Advertisement

- Brazil

- /

- Consumer Durables

- /

- BOVESPA:EZTC3

Brokers Are Upgrading Their Views On EZTEC Empreendimentos e Participações S.A. (BVMF:EZTC3) With These New Forecasts

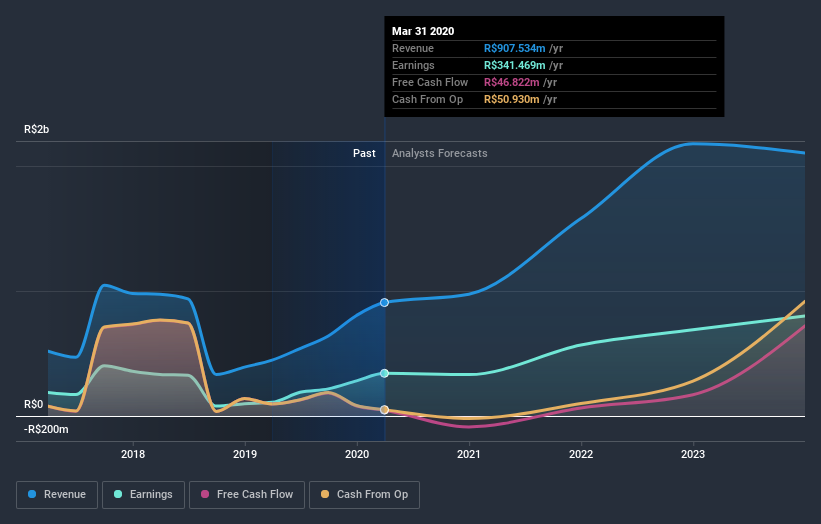

EZTEC Empreendimentos e Participações S.A. (BVMF:EZTC3) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with the analysts modelling a real improvement in business performance.

Following the upgrade, the most recent consensus for EZTEC Empreendimentos e Participações from its nine analysts is for revenues of R$974m in 2020 which, if met, would be an okay 7.3% increase on its sales over the past 12 months. Statutory earnings per share are anticipated to sink 12% to R$1.48 in the same period. Previously, the analysts had been modelling revenues of R$882m and earnings per share (EPS) of R$1.34 in 2020. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

View our latest analysis for EZTEC Empreendimentos e Participações

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the EZTEC Empreendimentos e Participações' past performance and to peers in the same industry. For example, we noticed that EZTEC Empreendimentos e Participações' rate of growth is expected to accelerate meaningfully, with revenues forecast to grow 7.3%, well above its historical decline of 5.4% a year over the past five years. Compare this against analyst estimates for the wider industry, which suggest that (in aggregate) industry revenues are expected to grow 14% next year. Although EZTEC Empreendimentos e Participações' revenues are expected to improve, it seems that the analysts are still bearish on the business, forecasting it to grow slower than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. The clear improvement in sentiment should be enough to get most shareholders feeling more optimistic about EZTEC Empreendimentos e Participações' future.

Using these estimates as a starting point, we've run a discounted cash flow calculation (DCF) on EZTEC Empreendimentos e Participações that suggests the company could be somewhat undervalued. You can learn more about our valuation methodology on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade EZTEC Empreendimentos e Participações, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if EZTEC Empreendimentos e Participações might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BOVESPA:EZTC3

EZTEC Empreendimentos e Participações

EZTEC Empreendimentos e Participações S.A.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor