Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:TNZ

Why Investors Shouldn't Be Surprised By Tenaz Energy Corp.'s (TSE:TNZ) 29% Share Price Surge

Tenaz Energy Corp. (TSE:TNZ) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. The annual gain comes to 281% following the latest surge, making investors sit up and take notice.

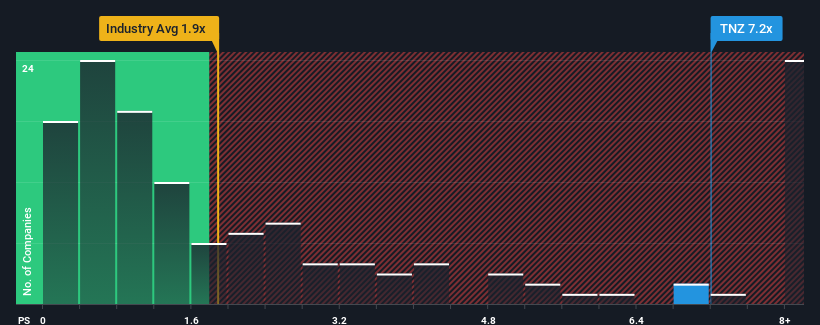

After such a large jump in price, given around half the companies in Canada's Oil and Gas industry have price-to-sales ratios (or "P/S") below 1.9x, you may consider Tenaz Energy as a stock to avoid entirely with its 7.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Tenaz Energy

How Tenaz Energy Has Been Performing

Tenaz Energy hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. Perhaps the market is expecting the poor revenue to reverse, justifying it's current high P/S.. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Tenaz Energy.How Is Tenaz Energy's Revenue Growth Trending?

Tenaz Energy's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 3.8%. Even so, admirably revenue has lifted 266% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 90% per year over the next three years. With the industry only predicted to deliver 2.4% per year, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Tenaz Energy's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What Does Tenaz Energy's P/S Mean For Investors?

Tenaz Energy's P/S has grown nicely over the last month thanks to a handy boost in the share price. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our look into Tenaz Energy shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Tenaz Energy with six simple checks.

If these risks are making you reconsider your opinion on Tenaz Energy, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Tenaz Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:TNZ

Tenaz Energy

An energy company, engages in the acquisition and development of oil and gas properties in Canada and the Netherlands.

Undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor