Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:BTE

New Forecasts: Here's What Analysts Think The Future Holds For Baytex Energy Corp. (TSE:BTE)

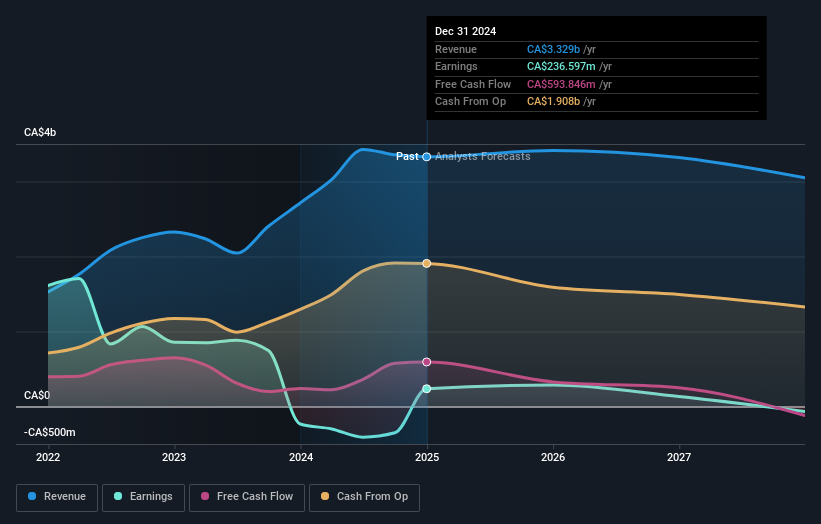

Shareholders in Baytex Energy Corp. (TSE:BTE) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The revenue forecast for this year has experienced a facelift, with analysts now much more optimistic on its sales pipeline.

Following the upgrade, the current consensus from Baytex Energy's five analysts is for revenues of CA$3.8b in 2025 which - if met - would reflect a decent 13% increase on its sales over the past 12 months. Prior to the latest estimates, the analysts were forecasting revenues of CA$3.4b in 2025. It looks like there's been a clear increase in optimism around Baytex Energy, given the decent improvement in revenue forecasts.

See our latest analysis for Baytex Energy

Notably, the analysts have cut their price target 8.6% to CA$4.00, suggesting concerns around Baytex Energy's valuation.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's pretty clear that there is an expectation that Baytex Energy's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 18% growth on an annualised basis. This is compared to a historical growth rate of 25% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 3.1% annually. So it's pretty clear that, while Baytex Energy's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away from this upgrade is that analysts lifted their revenue estimates for this year. Analysts also expect revenues to grow faster than the wider market. Furthermore, there was a cut to the price target, suggesting that the latest news has led to more pessimism about the intrinsic value of the business. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Baytex Energy.

Analysts are definitely bullish on Baytex Energy, but no company is perfect. Indeed, you should know that there are several potential concerns to be aware of, including a weak balance sheet. For more information, you can click through to our platform to learn more about this and the 3 other risks we've identified .

You can also see our analysis of Baytex Energy's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

Valuation is complex, but we're here to simplify it.

Discover if Baytex Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:BTE

Baytex Energy

An energy company, engages in the acquisition, development, and production of crude oil and natural gas in the Western Canadian Sedimentary Basin and in the Eagle Ford, the United States.

Acceptable track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor