Advertisement

- Belgium

- /

- Personal Products

- /

- ENXTBR:ONTEX

Is Ontex Group (EBR:ONTEX) Likely To Turn Things Around?

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Having said that, from a first glance at Ontex Group (EBR:ONTEX) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Return On Capital Employed (ROCE): What is it?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Ontex Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

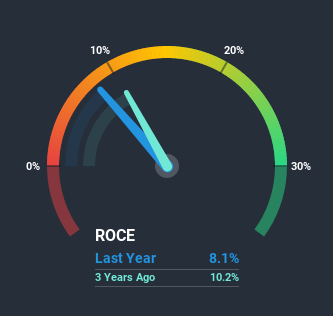

0.081 = €168m ÷ (€3.1b - €991m) (Based on the trailing twelve months to June 2020).

So, Ontex Group has an ROCE of 8.1%. On its own, that's a low figure but it's around the 9.5% average generated by the Personal Products industry.

Check out our latest analysis for Ontex Group

Above you can see how the current ROCE for Ontex Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Ontex Group here for free.

What Does the ROCE Trend For Ontex Group Tell Us?

On the surface, the trend of ROCE at Ontex Group doesn't inspire confidence. Around five years ago the returns on capital were 13%, but since then they've fallen to 8.1%. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 32%, which has impacted the ROCE. Without this increase, it's likely that ROCE would be even lower than 8.1%. Keep an eye on this ratio, because the business could encounter some new risks if this metric gets too high.The Key Takeaway

In summary, Ontex Group is reinvesting funds back into the business for growth but unfortunately it looks like sales haven't increased much just yet. And investors may be expecting the fundamentals to get a lot worse because the stock has crashed 71% over the last five years. Therefore based on the analysis done in this article, we don't think Ontex Group has the makings of a multi-bagger.

One more thing, we've spotted 2 warning signs facing Ontex Group that you might find interesting.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade Ontex Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTBR:ONTEX

Ontex Group

Develops, produces, and sells baby, feminine, and adult care products in Belgium, the United Kingdom, Italy, the United States, France, Poland, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

11 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

5 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative