- Canada

- /

- Oil and Gas

- /

- TSX:CVE

Does Cenovus Energy's (TSX:CVE) MEG-Driven 2026 Output Plan Reframe Its Margin Priorities?

Reviewed by Sasha Jovanovic

- Cenovus Energy recently issued fourth-quarter 2025 and full-year 2026 guidance, projecting upstream production of 910,000–920,000 BOE/d in late 2025 and 945,000–985,000 BOE/d in 2026, alongside downstream crude throughput of 430,000–450,000 bbls/d and about US$80 million of MEG-related transaction expenses.

- The company also plans to accelerate certain one-time benefits from the MEG acquisition into 2025, while an options trading surge in its stock highlights increased investor focus on how this guidance could shape future margins and capital allocation.

- We’ll now examine how Cenovus’s higher 2026 production guidance, following the MEG acquisition, may influence its existing investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Cenovus Energy Investment Narrative Recap

To own Cenovus, you need to be comfortable with a long-term, heavy-oil and integrated refining story where large, capital-intensive projects and Canadian regulation are central. The latest 2025–2026 guidance does not fundamentally change that, but it does bring near-term attention to how efficiently Cenovus can turn higher post-MEG production into stronger margins while managing the risk that ongoing high capital spending squeezes free cash flow.

The most relevant update here is Cenovus’s 2026 capital plan of US$5.0 billion to US$5.3 billion, alongside its reaffirmed US$4 billion net debt target. This sits directly beside the new, higher production guidance and MEG-related integration costs, giving investors a clearer line of sight on how the company intends to balance growth projects, balance sheet priorities, and shareholder returns over the next couple of years.

Yet even with higher production planned, investors should be aware that sustained high capital spending on oil sands and offshore projects could...

Read the full narrative on Cenovus Energy (it's free!)

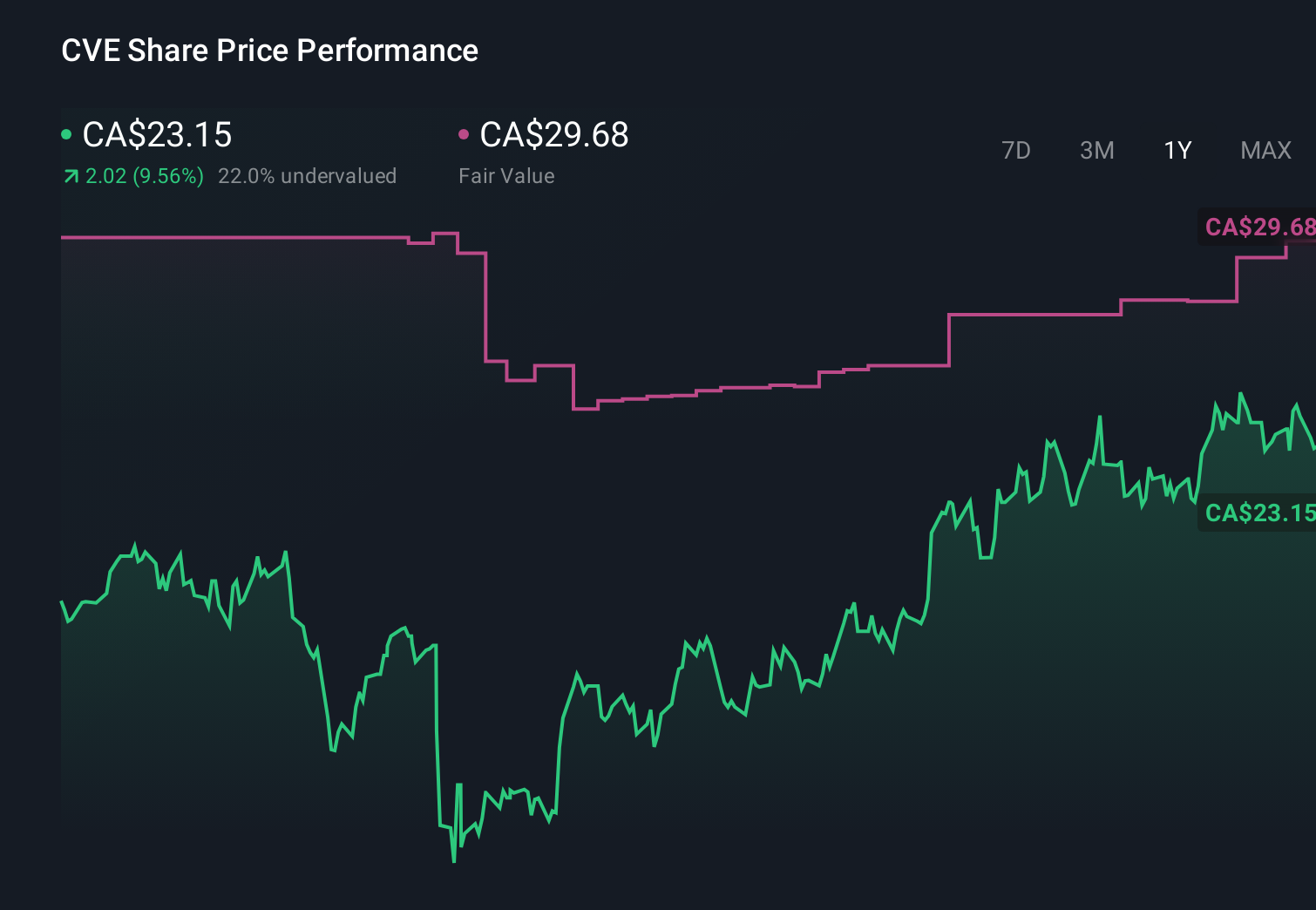

Cenovus Energy's narrative projects CA$59.0 billion revenue and CA$3.9 billion earnings by 2028. This requires 4.1% yearly revenue growth and about CA$1.3 billion earnings increase from CA$2.6 billion today.

Uncover how Cenovus Energy's forecasts yield a CA$29.68 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Six fair value views from the Simply Wall St Community span roughly CA$24 to CA$77.62 per share, showing how differently investors are thinking about Cenovus today. Set against this, the company’s sizable ongoing capital commitments to oil sands and offshore growth projects raise important questions about future cash flow flexibility and earnings resilience that are worth comparing across these perspectives.

Explore 6 other fair value estimates on Cenovus Energy - why the stock might be worth just CA$24.00!

Build Your Own Cenovus Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cenovus Energy research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Cenovus Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cenovus Energy's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CVE

Cenovus Energy

Develops, produces, refines, transports, and markets crude oil, natural gas, and refined petroleum products in Canada, the United States, and China.

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion