Advertisement

- Belgium

- /

- Metals and Mining

- /

- ENXTBR:CAMB

Campine (EBR:CAMB) Is Paying Out Less In Dividends Than Last Year

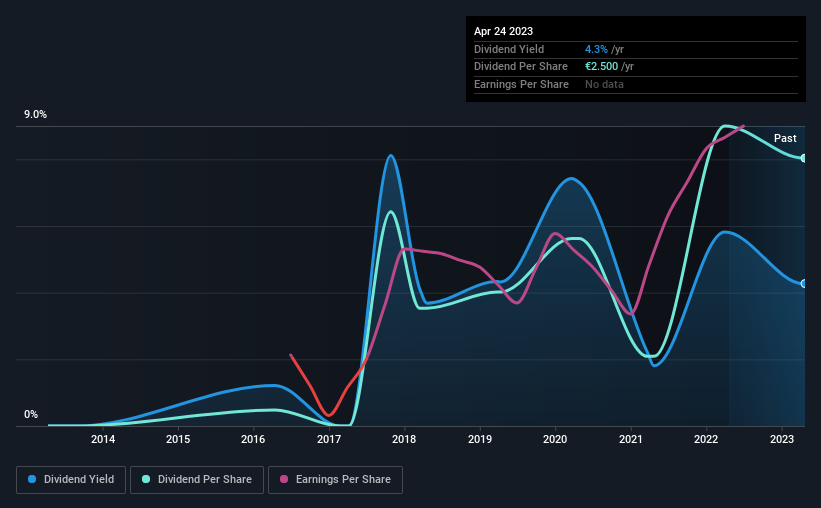

Campine NV's (EBR:CAMB) dividend is being reduced from last year's payment covering the same period to €1.75 on the 9th of June. However, the dividend yield of 4.3% still remains in a typical range for the industry.

View our latest analysis for Campine

Campine's Payment Has Solid Earnings Coverage

Unless the payments are sustainable, the dividend yield doesn't mean too much. However, Campine's earnings easily cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

Over the next year, EPS could expand by 25.1% if recent trends continue. Assuming the dividend continues along recent trends, we think the payout ratio could be 17% by next year, which is in a pretty sustainable range.

Campine's Dividend Has Lacked Consistency

Campine has been paying dividends for a while, but the track record isn't stellar. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2016, the dividend has gone from €0.15 total annually to €2.50. This implies that the company grew its distributions at a yearly rate of about 49% over that duration. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Campine has seen EPS rising for the last five years, at 25% per annum. Earnings have been growing rapidly, and with a low payout ratio we think that the company could turn out to be a great dividend stock.

Campine Looks Like A Great Dividend Stock

In general, we don't like to see the dividend being cut, especially when the company has such high potential like Campine does. The cut will allow the company to continue paying out the dividend without putting the balance sheet under pressure, which means that it could remain sustainable for longer. All in all, this checks a lot of the boxes we look for when choosing an income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, Campine has 5 warning signs (and 2 which shouldn't be ignored) we think you should know about. Is Campine not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTBR:CAMB

Campine

Engages in the circular metals and specialty chemicals businesses in Belgium and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor