Advertisement

IRB-Brasil Resseguros S.A.'s (BVMF:IRBR3) Financials Are Too Obscure To Link With Current Share Price Momentum: What's In Store For the Stock?

IRB-Brasil Resseguros (BVMF:IRBR3) has had a great run on the share market with its stock up by a significant 19% over the last month. However, we wonder if the company's inconsistent financials would have any adverse impact on the current share price momentum. Specifically, we decided to study IRB-Brasil Resseguros' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for IRB-Brasil Resseguros

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for IRB-Brasil Resseguros is:

6.3% = R$307m ÷ R$4.9b (Based on the trailing twelve months to September 2020).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every R$1 worth of equity, the company was able to earn R$0.06 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

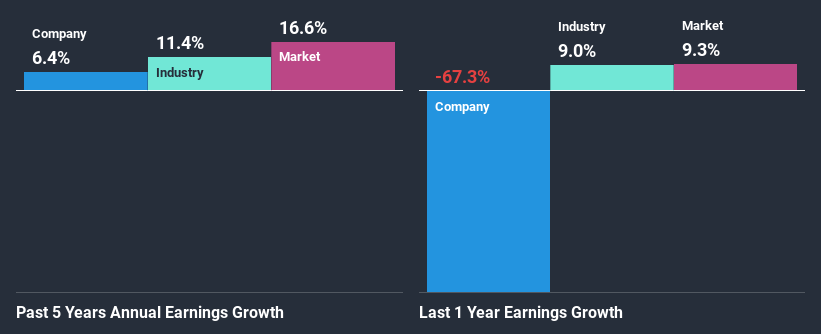

A Side By Side comparison of IRB-Brasil Resseguros' Earnings Growth And 6.3% ROE

As you can see, IRB-Brasil Resseguros' ROE looks pretty weak. Not just that, even compared to the industry average of 19%, the company's ROE is entirely unremarkable. IRB-Brasil Resseguros was still able to see a decent net income growth of 6.4% over the past five years. We reckon that there could be other factors at play here. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

We then compared IRB-Brasil Resseguros' net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 11% in the same period, which is a bit concerning.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is IRB-Brasil Resseguros fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is IRB-Brasil Resseguros Efficiently Re-investing Its Profits?

The high three-year median payout ratio of 74% (or a retention ratio of 26%) for IRB-Brasil Resseguros suggests that the company's growth wasn't really hampered despite it returning most of its income to its shareholders.

Besides, IRB-Brasil Resseguros has been paying dividends over a period of three years. This shows that the company is committed to sharing profits with its shareholders. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to drop to 44% over the next three years. The fact that the company's ROE is expected to rise to 13% over the same period is explained by the drop in the payout ratio.

Conclusion

Overall, we have mixed feelings about IRB-Brasil Resseguros. Although the company has shown a fair bit of growth in earnings, the reinvestment rate is low. Meaning, the earnings growth number could have been significantly higher had the company been retaining more of its profits and reinvesting that at a higher rate of return. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you decide to trade IRB-Brasil Resseguros, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BOVESPA:IRBR3

IRB-Brasil Resseguros

Provides reinsurance solutions in Brazil and internationally.

Proven track record and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor