Sprott (TSX:SII) just made waves with the introduction of its Sprott Active Metals & Miners ETF, an actively managed fund aimed directly at the heart of the metals and mining sector. This launch is more than just a new product on the shelf; it signals Sprott's strategy to focus on a high-demand part of the market and put its experienced team to work identifying undervalued opportunities. For investors weighing their next move, this new ETF highlights Sprott's evolving approach to capturing growth from strategic metals, an area receiving more investor attention as global demand rises.

So how has all this played out in Sprott's stock price? Digging into recent performance, Sprott’s shares have seen strong upward momentum, climbing over 80% in the past year with an especially sharp rise of more than 52% since January. That rally picked up steam over the past three months as well. While Sprott launched a few other products this year, the ETF announcement stands out for how it deepens the company’s footprint in metals investing.

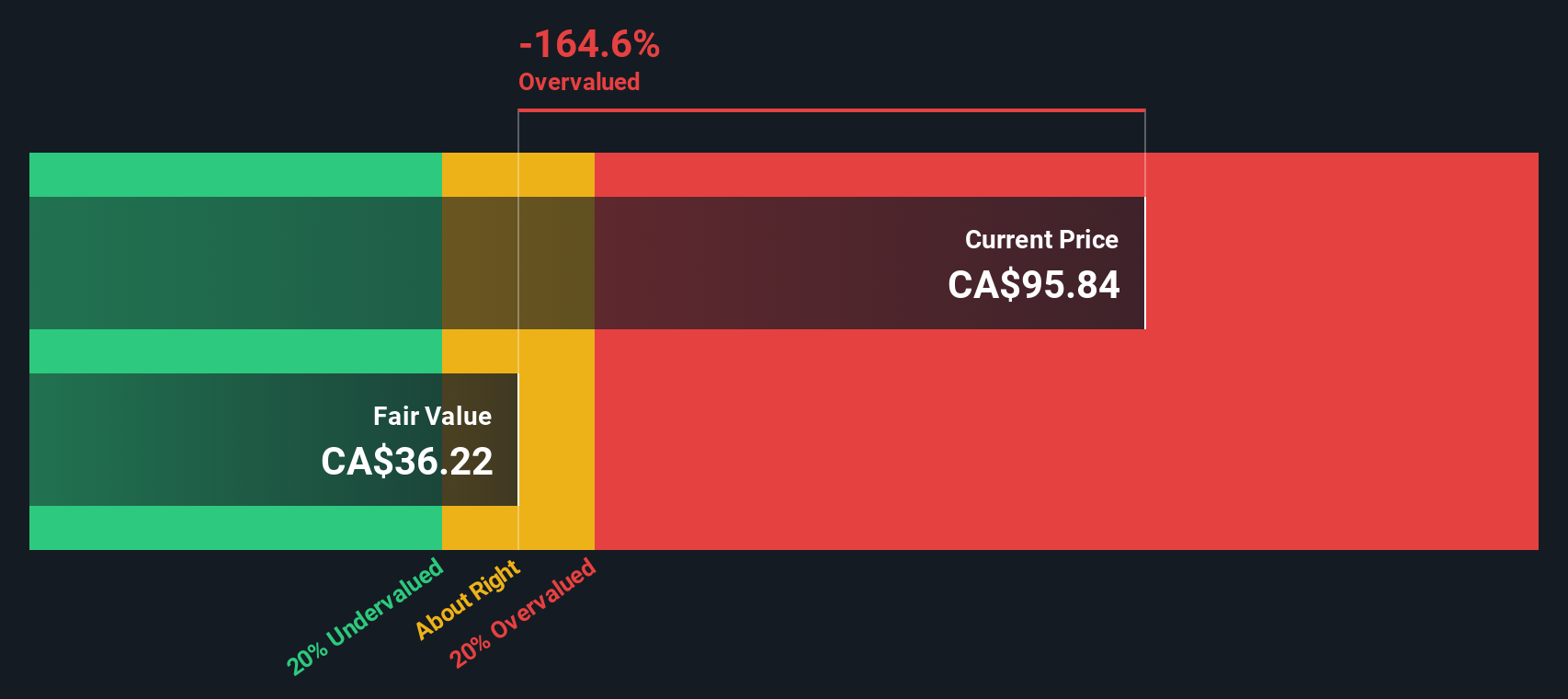

After such a surge, the big question remains: Does the current price reflect all the growth excitement, or is there more value left for patient investors to uncover?

Advertisement

Price-to-Earnings of 35.7x: Is it justified?

Sprott's current Price-To-Earnings (P/E) ratio of 35.7 times earnings positions the stock as expensive compared to both the Canadian Capital Markets industry average of 10.3x and the average among its peers at 16.6x. This suggests that the market is placing a significant premium on Sprott’s future earnings potential or growth prospects, relative to similar companies.

The P/E ratio is a widely used valuation metric that indicates how much investors are willing to pay today for a dollar of the company’s earnings. In capital markets, a higher P/E can reflect strong confidence in a company’s ability to grow earnings, but it can also signal overvaluation if growth expectations do not materialize.

Sprott’s high P/E, especially compared to the broader industry, suggests that investors expect robust profit growth or see the company as less risky than its peers. However, if the firm cannot deliver on these expectations, the stock’s valuation may be difficult to justify over the long term.

However, if Sprott's revenue growth slows or metals markets cool, investor optimism could fade. This could put downward pressure on the stock’s current valuation.

Looking at Sprott through our DCF model, we reach a similar conclusion as with the multiple approach. The current share price sits above its calculated fair value. Could both methods be missing something about future growth?

If you have a different perspective or want to dig into the numbers yourself, you can shape your own view in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Sprott.

Looking for more investment ideas?

Don’t limit your potential to just one opportunity. Give yourself an edge by finding companies with strong growth, yield, or innovation using these powerful tools:

Uncover high-potential disruptors in AI by checking out AI penny stocks. These companies are transforming industries with smart technologies and breakthrough automation.

Tap into the next wave of healthy returns by seeking out healthcare AI stocks and explore which pioneers are revolutionizing medicine with artificial intelligence.

Boost your income with reliable dividend stocks with yields > 3%. These options deliver yields higher than 3 percent while maintaining financial stability and long-term growth prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks