Advertisement

- Canada

- /

- Capital Markets

- /

- TSXV:NFD.A

Why Investors Shouldn't Be Surprised By Northfield Capital Corporation's (CVE:NFD.A) 26% Share Price Surge

Despite an already strong run, Northfield Capital Corporation (CVE:NFD.A) shares have been powering on, with a gain of 26% in the last thirty days. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

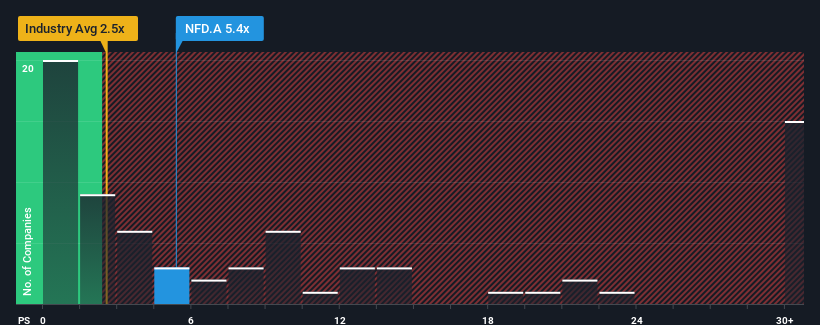

Following the firm bounce in price, given around half the companies in Canada's Capital Markets industry have price-to-sales ratios (or "P/S") below 2.5x, you may consider Northfield Capital as a stock to avoid entirely with its 5.4x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Northfield Capital

What Does Northfield Capital's P/S Mean For Shareholders?

With revenue growth that's exceedingly strong of late, Northfield Capital has been doing very well. Perhaps the market is expecting future revenue performance to outperform the wider market, which has seemingly got people interested in the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Northfield Capital's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Northfield Capital?

Northfield Capital's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 77%. Still, revenue has fallen 23% in total from three years ago, which is quite disappointing. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

This is in contrast to the rest of the industry, which is expected to decline by 69% over the next year, even worse than the company's recent medium-term annualised revenue decline.

With this information, it might not be hard to see why Northfield Capital is trading at a higher P/S in comparison. Nonetheless, there's no guarantee the P/S has found a floor yet with recent revenue going backwards, despite the industry heading down even harder. There is potential for the P/S to fall to lower levels if the company doesn't improve its top-line growth, which would be difficult to do with the current industry outlook.

The Bottom Line On Northfield Capital's P/S

The strong share price surge has lead to Northfield Capital's P/S soaring as well. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Despite experiencing declining revenues, Northfield Capital has been able to maintain its high P/S off the back of its recentthree-year revenue not being as bad as the forecasts for a struggling industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident revenue aren't under any additional threat. We still remain cautious about the company's ability to stay its recent course and avoid revenues slipping in line with the industry. Although, if the company's relative outperformance doesn't change it will continue to provide strong support to the share price.

You need to take note of risks, for example - Northfield Capital has 4 warning signs (and 2 which don't sit too well with us) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Northfield Capital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:NFD.A

Adequate balance sheet low.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor