Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:EFR

Is Energy Fuels Inc.'s (TSE:EFR) Balance Sheet Strong Enough To Weather A Storm?

While small-cap stocks, such as Energy Fuels Inc. (TSE:EFR) with its market cap of CA$353m, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Companies operating in the Oil and Gas industry, especially ones that are currently loss-making, are more likely to be higher risk. So, understanding the company's financial health becomes vital. Here are a few basic checks that are good enough to have a broad overview of the company’s financial strength. However, I know these factors are very high-level, so I’d encourage you to dig deeper yourself into EFR here.

Does EFR produce enough cash relative to debt?

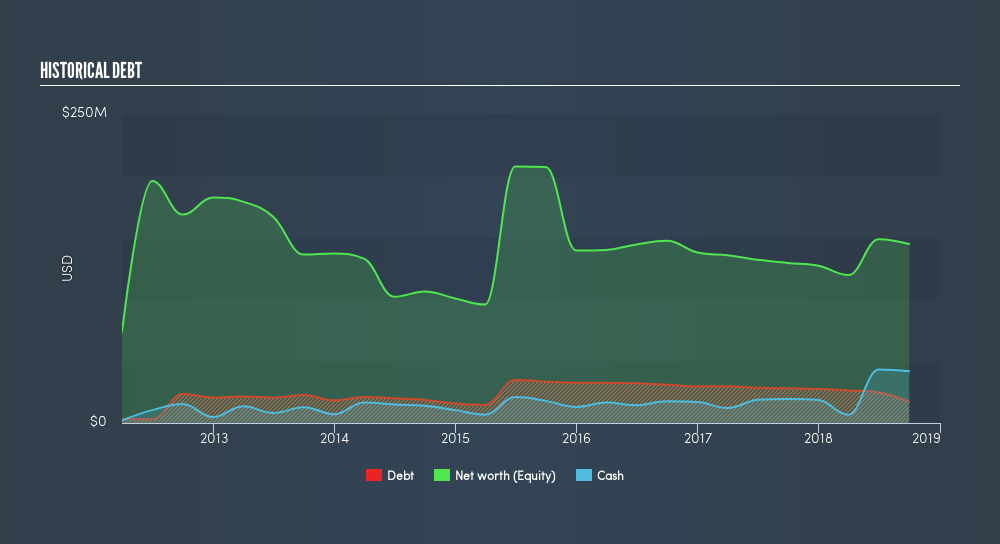

EFR has shrunken its total debt levels in the last twelve months, from US$28m to US$17m , which includes long-term debt. With this debt payback, EFR currently has US$42m remaining in cash and short-term investments for investing into the business. Moving onto cash from operations, its trivial cash flows from operations make the cash-to-debt ratio less useful to us, though these low levels of cash means that operational efficiency is worth a look. For this article’s sake, I won’t be looking at this today, but you can take a look at some of EFR’s operating efficiency ratios such as ROA here.

Does EFR’s liquid assets cover its short-term commitments?

At the current liabilities level of US$8.0m, it seems that the business has been able to meet these commitments with a current assets level of US$59m, leading to a 7.42x current account ratio. Having said that, a ratio above 3x may be considered excessive by some investors.

Is EFR’s debt level acceptable?

EFR’s level of debt is appropriate relative to its total equity, at 12%. EFR is not taking on too much debt commitment, which may be constraining for future growth. Investors' risk associated with debt is very low with EFR, and the company has plenty of headroom and ability to raise debt should it need to in the future.

Next Steps:

EFR’s high cash coverage and low debt levels indicate its ability to utilise its borrowings efficiently in order to generate ample cash flow. In addition to this, the company will be able to pay all of its upcoming liabilities from its current short-term assets. This is only a rough assessment of financial health, and I'm sure EFR has company-specific issues impacting its capital structure decisions. You should continue to research Energy Fuels to get a better picture of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for EFR’s future growth? Take a look at our free research report of analyst consensus for EFR’s outlook.

- Valuation: What is EFR worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether EFR is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:EFR

Energy Fuels

Engages in the exploration, recovery, recycling, exploration, operation, development, permitting, evaluation, and sale of uranium mineral properties in the United States.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor