Advertisement

- Belgium

- /

- Personal Products

- /

- ENXTBR:ONTEX

Lacklustre Performance Is Driving Ontex Group NV's (EBR:ONTEX) Low P/S

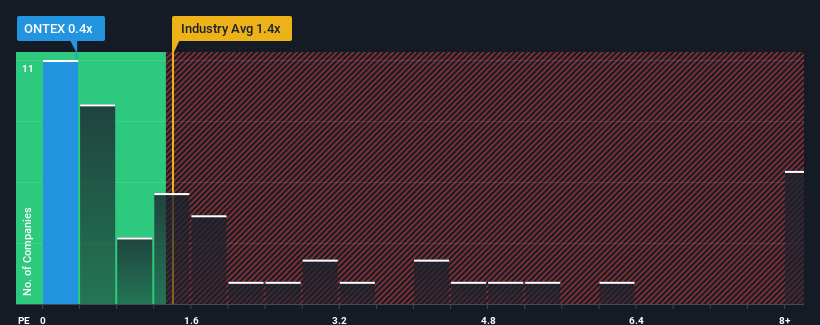

You may think that with a price-to-sales (or "P/S") ratio of 0.4x Ontex Group NV (EBR:ONTEX) is a stock worth checking out, seeing as almost half of all the Personal Products companies in Belgium have P/S ratios greater than 1.4x and even P/S higher than 5x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

Check out our latest analysis for Ontex Group

What Does Ontex Group's P/S Mean For Shareholders?

There hasn't been much to differentiate Ontex Group's and the industry's revenue growth lately. It might be that many expect the mediocre revenue performance to degrade, which has repressed the P/S ratio. If not, then existing shareholders have reason to be optimistic about the future direction of the share price.

Keen to find out how analysts think Ontex Group's future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Ontex Group?

In order to justify its P/S ratio, Ontex Group would need to produce sluggish growth that's trailing the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 7.3% last year. However, this wasn't enough as the latest three year period has seen an unpleasant 14% overall drop in revenue. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 3.0% each year during the coming three years according to the five analysts following the company. That's shaping up to be materially lower than the 5.5% per annum growth forecast for the broader industry.

With this information, we can see why Ontex Group is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Ontex Group's P/S

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As expected, our analysis of Ontex Group's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

Plus, you should also learn about these 2 warning signs we've spotted with Ontex Group (including 1 which doesn't sit too well with us).

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTBR:ONTEX

Ontex Group

Develops, produces, and sells baby, feminine, and adult care products in Belgium, the United Kingdom, Italy, the United States, France, Poland, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

FU

FundamentalFlow on Vertiv Holdings Co ·

The Short and Long Term Compounder of Liquid Cooling industry.

Fair Value:US$45040.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2034.6% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on GQG Partners ·

The Cheap Genius Problem

Fair Value:AU$2.4541.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

Recently Updated Narratives

DA

david_1211213 on Robo.ai ·

Robo.ai (AIIO): A Long-Term Bullish Technical Setup

Fair Value:US$5.6443.6% undervalued

1 followerusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on Lagenda Properties Berhad ·

Lagenda Properties 录得创纪录销售额与收入,推动盈利能见度提升

Fair Value:RM 2.543.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on STLLR Gold ·

STLLR Gold, Eric Sprott + Agnico Backed: Massive Canadian Gold Developer at Junior Prices

Fair Value:CA$102.2298.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

291 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

154 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

175 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0