Advertisement

- Brazil

- /

- Entertainment

- /

- BOVESPA:SHOW3

We Think That There Are Issues Underlying T4F Entretenimento's (BVMF:SHOW3) Earnings

T4F Entretenimento S.A. (BVMF:SHOW3) just reported some strong earnings, and the market reacted accordingly with a healthy uplift in the share price. We did some analysis and think that investors are missing some details hidden beneath the profit numbers.

Check out our latest analysis for T4F Entretenimento

A Closer Look At T4F Entretenimento's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

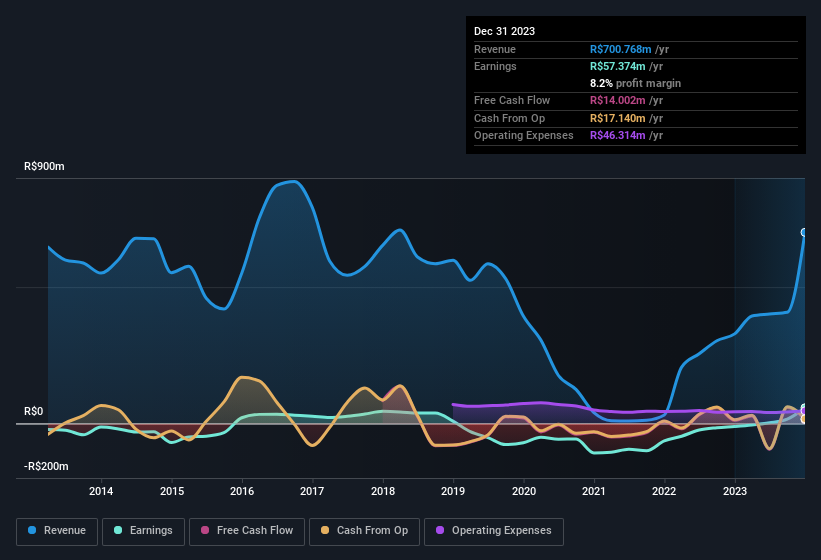

T4F Entretenimento has an accrual ratio of 1.01 for the year to December 2023. That means it didn't generate anywhere near enough free cash flow to match its profit. As a general rule, that bodes poorly for future profitability. To wit, it produced free cash flow of R$14m during the period, falling well short of its reported profit of R$57.4m. At this point we should mention that T4F Entretenimento did manage to increase its free cash flow in the last twelve months One positive for T4F Entretenimento shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of T4F Entretenimento.

Our Take On T4F Entretenimento's Profit Performance

As we discussed above, we think T4F Entretenimento's earnings were not supported by free cash flow, which might concern some investors. As a result, we think it may well be the case that T4F Entretenimento's underlying earnings power is lower than its statutory profit. On the bright side, the company showed enough improvement to book a profit this year, after losing money last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. For example, T4F Entretenimento has 3 warning signs (and 2 which are significant) we think you should know about.

This note has only looked at a single factor that sheds light on the nature of T4F Entretenimento's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if T4F Entretenimento might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:SHOW3

T4F Entretenimento

Operates as a live entertainment company in South America.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor