Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies. Paramount Resources Ltd. (TSE:POU) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Paramount Resources

What Is Paramount Resources's Debt?

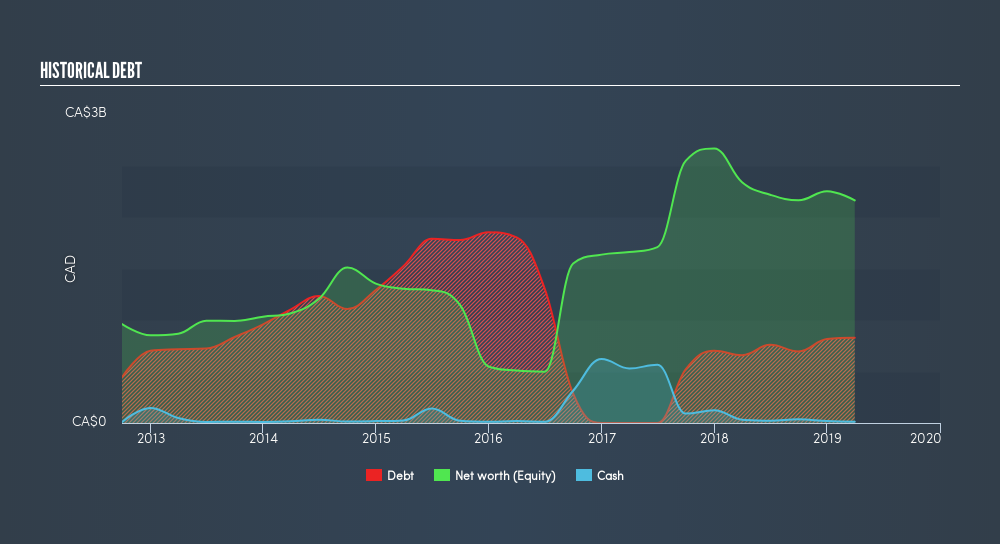

The image below, which you can click on for greater detail, shows that at March 2019 Paramount Resources had debt of CA$827.3m, up from CA$658.0m in one year. And it doesn't have much cash, so its net debt is about the same.

A Look At Paramount Resources's Liabilities

Zooming in on the latest balance sheet data, we can see that Paramount Resources had liabilities of CA$294.0m due within 12 months and liabilities of CA$1.65b due beyond that. Offsetting this, it had CA$12.9m in cash and CA$126.2m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CA$1.81b.

The deficiency here weighs heavily on the CA$836.5m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Paramount Resources would likely require a major re-capitalisation if it had to pay its creditors today. Either way, since Paramount Resources does have more debt than cash, it's worth keeping an eye on its balance sheet. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Paramount Resources's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Paramount Resources managed to grow its revenue by 31%, to CA$873m. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Even though Paramount Resources managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. Its EBIT loss was a whopping CA$580m. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of CA$322m over the last twelve months. That means it's on the risky side of things. For riskier companies like Paramount Resources I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:POU

Paramount Resources

An energy company, explores for and develops conventional and unconventional petroleum and natural gas reserves and resources in Canada.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor