Advertisement

Declining Stock and Solid Fundamentals: Is The Market Wrong About Wiz Soluções e Corretagem de Seguros S.A. (BVMF:WIZS3)?

It is hard to get excited after looking at Wiz Soluções e Corretagem de Seguros' (BVMF:WIZS3) recent performance, when its stock has declined 14% over the past three months. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. Specifically, we decided to study Wiz Soluções e Corretagem de Seguros' ROE in this article.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

Check out our latest analysis for Wiz Soluções e Corretagem de Seguros

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Wiz Soluções e Corretagem de Seguros is:

60% = R$217m ÷ R$363m (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. So, this means that for every R$1 of its shareholder's investments, the company generates a profit of R$0.60.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Wiz Soluções e Corretagem de Seguros' Earnings Growth And 60% ROE

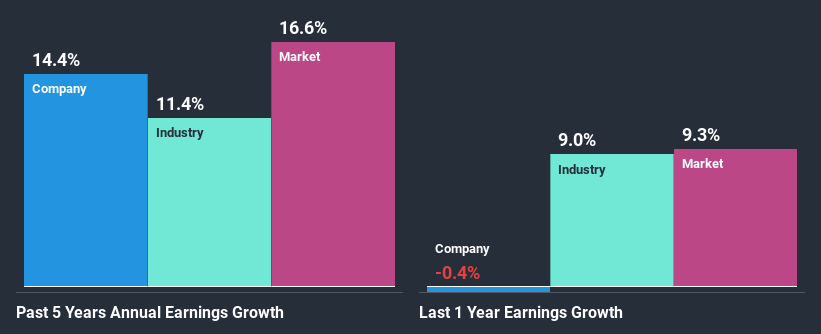

To begin with, Wiz Soluções e Corretagem de Seguros has a pretty high ROE which is interesting. Additionally, the company's ROE is higher compared to the industry average of 19% which is quite remarkable. This probably laid the groundwork for Wiz Soluções e Corretagem de Seguros' moderate 14% net income growth seen over the past five years.

Next, on comparing with the industry net income growth, we found that Wiz Soluções e Corretagem de Seguros' growth is quite high when compared to the industry average growth of 11% in the same period, which is great to see.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Wiz Soluções e Corretagem de Seguros''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Wiz Soluções e Corretagem de Seguros Using Its Retained Earnings Effectively?

While Wiz Soluções e Corretagem de Seguros has a three-year median payout ratio of 88% (which means it retains 12% of profits), the company has still seen a fair bit of earnings growth in the past, meaning that its high payout ratio hasn't hampered its ability to grow.

While Wiz Soluções e Corretagem de Seguros has been growing its earnings, it only recently started to pay dividends which likely means that the company decided to impress new and existing shareholders with a dividend. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 76%.

Summary

On the whole, we feel that Wiz Soluções e Corretagem de Seguros' performance has been quite good. In particular, its high ROE is quite noteworthy and also the probable explanation behind its considerable earnings growth. Yet, the company is retaining a small portion of its profits. Which means that the company has been able to grow its earnings in spite of it, so that's not too bad. That being so, according to the latest industry analyst forecasts, the company's earnings are expected to shrink in the future. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you’re looking to trade Wiz Soluções e Corretagem de Seguros, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wiz Co Participações e Corretagem de Seguros might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BOVESPA:WIZC3

Wiz Co Participações e Corretagem de Seguros

Wiz Co Participações e Corretagem de Seguros S.A.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor