Advertisement

- Brazil

- /

- Healthcare Services

- /

- BOVESPA:PFRM3

Profarma Distribuidora de Produtos Farmacêuticos (BVMF:PFRM3) Has A Somewhat Strained Balance Sheet

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Profarma Distribuidora de Produtos Farmacêuticos S.A. (BVMF:PFRM3) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Profarma Distribuidora de Produtos Farmacêuticos

How Much Debt Does Profarma Distribuidora de Produtos Farmacêuticos Carry?

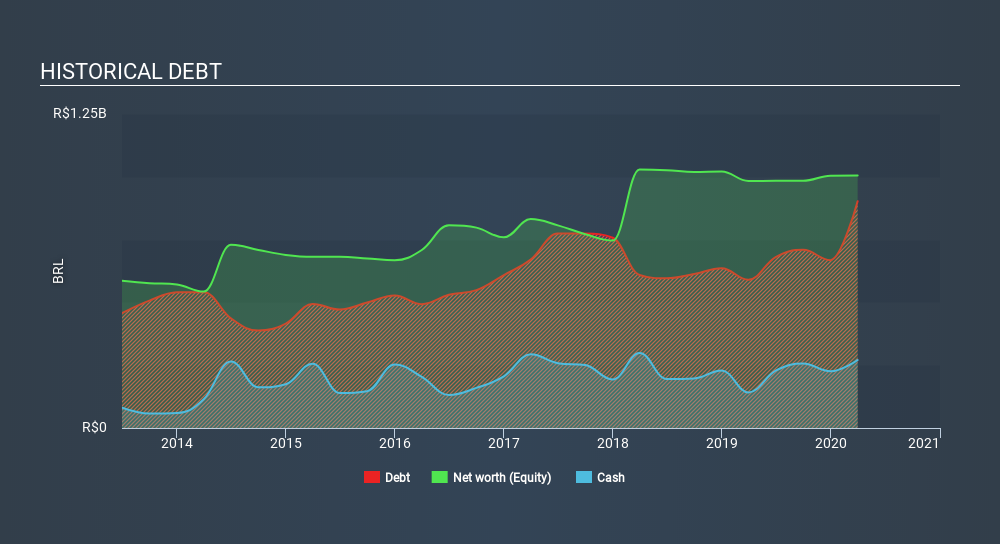

As you can see below, at the end of March 2020, Profarma Distribuidora de Produtos Farmacêuticos had R$902.5m of debt, up from R$590.2m a year ago. Click the image for more detail. However, it does have R$270.8m in cash offsetting this, leading to net debt of about R$631.7m.

A Look At Profarma Distribuidora de Produtos Farmacêuticos's Liabilities

Zooming in on the latest balance sheet data, we can see that Profarma Distribuidora de Produtos Farmacêuticos had liabilities of R$1.96b due within 12 months and liabilities of R$618.6m due beyond that. Offsetting these obligations, it had cash of R$270.8m as well as receivables valued at R$1.15b due within 12 months. So its liabilities total R$1.15b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the R$663.3m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Profarma Distribuidora de Produtos Farmacêuticos would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 1.2 times and a disturbingly high net debt to EBITDA ratio of 5.1 hit our confidence in Profarma Distribuidora de Produtos Farmacêuticos like a one-two punch to the gut. The debt burden here is substantial. Looking on the bright side, Profarma Distribuidora de Produtos Farmacêuticos boosted its EBIT by a silky 66% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Profarma Distribuidora de Produtos Farmacêuticos can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last two years, Profarma Distribuidora de Produtos Farmacêuticos saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Profarma Distribuidora de Produtos Farmacêuticos's conversion of EBIT to free cash flow and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. We should also note that Healthcare industry companies like Profarma Distribuidora de Produtos Farmacêuticos commonly do use debt without problems. We're quite clear that we consider Profarma Distribuidora de Produtos Farmacêuticos to be really rather risky, as a result of its balance sheet health. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Profarma Distribuidora de Produtos Farmacêuticos is showing 3 warning signs in our investment analysis , and 1 of those can't be ignored...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About BOVESPA:PFRM3

Profarma Distribuidora de Produtos Farmacêuticos

Engages in the distribution of pharmaceutical products in Brazil.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor