Advertisement

- Brazil

- /

- Real Estate

- /

- BOVESPA:BRPR3

Analysts Have Just Cut Their BR Properties S.A. (BVMF:BRPR3) Revenue Estimates By 17%

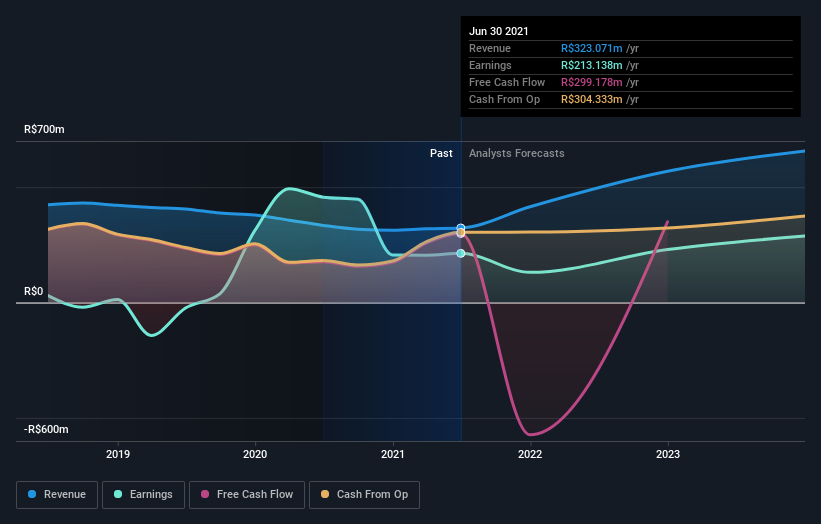

Market forces rained on the parade of BR Properties S.A. (BVMF:BRPR3) shareholders today, when the analysts downgraded their forecasts for this year. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic.

Following the downgrade, the most recent consensus for BR Properties from its five analysts is for revenues of R$345m in 2021 which, if met, would be a reasonable 6.6% increase on its sales over the past 12 months. Statutory earnings per share are anticipated to nosedive 42% to R$0.26 in the same period. Prior to this update, the analysts had been forecasting revenues of R$416m and earnings per share (EPS) of R$0.28 in 2021. It looks like analyst sentiment has fallen somewhat in this update, with a measurable cut to revenue estimates and a minor downgrade to earnings per share numbers as well.

View our latest analysis for BR Properties

Analysts made no major changes to their price target of R$11.31, suggesting the downgrades are not expected to have a long-term impact on BR Properties' valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on BR Properties, with the most bullish analyst valuing it at R$15.00 and the most bearish at R$10.00 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. One thing stands out from these estimates, which is that BR Properties is forecast to grow faster in the future than it has in the past, with revenues expected to display 14% annualised growth until the end of 2021. If achieved, this would be a much better result than the 10% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 14% annually. So while BR Properties' revenues are expected to improve, it seems that it is expected to grow at about the same rate as the overall industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. There was also a drop in their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of BR Properties going forwards.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple BR Properties analysts - going out to 2023, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BR Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BOVESPA:BRPR3

BR Properties

BR Properties is one of the leading high-income commercial real estate investment companies in Brazil, focused on the acquisition, leasing, management, development and sale of commercial real estate, including office buildings and industrial and logistics warehouses, located in the main metropolitan regions from Brazil.

Good value with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor