Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:BIR

Birchcliff Energy (TSX:BIR) Valuation in Focus Following Share Buyback Authorization

Simply Wall St

Reviewed by Simply Wall St

Birchcliff Energy (TSX:BIR) just announced that its Board has authorized a share buyback plan. The company aims to repurchase up to 10% of its outstanding shares over the next year. This move highlights management's confidence and could increase shareholder value.

See our latest analysis for Birchcliff Energy.

The share buyback announcement follows a period of strong momentum for Birchcliff Energy, with the stock delivering a notable 20% share price return over the past month and a year-to-date gain of 42%. Over the past year, total shareholder return is 54%, reflecting a wave of optimism and renewed belief in the company’s longer-term growth, although the three-year total return remains slightly negative.

If you’re interested in spotting other companies with significant upside, this could be the right moment to expand your search and discover fast growing stocks with high insider ownership

With shares rebounding strongly and management signaling their optimism, the big question remains: is Birchcliff Energy’s recent rally supported by underlying value, or is the market already pricing in all its future growth potential?

Price-to-Earnings of 29.5x: Is it justified?

Birchcliff Energy’s shares are trading at a Price-to-Earnings (P/E) ratio of 29.5x, which suggests investors are paying a premium compared to both its historical trends and similar peers in the Canadian energy space.

The Price-to-Earnings ratio measures how much investors are willing to pay for each dollar of current earnings. For Birchcliff, a P/E of 29.5x reflects confidence in future profitability, especially following a period of substantial earnings growth. This ratio is a useful yardstick for investors to compare valuation across companies and sectors, particularly in industries where earnings are a key driver of value.

BIR’s 29.5x P/E ratio appears reasonable when compared to its fair P/E estimate of 43.5x, indicating the stock may still be undervalued based on this metric. When compared to its direct peers, which trade at an average of 31.7x, Birchcliff is slightly cheaper. However, relative to the broader Canadian Oil and Gas industry’s average of 14.9x, BIR looks quite expensive. This may indicate that the market is expecting stronger growth or is assigning a premium for its quality of earnings and management tenure. The current P/E remains well below the fair value suggested by regression analysis, which could be a reference point the market eventually gravitates toward.

Explore the SWS fair ratio for Birchcliff Energy

Result: Price-to-Earnings of 29.5x (UNDERVALUED)

However, sustained earnings growth is not guaranteed. Fluctuations in energy prices or operational challenges could quickly dampen the current optimism.

Find out about the key risks to this Birchcliff Energy narrative.

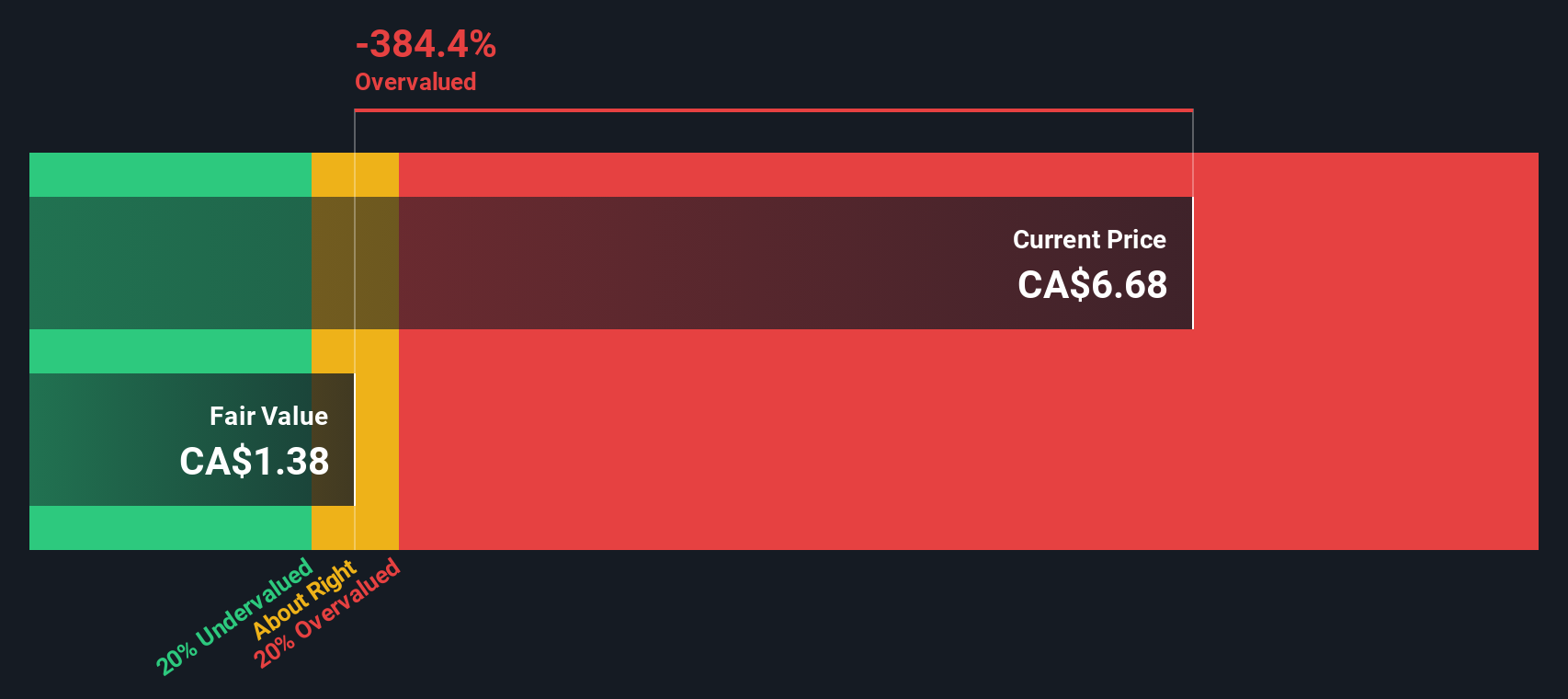

Another View: What Does Our DCF Model Suggest?

Switching from an earnings-based valuation to our SWS DCF model provides a different perspective. By estimating the future cash flows Birchcliff could generate, our DCF model currently suggests the shares trade at a significant 51% discount to fair value. This indicates a deeper undervaluation than the P/E ratio implies, but no model is perfect. Can investors rely on these assumptions?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Birchcliff Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Birchcliff Energy Narrative

If you have a different perspective on what the numbers mean or want to explore the data in your own way, you can easily build your personal view in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Birchcliff Energy.

Looking for more investment ideas?

Don’t let your next big opportunity slip by. The Simply Wall Street Screener uncovers trends and stocks that others often overlook. This helps you always stay a step ahead.

- Capture potential market upswings when you find these 914 undervalued stocks based on cash flows offering solid value based on real cash flow analysis and smart fundamentals.

- Boost your income strategy by targeting these 15 dividend stocks with yields > 3% built for steady returns and attractive yields above 3%.

- Get ahead of innovation by tapping into these 25 AI penny stocks at the forefront of artificial intelligence and shaping tomorrow’s industries today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Birchcliff Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:BIR

Birchcliff Energy

An intermediate oil and natural gas company, engages in the exploration, development, and production of natural gas, light oil, condensate, and other natural gas liquids in Western Canada.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative