Advertisement

Bearish: This Analyst Is Revising Their Wiseway Group Limited (ASX:WWG) Revenue and EPS Prognostications

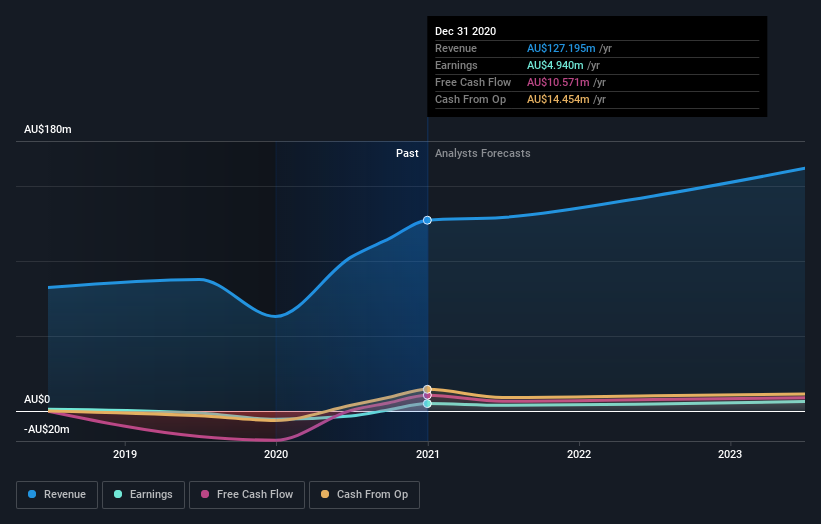

Today is shaping up negative for Wiseway Group Limited (ASX:WWG) shareholders, with the covering analyst delivering a substantial negative revision to this year's forecasts. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business. Bidders are definitely seeing a different story, with the stock price of AU$0.43 reflecting a 18% rise in the past week. It will be interesting to see if the downgrade has an impact on buying demand for the company's shares.

Following this downgrade, Wiseway Group's lone analyst are forecasting 2021 revenues to be AU$129m, approximately in line with the last 12 months. Statutory earnings per share are anticipated to plummet 28% to AU$0.025 in the same period. Before this latest update, the analyst had been forecasting revenues of AU$144m and earnings per share (EPS) of AU$0.042 in 2021. Indeed, we can see that the analyst is a lot more bearish about Wiseway Group's prospects, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for Wiseway Group

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that Wiseway Group's revenue growth is expected to slow, with the forecast 2.9% annualised growth rate until the end of 2021 being well below the historical 101% growth over the last year. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 5.9% annually. Factoring in the forecast slowdown in growth, it seems obvious that Wiseway Group is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. After a cut like that, investors could be forgiven for thinking the analyst is a lot more bearish on Wiseway Group, and a few readers might choose to steer clear of the stock.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Wiseway Group going out as far as 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Wiseway Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wiseway Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:WWG

Wiseway Group

Provides logistics and freight forwarding services in Australia, New Zealand, China, Singapore, and the United States.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor