We Like These Underlying Return On Capital Trends At PBG (BVMF:PTBL3)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in PBG's (BVMF:PTBL3) returns on capital, so let's have a look.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for PBG:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

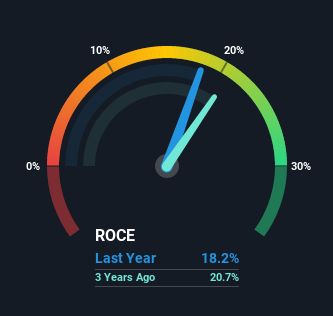

0.18 = R$222m ÷ (R$2.0b - R$758m) (Based on the trailing twelve months to June 2021).

So, PBG has an ROCE of 18%. In absolute terms, that's a pretty normal return, and it's somewhat close to the Building industry average of 16%.

See our latest analysis for PBG

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how PBG has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

We like the trends that we're seeing from PBG. The data shows that returns on capital have increased substantially over the last five years to 18%. The amount of capital employed has increased too, by 63%. So we're very much inspired by what we're seeing at PBG thanks to its ability to profitably reinvest capital.

In Conclusion...

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what PBG has. Since the stock has returned a staggering 388% to shareholders over the last five years, it looks like investors are recognizing these changes. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

PBG does have some risks though, and we've spotted 3 warning signs for PBG that you might be interested in.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BOVESPA:PTBL3

PBG

Manufactures, exports, and sells ceramic and porcelain products in Brazil and internationally.

Slight and slightly overvalued.

Market Insights

Community Narratives