- Brazil

- /

- Oil and Gas

- /

- BOVESPA:BRAV3

3R Petroleum Óleo e Gás S.A.'s (BVMF:RRRP3) Subdued P/S Might Signal An Opportunity

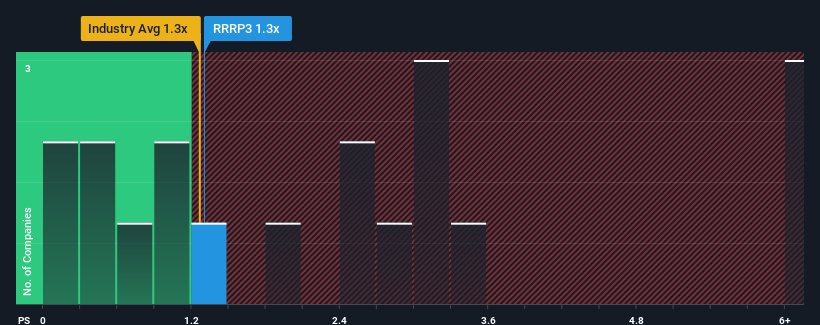

With a median price-to-sales (or "P/S") ratio of close to 1x in the Oil and Gas industry in Brazil, you could be forgiven for feeling indifferent about 3R Petroleum Óleo e Gás S.A.'s (BVMF:RRRP3) P/S ratio of 1.3x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for 3R Petroleum Óleo e Gás

What Does 3R Petroleum Óleo e Gás' Recent Performance Look Like?

Recent times have been pleasing for 3R Petroleum Óleo e Gás as its revenue has risen in spite of the industry's average revenue going into reverse. One possibility is that the P/S ratio is moderate because investors think the company's revenue will be less resilient moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Keen to find out how analysts think 3R Petroleum Óleo e Gás' future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, 3R Petroleum Óleo e Gás would need to produce growth that's similar to the industry.

If we review the last year of revenue growth, we see the company's revenues grew exponentially. Spectacularly, three year revenue growth has also set the world alight, thanks to the last 12 months of incredible growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 67% as estimated by the five analysts watching the company. With the industry only predicted to deliver 14%, the company is positioned for a stronger revenue result.

With this information, we find it interesting that 3R Petroleum Óleo e Gás is trading at a fairly similar P/S compared to the industry. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On 3R Petroleum Óleo e Gás' P/S

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Despite enticing revenue growth figures that outpace the industry, 3R Petroleum Óleo e Gás' P/S isn't quite what we'd expect. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. It appears some are indeed anticipating revenue instability, because these conditions should normally provide a boost to the share price.

Before you settle on your opinion, we've discovered 1 warning sign for 3R Petroleum Óleo e Gás that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Brava Energia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:BRAV3

Brava Energia

Engages in the exploration and production of oil and natural gas in Brazil.

High growth potential and fair value.

Market Insights

Community Narratives