Biomm S.A. (BVMF:BIOM3) Investors Are Less Pessimistic Than Expected

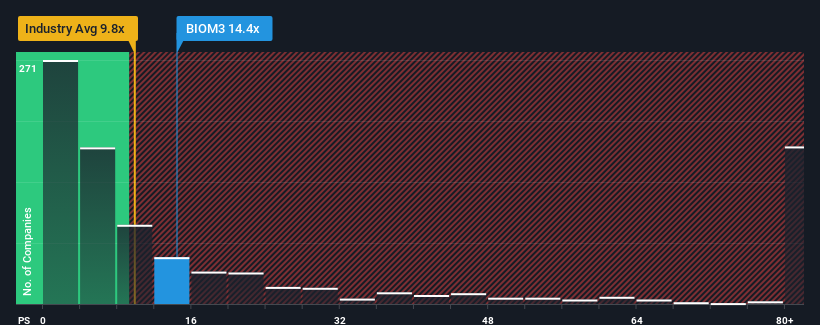

Biomm S.A.'s (BVMF:BIOM3) price-to-sales (or "P/S") ratio of 14.4x might make it look like a sell right now compared to the Biotechs industry in Brazil, where around half of the companies have P/S ratios below 9.8x and even P/S below 4x are quite common. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Biomm

What Does Biomm's Recent Performance Look Like?

Biomm has been doing a good job lately as it's been growing revenue at a solid pace. Perhaps the market is expecting this decent revenue performance to beat out the industry over the near term, which has kept the P/S propped up. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for Biomm, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Biomm's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as Biomm's is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a decent 7.6% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 94% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Comparing that to the industry, which is predicted to deliver 260% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this in mind, we find it worrying that Biomm's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Final Word

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

The fact that Biomm currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you settle on your opinion, we've discovered 3 warning signs for Biomm that you should be aware of.

If you're unsure about the strength of Biomm's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Biomm might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BOVESPA:BIOM3

Flawless balance sheet low.

Market Insights

Community Narratives