Advertisement

We Think Recticel's (EBR:RECT) Profit Is Only A Baseline For What They Can Achieve

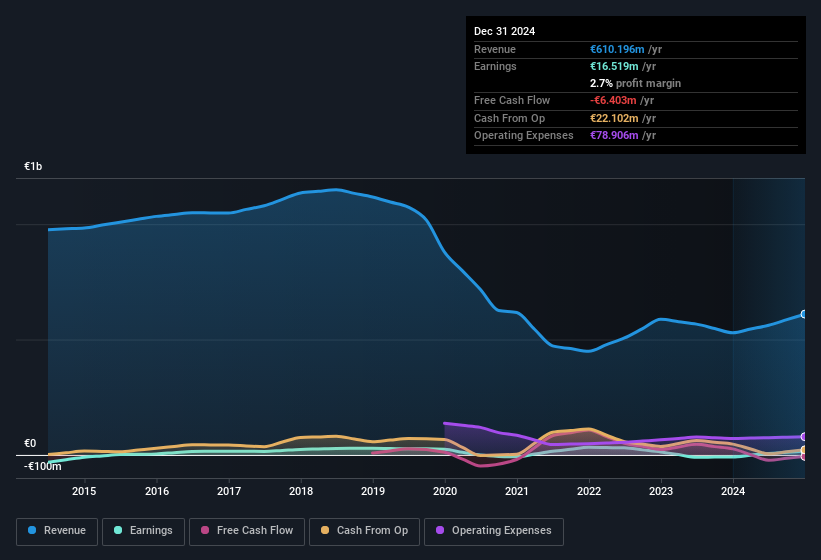

Recticel SA/NV (EBR:RECT) just reported healthy earnings but the stock price didn't move much. We think that investors have missed some encouraging factors underlying the profit figures.

Our free stock report includes 2 warning signs investors should be aware of before investing in Recticel. Read for free now.

How Do Unusual Items Influence Profit?

To properly understand Recticel's profit results, we need to consider the €8.0m expense attributed to unusual items. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. Recticel took a rather significant hit from unusual items in the year to December 2024. As a result, we can surmise that the unusual items made its statutory profit significantly weaker than it would otherwise be.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

An Unusual Tax Situation

Having already discussed the impact of the unusual items, we should also note that Recticel received a tax benefit of €1.5m. It's always a bit noteworthy when a company is paid by the tax man, rather than paying the tax man. Of course, prima facie it's great to receive a tax benefit. And since it previously lost money, it may well simply indicate the realisation of past tax losses. However, our data indicates that tax benefits can temporarily boost statutory profit in the year it is booked, but subsequently profit may fall back. Assuming the tax benefit is not repeated every year, we could see its profitability drop noticeably, all else being equal. While we think it's good that the company has booked a tax benefit, it does mean that there's every chance the statutory profit will come in a lot higher than it would be if the income was adjusted for one-off factors.

Our Take On Recticel's Profit Performance

In the last year Recticel received a tax benefit, which boosted its profit in a way that might not be much more sustainable than turning prime farmland into gas fields. Having said that, it also had a unusual item reducing its profit. Considering all the aforementioned, we'd venture that Recticel's profit result is a pretty good guide to its true profitability, albeit a bit on the conservative side. So while earnings quality is important, it's equally important to consider the risks facing Recticel at this point in time. For instance, we've identified 2 warning signs for Recticel (1 shouldn't be ignored) you should be familiar with.

Our examination of Recticel has focussed on certain factors that can make its earnings look better than they are. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTBR:RECT

Recticel

An insulation company, provides thermal and thermo-acoustic solutions in Belgium, France, the Netherlands, Germany, Slovenia, other European Union countries, the United Kingdom, the United States, and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor