Advertisement

AtkinsRéalis Group And 2 Other TSX Stocks Conceivably Priced Below Intrinsic Value Estimates

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market navigates a period of economic adjustment, with inflationary pressures easing and interest rates potentially on the decline, investors are keenly observing opportunities that may arise from these shifting conditions. In this environment, identifying stocks that are priced below their intrinsic value can be particularly rewarding, as they offer potential for growth when market conditions stabilize.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Savaria (TSX:SIS) | CA$16.53 | CA$30.37 | 45.6% |

| Docebo (TSX:DCBO) | CA$44.29 | CA$85.17 | 48% |

| Thunderbird Entertainment Group (TSXV:TBRD) | CA$1.65 | CA$3.26 | 49.4% |

| Groupe Dynamite (TSX:GRGD) | CA$14.29 | CA$27.63 | 48.3% |

| Lithium Royalty (TSX:LIRC) | CA$5.10 | CA$9.19 | 44.5% |

| Tourmaline Oil (TSX:TOU) | CA$68.85 | CA$136.58 | 49.6% |

| Kits Eyecare (TSX:KITS) | CA$12.42 | CA$24.64 | 49.6% |

| Aya Gold & Silver (TSX:AYA) | CA$12.82 | CA$25.01 | 48.7% |

| Wishpond Technologies (TSXV:WISH) | CA$0.285 | CA$0.56 | 48.7% |

| Electrovaya (TSX:ELVA) | CA$3.51 | CA$5.90 | 40.5% |

Here's a peek at a few of the choices from the screener.

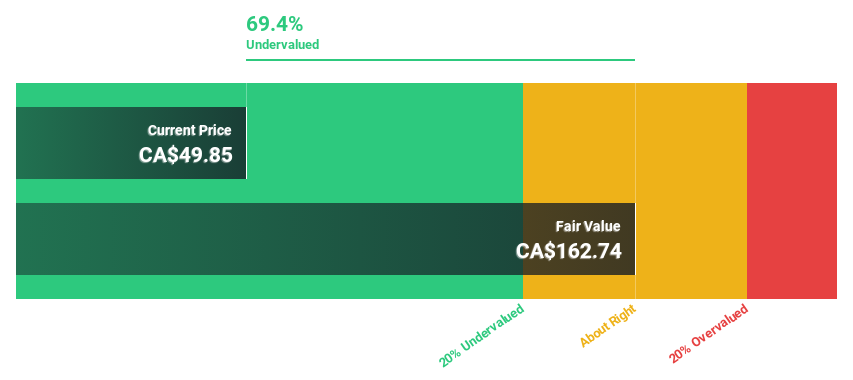

AtkinsRéalis Group (TSX:ATRL)

Overview: AtkinsRéalis Group Inc. offers professional services, project management, and capital investment services across the United Kingdom, Canada, the United States, Saudi Arabia, and internationally with a market cap of CA$12.38 billion.

Operations: The company's revenue is primarily derived from Engineering Services in the UKI (CA$2.48 billion), USLA (CA$1.71 billion), AMEA (CA$1.32 billion), and Canada (CA$1.46 billion) regions, along with contributions from Nuclear services (CA$1.49 billion), Linxon (CA$835.68 million), Capital investments (CA$126.06 million), and LSTK Projects (CA$249.37 million).

Estimated Discount To Fair Value: 32.8%

AtkinsRéalis Group is trading at CA$70.04, significantly below its estimated fair value of CA$104.23, indicating potential undervaluation based on cash flows. Earnings are projected to grow 21.8% annually, outpacing the Canadian market's growth rate. Recent contracts, including a high-speed rail project in Canada and infrastructure work in Puerto Rico, bolster its revenue prospects and operational footprint despite a modest net income decline last year to CA$283.87 million from CA$287.21 million.

- Our growth report here indicates AtkinsRéalis Group may be poised for an improving outlook.

- Unlock comprehensive insights into our analysis of AtkinsRéalis Group stock in this financial health report.

BRP (TSX:DOO)

Overview: BRP Inc. is a company that designs, develops, manufactures, distributes, and markets powersports vehicles and marine products globally, with a market cap of approximately CA$3.98 billion.

Operations: BRP Inc.'s revenue is primarily generated from the design, development, manufacturing, distribution, and marketing of powersports vehicles and marine products across various international markets.

Estimated Discount To Fair Value: 38%

BRP is trading at CA$50.82, well below its estimated fair value of CA$81.92, suggesting it's undervalued based on cash flows. Despite a recent net loss of CA$213.1 million due to large one-off items, earnings are forecast to grow significantly at 39.8% annually, outpacing the Canadian market's growth rate. The company's high debt level remains a concern, but its return on equity is projected to be very high in three years at 55.9%.

- Upon reviewing our latest growth report, BRP's projected financial performance appears quite optimistic.

- Click to explore a detailed breakdown of our findings in BRP's balance sheet health report.

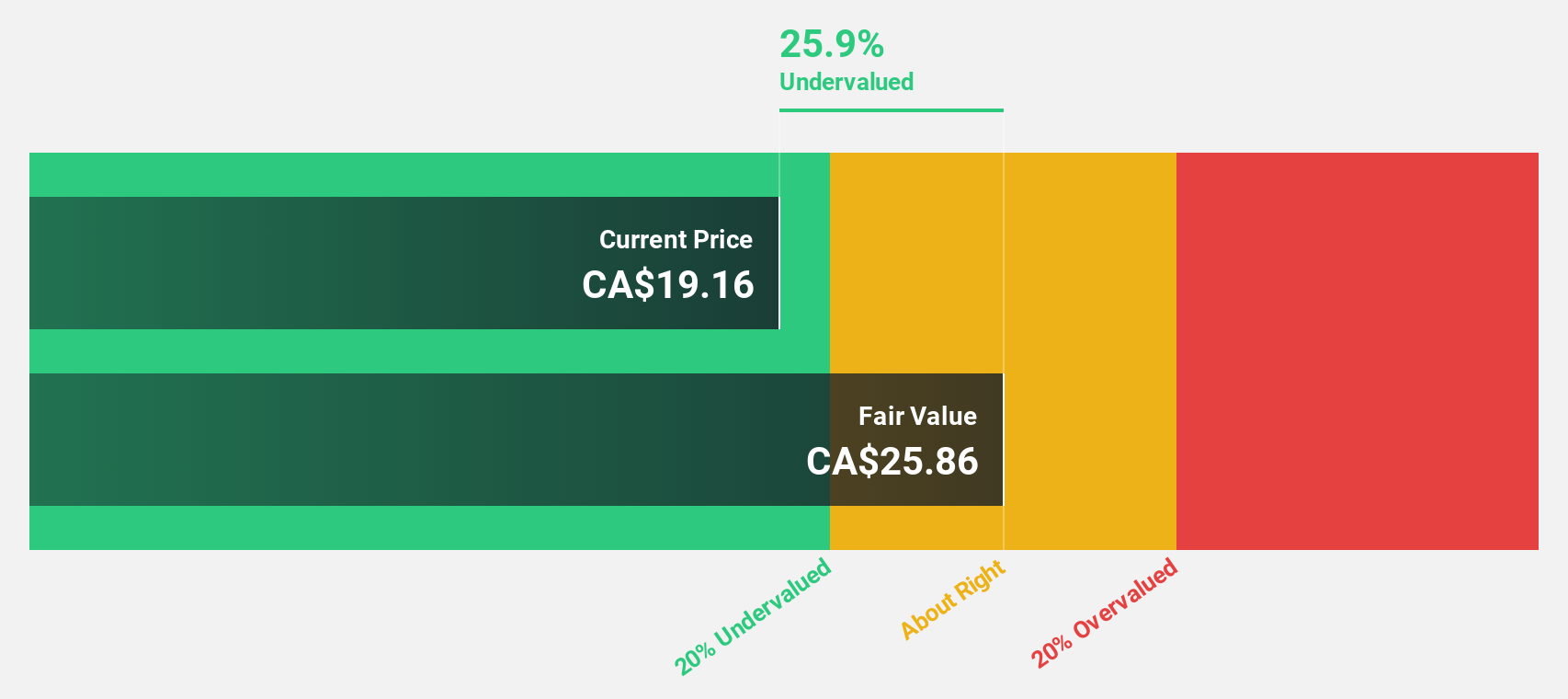

Savaria (TSX:SIS)

Overview: Savaria Corporation offers accessibility solutions for the elderly and physically challenged across Canada, the United States, Europe, and internationally, with a market cap of CA$1.20 billion.

Operations: The company's revenue is generated from two main segments: Patient Care, contributing CA$193.88 million, and Accessibility (including Adapted Vehicles), which accounts for CA$673.88 million.

Estimated Discount To Fair Value: 45.6%

Savaria Corporation, trading at CA$16.53, is significantly undervalued with an estimated fair value of CA$30.37. Earnings grew by 28.2% last year and are projected to increase by 22.4% annually, surpassing the Canadian market's growth rate of 14.9%. Recent earnings reported sales of CA$867.76 million and net income of CA$48.51 million for 2024, with revenue expected to reach approximately $925 million in fiscal 2025, driven by strategic initiatives across key segments.

- Our earnings growth report unveils the potential for significant increases in Savaria's future results.

- Get an in-depth perspective on Savaria's balance sheet by reading our health report here.

Taking Advantage

- Gain an insight into the universe of 23 Undervalued TSX Stocks Based On Cash Flows by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:SIS

Savaria

Provides accessibility solutions for the elderly and physically challenged people in Canada, the United States, Europe, and internationally.

Established dividend payer and good value.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets