Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:PEY

Don't Race Out To Buy Peyto Exploration & Development Corp. (TSE:PEY) Just Because It's Going Ex-Dividend

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

It looks like Peyto Exploration & Development Corp. (TSE:PEY) is about to go ex-dividend in the next 2 days. Investors can purchase shares before the 27th of June in order to be eligible for this dividend, which will be paid on the 15th of July.

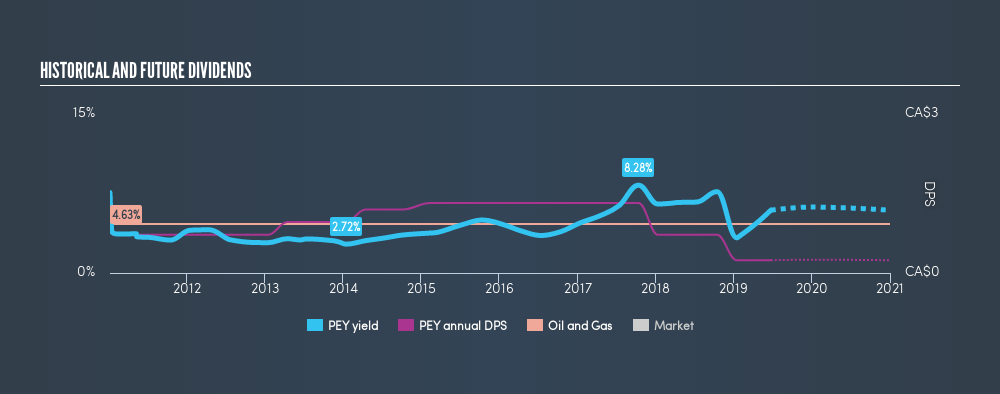

Peyto Exploration & Development's next dividend payment will be CA$0.02 per share. Last year, in total, the company distributed CA$0.24 to shareholders. Looking at the last 12 months of distributions, Peyto Exploration & Development has a trailing yield of approximately 5.9% on its current stock price of CA$4.05. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. As a result, readers should always check whether Peyto Exploration & Development has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for Peyto Exploration & Development

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Last year, Peyto Exploration & Development paid out 93% of its income as dividends, which is above a level that we're comfortable with, especially if the company needs to reinvest in its business. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Over the last year it paid out 63% of its free cash flow as dividends, within the usual range for most companies.

It's good to see that while Peyto Exploration & Development's dividends were not well covered by profits, at least they are affordable from a cash perspective. Still, if this were to happen repeatedly, we'd be concerned about whether the dividend is sustainable in a downturn.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings fall far enough, the company could be forced to cut its dividend. Readers will understand then, why we're concerned to see Peyto Exploration & Development's earnings per share have dropped 7.6% a year over the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Peyto Exploration & Development's dividend payments per share have declined at 20% per year on average over the past 8 years, which is uninspiring. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

The Bottom Line

Has Peyto Exploration & Development got what it takes to maintain its dividend payments? It's never fun to see a company's earnings per share in retreat. Worse, Peyto Exploration & Development's paying out a majority of its earnings and more than half its free cash flow. Positive cash flows are good news but it's not a good combination. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Curious what other investors think of Peyto Exploration & Development? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow .

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:PEY

Peyto Exploration & Development

Engages in the exploration, development, and production of natural gas, oil, and natural gas liquids in Alberta’s deep basin.

Good value average dividend payer.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor