Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that CEZ Distribution Bulgaria AD (BUL:CEZD) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for CEZ Distribution Bulgaria AD

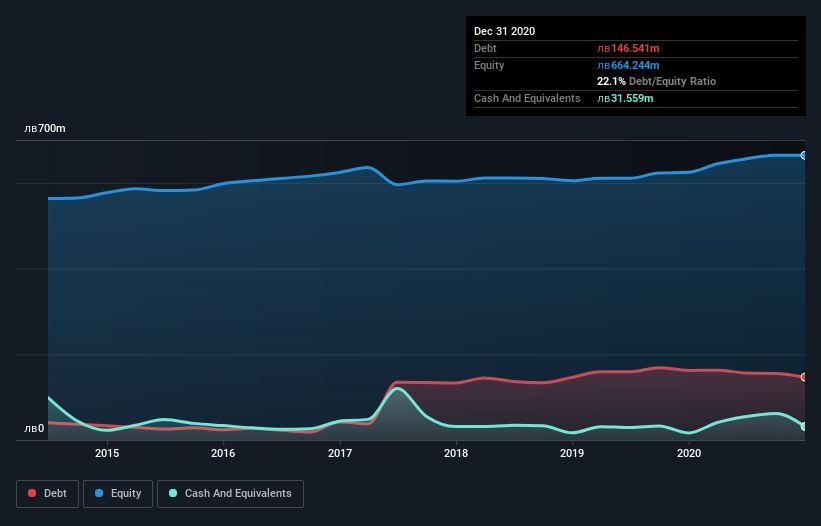

How Much Debt Does CEZ Distribution Bulgaria AD Carry?

The image below, which you can click on for greater detail, shows that CEZ Distribution Bulgaria AD had debt of лв146.5m at the end of December 2020, a reduction from лв162.3m over a year. However, because it has a cash reserve of лв31.6m, its net debt is less, at about лв115.0m.

How Healthy Is CEZ Distribution Bulgaria AD's Balance Sheet?

According to the last reported balance sheet, CEZ Distribution Bulgaria AD had liabilities of лв180.3m due within 12 months, and liabilities of лв112.8m due beyond 12 months. Offsetting these obligations, it had cash of лв31.6m as well as receivables valued at лв84.6m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by лв176.9m.

CEZ Distribution Bulgaria AD has a market capitalization of лв528.3m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

CEZ Distribution Bulgaria AD's net debt is only 0.89 times its EBITDA. And its EBIT easily covers its interest expense, being 32.4 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On top of that, CEZ Distribution Bulgaria AD grew its EBIT by 54% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if CEZ Distribution Bulgaria AD can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Considering the last three years, CEZ Distribution Bulgaria AD actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

The good news is that CEZ Distribution Bulgaria AD's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. It's also worth noting that CEZ Distribution Bulgaria AD is in the Electric Utilities industry, which is often considered to be quite defensive. All these things considered, it appears that CEZ Distribution Bulgaria AD can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it's worth monitoring the balance sheet. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of CEZ Distribution Bulgaria AD's earnings per share history for free.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade CEZ Distribution Bulgaria AD, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Electrodistribution Grid West AD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BUL:CEZD

Electrodistribution Grid West AD

Electrodistribution Grid West AD operates and maintains electricity distribution network in Bulgaria.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|37.1% undervalued

UN

Community Contributor