Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:FRU

Freehold Royalties (TSX:FRU): Evaluating Valuation After Strong Q3 2025 Results and U.S. Growth Momentum

Simply Wall St

Reviewed by Simply Wall St

Freehold Royalties (TSX:FRU) just posted its third quarter 2025 results, showing higher net income compared to last year. The boost comes largely from increased U.S. production, strategic acquisitions, and operational efficiencies.

See our latest analysis for Freehold Royalties.

Freehold Royalties’ latest financials gave momentum to the share price, which climbed nearly 10% in the past month and is now up 13.8% year-to-date. The total shareholder return has been steady as well, with a 14.6% gain over the past year and an impressive 332% over five years. This reflects durable performance as growth from U.S. assets and portfolio diversification continue to pay off.

If you’re looking for your next discovery beyond Freehold's recent surge, now is an ideal time to broaden your horizons and explore fast growing stocks with high insider ownership

But with shares trading close to analyst price targets and a multi-year run already behind it, investors now face a key question: is Freehold still undervalued, or has the market already priced in future growth?

Price-to-Earnings of 18.9x: Is it justified?

Freehold Royalties is trading at a price-to-earnings (P/E) ratio of 18.9x, based on the last close of CA$14.88. This valuation reflects investor expectations for sustained earnings power. How does it stack up against competitors?

The P/E ratio measures how much investors are willing to pay per dollar of current earnings. For an oil and gas royalty company like Freehold, this multiple signals confidence in the business model’s ability to generate stable profits, even during periods of sector volatility. A higher multiple may indicate that the market expects reliable cash flow or significant future growth potential, while a lower one can suggest caution or sector headwinds.

Compared to the Canadian Oil and Gas industry average of 14.7x, Freehold's 18.9x P/E appears elevated. However, it is attractively valued relative to a peer group average of 32.9x, indicating the stock is neither a bargain nor priced at an extreme premium, especially if Freehold’s diversified portfolio and U.S. expansion support its performance against rivals.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 18.9x (ABOUT RIGHT)

However, revenue growth has recently stalled. Any sustained slowdown or unexpected sector weakness could challenge further upside for Freehold shares.

Find out about the key risks to this Freehold Royalties narrative.

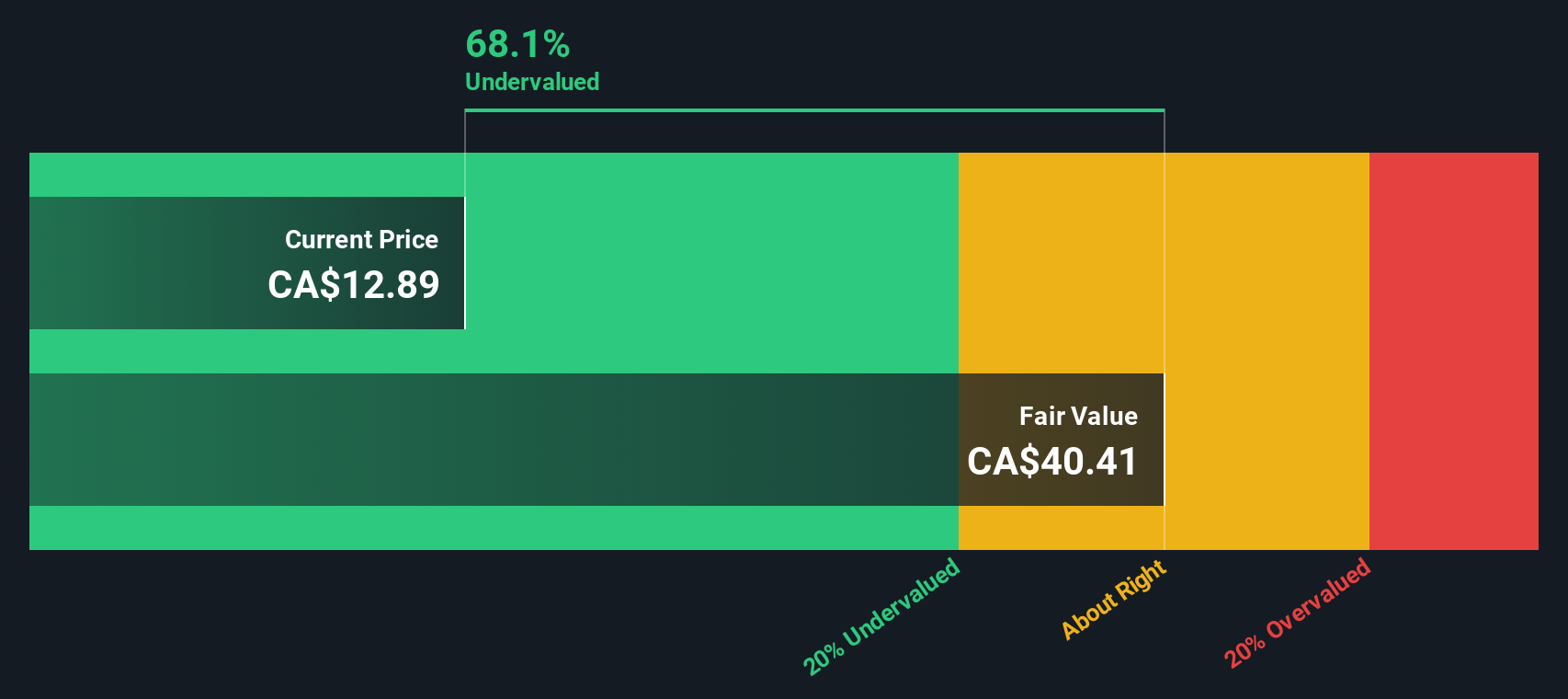

Another Perspective: Deep Discount to Fair Value

Looking at the SWS DCF model, Freehold Royalties appears significantly undervalued by the market. With shares trading at CA$14.88, our DCF estimate of fair value is CA$42.46, showing a steep 65% difference. Could this signal untapped upside, or is the gap a sign of caution?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Freehold Royalties for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 897 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Freehold Royalties Narrative

If you want to dive deeper, challenge today’s outlook, or build your own view from the numbers, it only takes a few minutes to explore and Do it your way

A great starting point for your Freehold Royalties research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors never stop seeking opportunity. With the right tools, you could be tapping into the stocks fueling tomorrow’s growth stories and income streams right now.

- Capitalize on strong cash flows and attractive entry points by checking out these 897 undervalued stocks based on cash flows that could be poised for a breakout.

- Supercharge your portfolio’s future relevance and gain an edge by targeting the market leaders among these 27 AI penny stocks, which are set to transform industries.

- Build wealth through reliable payouts when you start searching these 18 dividend stocks with yields > 3% and pick companies with dividend yields over 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:FRU

Freehold Royalties

Acquires and manages royalty interests in the crude oil, natural gas, natural gas liquids, and potash properties in Canada and the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor