Advertisement

- Brazil

- /

- Healthcare Services

- /

- BOVESPA:PFRM3

Profarma Distribuidora de Produtos Farmacêuticos S.A.'s (BVMF:PFRM3) 28% Price Boost Is Out Of Tune With Earnings

Profarma Distribuidora de Produtos Farmacêuticos S.A. (BVMF:PFRM3) shares have had a really impressive month, gaining 28% after a shaky period beforehand. Looking back a bit further, it's encouraging to see the stock is up 82% in the last year.

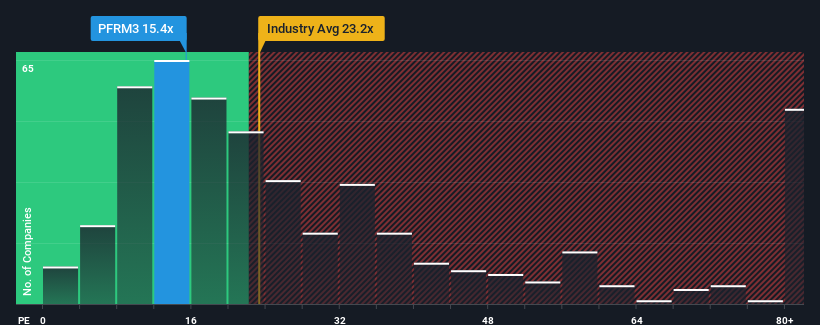

Following the firm bounce in price, Profarma Distribuidora de Produtos Farmacêuticos' price-to-earnings (or "P/E") ratio of 15.4x might make it look like a sell right now compared to the market in Brazil, where around half of the companies have P/E ratios below 10x and even P/E's below 7x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

For example, consider that Profarma Distribuidora de Produtos Farmacêuticos' financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Profarma Distribuidora de Produtos Farmacêuticos

How Is Profarma Distribuidora de Produtos Farmacêuticos' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as Profarma Distribuidora de Produtos Farmacêuticos' is when the company's growth is on track to outshine the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 47%. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 5.6% in total. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 23% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we find it concerning that Profarma Distribuidora de Produtos Farmacêuticos is trading at a P/E higher than the market. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

What We Can Learn From Profarma Distribuidora de Produtos Farmacêuticos' P/E?

The large bounce in Profarma Distribuidora de Produtos Farmacêuticos' shares has lifted the company's P/E to a fairly high level. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Profarma Distribuidora de Produtos Farmacêuticos currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Profarma Distribuidora de Produtos Farmacêuticos that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:PFRM3

Profarma Distribuidora de Produtos Farmacêuticos

Engages in the distribution of pharmaceutical products in Brazil.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.6% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.8% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.9% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$206.17|20.5% undervalued

AN

Based on Analyst Price Targets