Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:ENB

Enbridge Inc.'s (TSE:ENB) Business Is Yet to Catch Up With Its Share Price

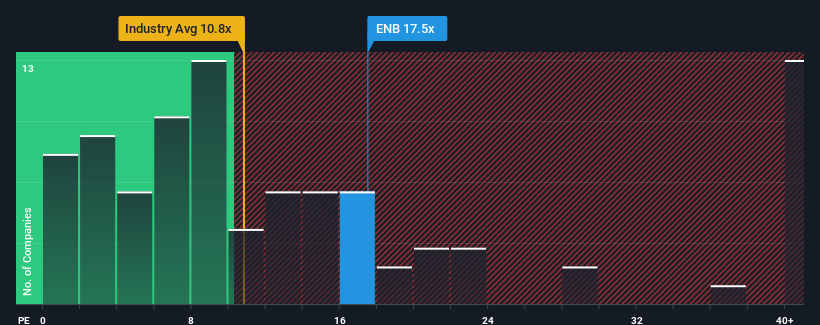

With a price-to-earnings (or "P/E") ratio of 17.5x Enbridge Inc. (TSE:ENB) may be sending bearish signals at the moment, given that almost half of all companies in Canada have P/E ratios under 14x and even P/E's lower than 7x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Recent times have been pleasing for Enbridge as its earnings have risen in spite of the market's earnings going into reverse. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

Check out our latest analysis for Enbridge

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as high as Enbridge's is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 122% gain to the company's bottom line. Pleasingly, EPS has also lifted 86% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 6.2% per annum during the coming three years according to the twelve analysts following the company. That's shaping up to be materially lower than the 8.6% per year growth forecast for the broader market.

With this information, we find it concerning that Enbridge is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Bottom Line On Enbridge's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Enbridge currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Enbridge (1 is significant!) that you should be aware of before investing here.

You might be able to find a better investment than Enbridge. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Enbridge might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:ENB

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|65.7% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.9% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.4% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.0% undervalued

AN

Based on Analyst Price Targets