Advertisement

- Brazil

- /

- Specialty Stores

- /

- BOVESPA:LREN3

These 4 Measures Indicate That Lojas Renner (BVMF:LREN3) Is Using Debt Reasonably Well

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Lojas Renner S.A. (BVMF:LREN3) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Lojas Renner

How Much Debt Does Lojas Renner Carry?

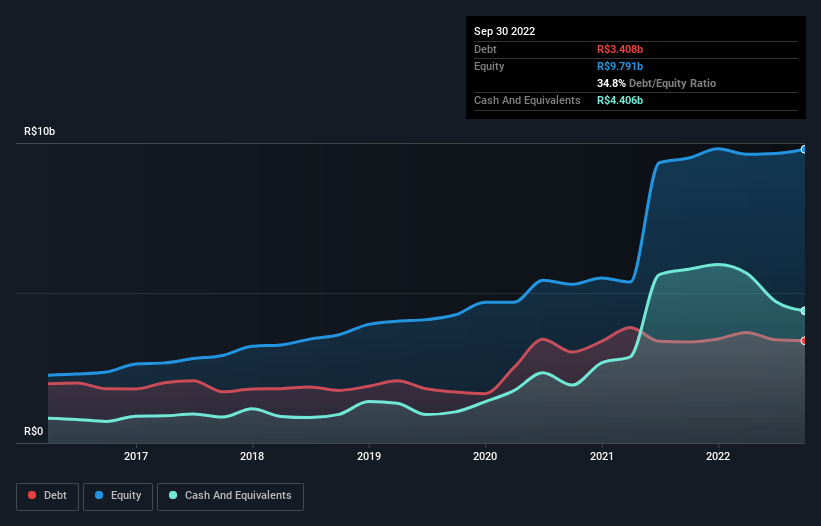

The chart below, which you can click on for greater detail, shows that Lojas Renner had R$3.41b in debt in September 2022; about the same as the year before. But it also has R$4.41b in cash to offset that, meaning it has R$998.6m net cash.

How Healthy Is Lojas Renner's Balance Sheet?

The latest balance sheet data shows that Lojas Renner had liabilities of R$7.30b due within a year, and liabilities of R$3.73b falling due after that. Offsetting these obligations, it had cash of R$4.41b as well as receivables valued at R$6.48b due within 12 months. So these liquid assets roughly match the total liabilities.

Having regard to Lojas Renner's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the R$19.8b company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, Lojas Renner also has more cash than debt, so we're pretty confident it can manage its debt safely.

Even more impressive was the fact that Lojas Renner grew its EBIT by 2,855% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Lojas Renner's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Lojas Renner has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Looking at the most recent three years, Lojas Renner recorded free cash flow of 34% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing Up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Lojas Renner has R$998.6m in net cash. And it impressed us with its EBIT growth of 2,855% over the last year. So is Lojas Renner's debt a risk? It doesn't seem so to us. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Lojas Renner , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:LREN3

Lojas Renner

Operates as a fashion and lifestyle company in Brazil, Argentina, and Uruguay.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor