Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Empire Company Limited (TSE:EMP.A) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out the opportunities and risks within the CA Consumer Retailing industry.

How Much Debt Does Empire Carry?

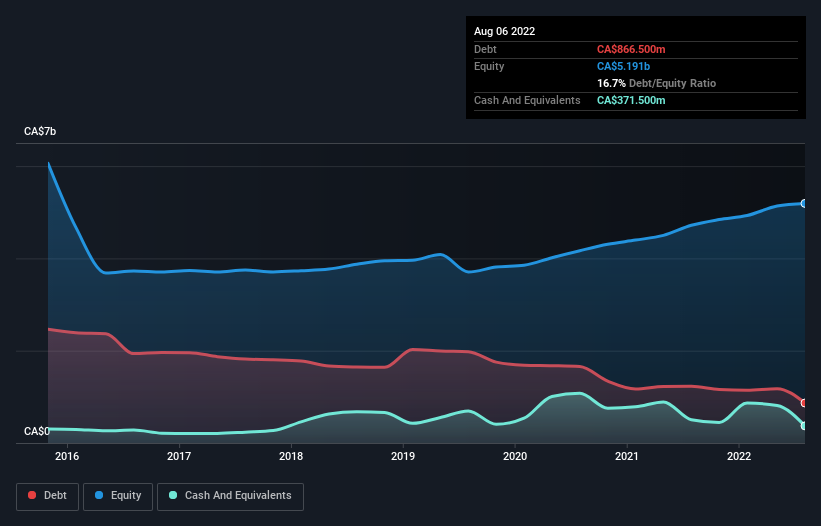

The image below, which you can click on for greater detail, shows that Empire had debt of CA$866.5m at the end of August 2022, a reduction from CA$1.23b over a year. On the flip side, it has CA$371.5m in cash leading to net debt of about CA$495.0m.

How Healthy Is Empire's Balance Sheet?

The latest balance sheet data shows that Empire had liabilities of CA$3.89b due within a year, and liabilities of CA$7.22b falling due after that. Offsetting these obligations, it had cash of CA$371.5m as well as receivables valued at CA$763.7m due within 12 months. So its liabilities total CA$9.98b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company's CA$9.26b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Empire's low debt to EBITDA ratio of 0.27 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 5.0 times last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. We saw Empire grow its EBIT by 7.7% in the last twelve months. That's far from incredible but it is a good thing, when it comes to paying off debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Empire's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Empire actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Empire's conversion of EBIT to free cash flow was a real positive on this analysis, as was its net debt to EBITDA. On the other hand, its level of total liabilities makes us a little less comfortable about its debt. When we consider all the factors mentioned above, we do feel a bit cautious about Empire's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Empire insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Empire might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:EMP.A

Empire

Engages in the food retail and related real estate businesses in Canada.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Community Narratives