Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Biomm S.A. (BVMF:BIOM3) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Biomm

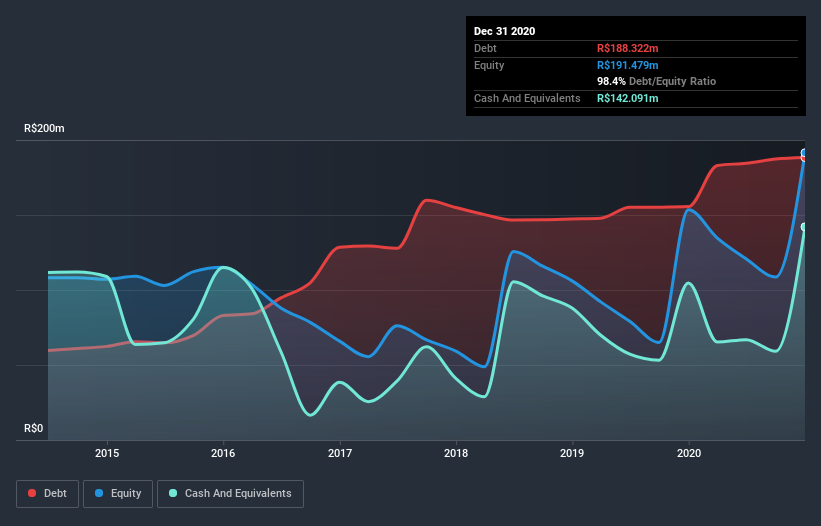

How Much Debt Does Biomm Carry?

As you can see below, at the end of December 2020, Biomm had R$188.3m of debt, up from R$155.6m a year ago. Click the image for more detail. However, it does have R$142.1m in cash offsetting this, leading to net debt of about R$46.2m.

A Look At Biomm's Liabilities

We can see from the most recent balance sheet that Biomm had liabilities of R$66.3m falling due within a year, and liabilities of R$177.2m due beyond that. Offsetting this, it had R$142.1m in cash and R$21.6m in receivables that were due within 12 months. So its liabilities total R$79.8m more than the combination of its cash and short-term receivables.

Given Biomm has a market capitalization of R$1.08b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Biomm will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Biomm wasn't profitable at an EBIT level, but managed to grow its revenue by 550%, to R$59m. That's virtually the hole-in-one of revenue growth!

Caveat Emptor

Despite the top line growth, Biomm still had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost R$55m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through R$100m of cash over the last year. So suffice it to say we consider the stock very risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Biomm (1 can't be ignored!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Biomm, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Biomm might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BOVESPA:BIOM3

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor