Advertisement

- Brazil

- /

- Healthcare Services

- /

- BOVESPA:ONCO3

It's A Story Of Risk Vs Reward With Oncoclínicas do Brasil Serviços Médicos S.A. (BVMF:ONCO3)

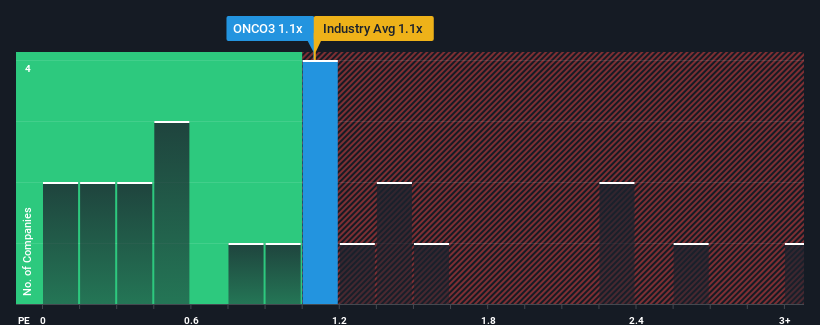

There wouldn't be many who think Oncoclínicas do Brasil Serviços Médicos S.A.'s (BVMF:ONCO3) price-to-sales (or "P/S") ratio of 1.1x is worth a mention when the median P/S for the Healthcare industry in Brazil is similar at about 1.2x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Oncoclínicas do Brasil Serviços Médicos

How Oncoclínicas do Brasil Serviços Médicos Has Been Performing

With revenue growth that's inferior to most other companies of late, Oncoclínicas do Brasil Serviços Médicos has been relatively sluggish. Perhaps the market is expecting future revenue performance to lift, which has kept the P/S from declining. If not, then existing shareholders may be a little nervous about the viability of the share price.

Keen to find out how analysts think Oncoclínicas do Brasil Serviços Médicos' future stacks up against the industry? In that case, our free report is a great place to start.How Is Oncoclínicas do Brasil Serviços Médicos' Revenue Growth Trending?

Oncoclínicas do Brasil Serviços Médicos' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 45%. The latest three year period has also seen an excellent 159% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 17% per annum as estimated by the nine analysts watching the company. With the industry only predicted to deliver 13% each year, the company is positioned for a stronger revenue result.

With this information, we find it interesting that Oncoclínicas do Brasil Serviços Médicos is trading at a fairly similar P/S compared to the industry. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From Oncoclínicas do Brasil Serviços Médicos' P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Looking at Oncoclínicas do Brasil Serviços Médicos' analyst forecasts revealed that its superior revenue outlook isn't giving the boost to its P/S that we would've expected. Perhaps uncertainty in the revenue forecasts are what's keeping the P/S ratio consistent with the rest of the industry. It appears some are indeed anticipating revenue instability, because these conditions should normally provide a boost to the share price.

Before you settle on your opinion, we've discovered 2 warning signs for Oncoclínicas do Brasil Serviços Médicos (1 shouldn't be ignored!) that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:ONCO3

Oncoclínicas do Brasil Serviços Médicos

Oncoclínicas do Brasil Serviços Médicos S.A.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor