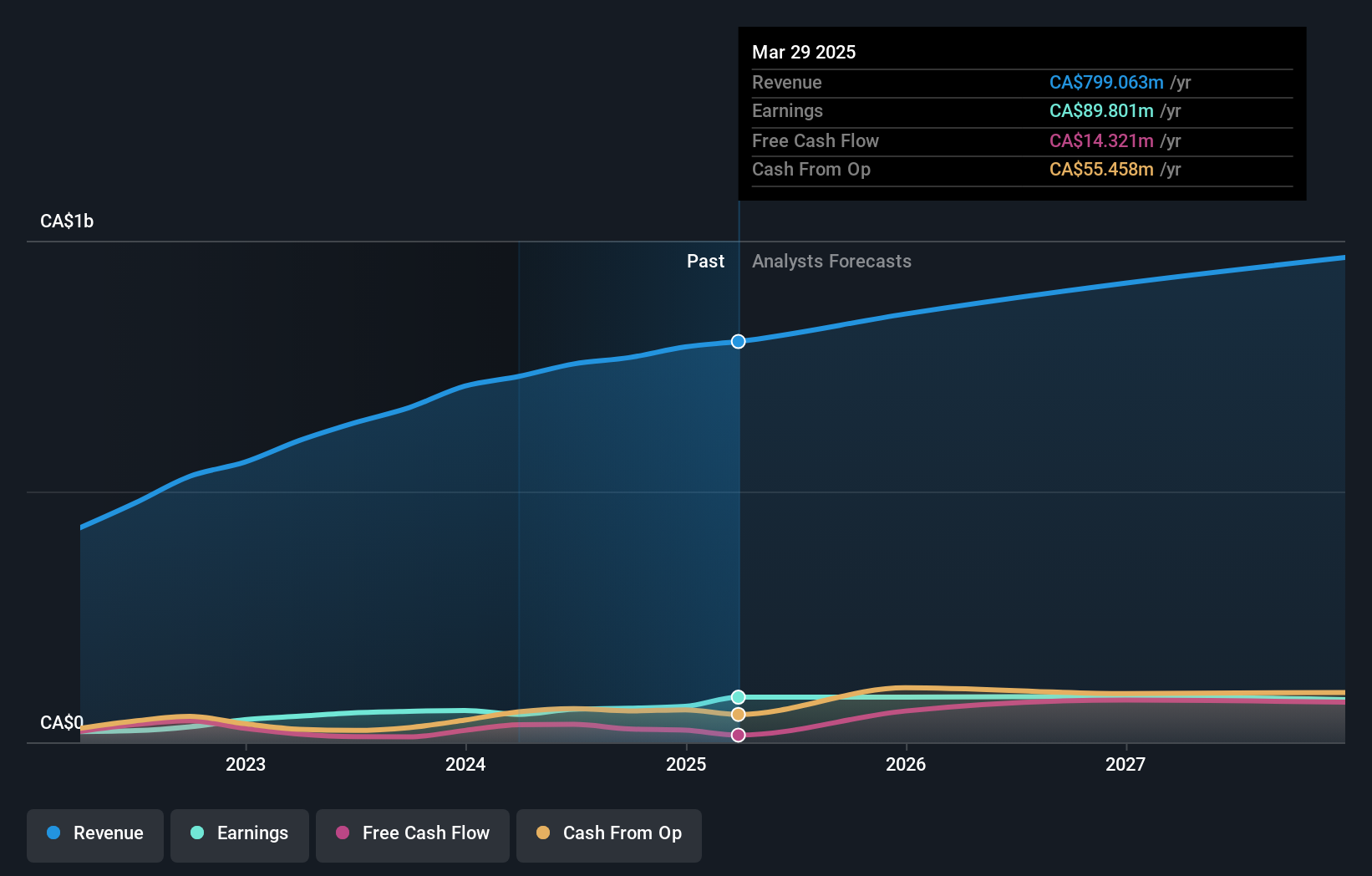

North West (TSX:NWC)

Simply Wall St Value Rating: ★★★★★★

Overview: The North West Company Inc. operates as a retailer of food and everyday products and services, catering to rural communities and urban neighborhood markets in northern Canada, rural Alaska, the South Pacific, and the Caribbean, with a market cap of CA$2.47 billion.

Operations: North West generates revenue primarily from the retail of food and everyday products and services, amounting to CA$2.52 billion.

North West, a Canadian retail company, shows promising attributes with its net debt to equity ratio at 31.4%, deemed satisfactory. Earnings grew by 9.5% over the past year, outpacing the industry average of -11.7%. Despite significant insider selling recently, North West trades at a value 44.5% below its estimated fair value. Recent earnings reports showed sales of C$646 million for Q2 2024 and an increased quarterly dividend of C$0.40 per share announced in September 2024.

- Take a closer look at North West's potential here in our health report.

Gain insights into North West's past trends and performance with our Past report.

TerraVest Industries (TSX:TVK)

Simply Wall St Value Rating: ★★★★★☆

Overview: TerraVest Industries Inc. is a company that manufactures and sells goods and services to energy, agriculture, mining, transportation, and other markets in Canada and the United States with a market cap of approximately CA$1.86 billion.

Operations: TerraVest Industries generates revenue primarily from its HVAC and Containment Equipment segment (CA$292.90 million) and Compressed Gas Equipment segment (CA$243.77 million). The Service segment also contributes significantly with CA$201.78 million, while Processing Equipment adds CA$117.58 million to the total revenue stream.

TerraVest Industries, a dynamic player in the energy services sector, recently saw its earnings soar by 43.6%, outpacing the industry's -6.7% performance. Trading at 22.7% below estimated fair value, it seems attractively priced for potential investors. Despite a high net debt to equity ratio of 42.3%, interest payments are well covered with EBIT at 5x coverage, and debt has decreased from 117.9% to 49.4% over five years, indicating improving financial health and stability in operations.

- Delve into the full analysis health report here for a deeper understanding of TerraVest Industries.

Evaluate TerraVest Industries' historical performance by accessing our past performance report.

Next Steps

- Unlock our comprehensive list of 48 TSX Undiscovered Gems With Strong Fundamentals by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if North West might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:NWC

North West

Through its subsidiaries, engages in the retail of food and everyday products and services to rural communities and urban neighborhood markets in northern Canada, rural Alaska, the South Pacific, and the Caribbean.

Flawless balance sheet with solid track record and pays a dividend.