Advertisement

Blau Farmacêutica S.A.'s (BVMF:BLAU3) 25% Share Price Surge Not Quite Adding Up

Despite an already strong run, Blau Farmacêutica S.A. (BVMF:BLAU3) shares have been powering on, with a gain of 25% in the last thirty days. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 5.8% over the last year.

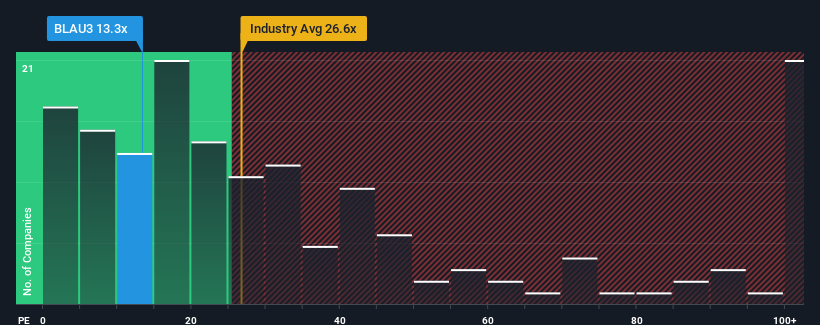

After such a large jump in price, Blau Farmacêutica may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 13.3x, since almost half of all companies in Brazil have P/E ratios under 9x and even P/E's lower than 6x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

While the market has experienced earnings growth lately, Blau Farmacêutica's earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Blau Farmacêutica

What Are Growth Metrics Telling Us About The High P/E?

Blau Farmacêutica's P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 30%. This means it has also seen a slide in earnings over the longer-term as EPS is down 43% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 15% per annum as estimated by the eight analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 16% per year, which is not materially different.

With this information, we find it interesting that Blau Farmacêutica is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

The Final Word

The large bounce in Blau Farmacêutica's shares has lifted the company's P/E to a fairly high level. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Blau Farmacêutica's analyst forecasts revealed that its market-matching earnings outlook isn't impacting its high P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Blau Farmacêutica that you should be aware of.

Of course, you might also be able to find a better stock than Blau Farmacêutica. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Blau Farmacêutica might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:BLAU3

Blau Farmacêutica

A pharmaceutical company provides high-complpexity drugs in Brazil, Argentina, Chile, Colombia, Uruguay, Ecuador, Peru, and the United States.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor