Advertisement

Transcontinental Inc. Just Beat EPS By 33%: Here's What Analysts Think Will Happen Next

Shareholders of Transcontinental Inc. (TSE:TCL.A) will be pleased this week, given that the stock price is up 16% to CA$25.73 following its latest quarterly results. It looks like a credible result overall - although revenues of CA$623m were what the analysts expected, Transcontinental surprised by delivering a (statutory) profit of CA$0.41 per share, an impressive 33% above what was forecast. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for Transcontinental

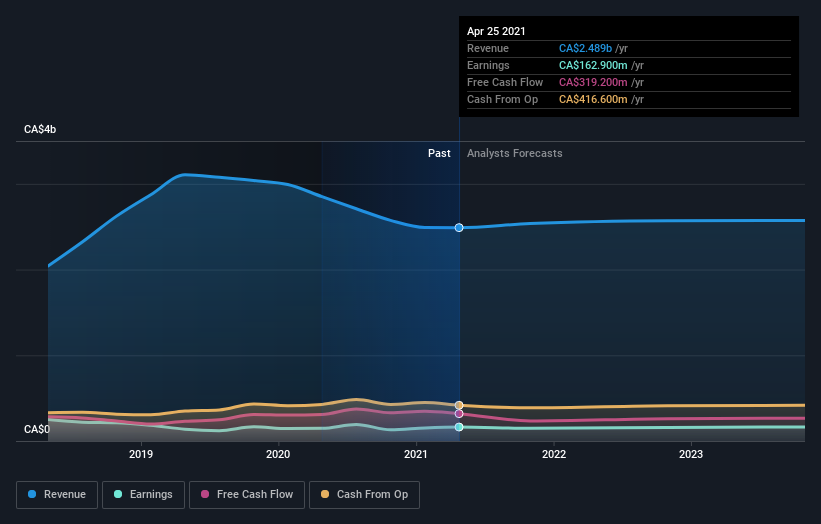

Following last week's earnings report, Transcontinental's six analysts are forecasting 2021 revenues to be CA$2.54b, approximately in line with the last 12 months. Statutory per share are forecast to be CA$1.75, approximately in line with the last 12 months. In the lead-up to this report, the analysts had been modelling revenues of CA$2.53b and earnings per share (EPS) of CA$1.61 in 2021. The analysts seems to have become more bullish on the business, judging by their new earnings per share estimates.

The analysts have been lifting their price targets on the back of the earnings upgrade, with the consensus price target rising 5.9% to CA$27.00. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Transcontinental analyst has a price target of CA$32.00 per share, while the most pessimistic values it at CA$24.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Transcontinental's revenue growth will slow down substantially, with revenues to the end of 2021 expected to display 3.9% growth on an annualised basis. This is compared to a historical growth rate of 8.1% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 13% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Transcontinental.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Transcontinental following these results. On the plus side, there were no major changes to revenue estimates; although forecasts imply revenues will perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn't be too quick to come to a conclusion on Transcontinental. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Transcontinental analysts - going out to 2023, and you can see them free on our platform here.

Before you take the next step you should know about the 1 warning sign for Transcontinental that we have uncovered.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Transcontinental might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:TCL.A

Transcontinental

Engages in the flexible packaging business in Canada, the United States, Latin America, the United Kingdom, and internationally.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets