Advertisement

WiseTech Global (ASX:WTC) Navigates Leadership Changes and Strategic Growth Amid Financial Challenges

Simply Wall St

Reviewed by Simply Wall St

WiseTech Global (ASX:WTC) is navigating significant leadership transitions with Andrew Cartledge stepping in as Interim CEO, following Richard White's transition to a consulting role. Despite strong financial health marked by impressive profit and revenue growth, challenges such as a declining net profit margin and operational inefficiencies persist. Investors should anticipate discussions on how WiseTech plans to leverage its innovation-driven strategy amidst these challenges and explore growth opportunities in the evolving logistics sector.

Click to explore a detailed breakdown of our findings on WiseTech Global.

Core Advantages Driving Sustained Success for WiseTech Global

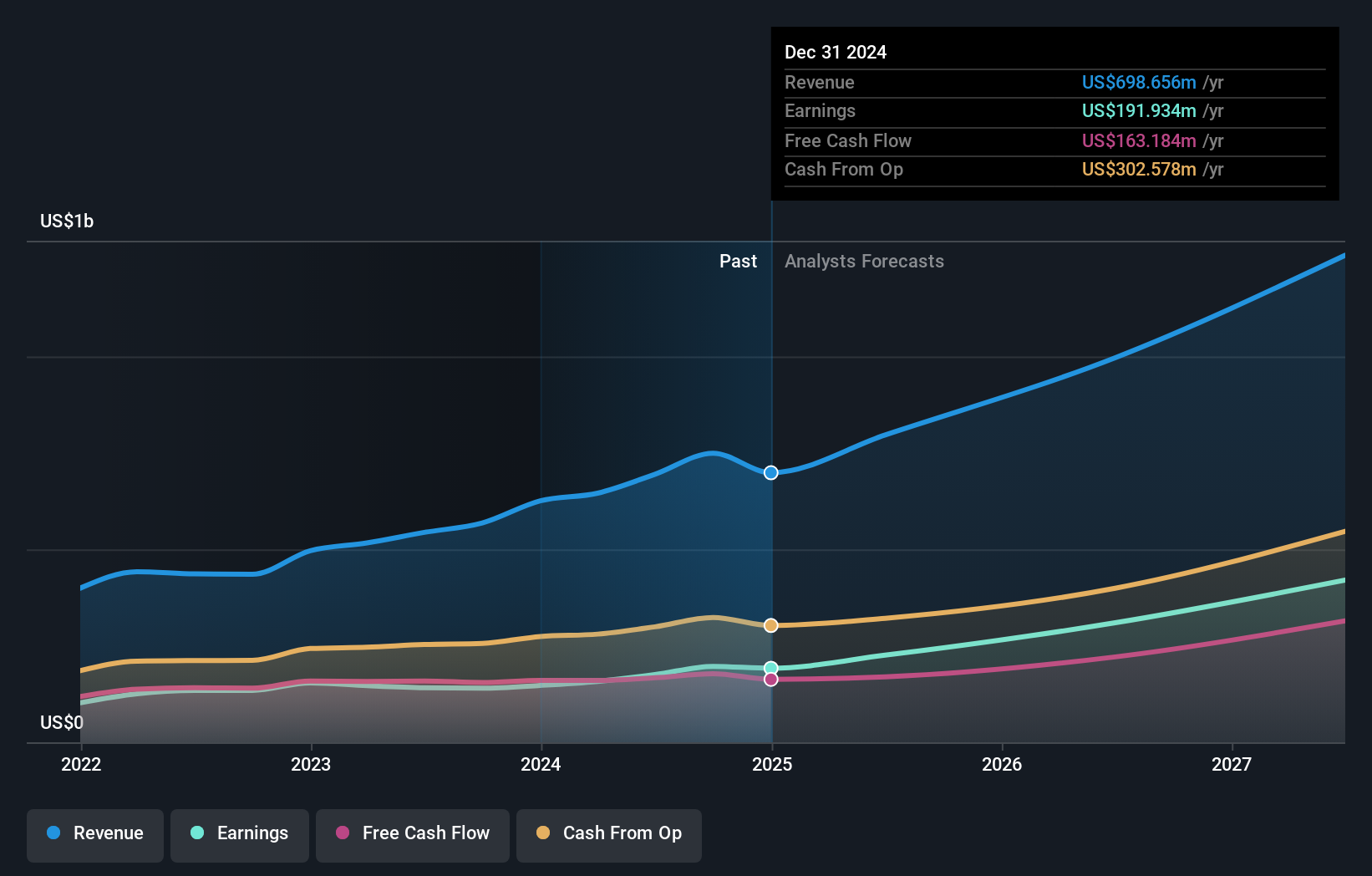

WiseTech Global's financial health is underscored by its significant annual profit growth of 23.8% and revenue forecasted to grow at 19.2% per year, outpacing the Australian market average. The company's strong cash position, with more cash than total debt and well-covered interest payments, highlights its financial standing. Leadership changes, such as Andrew Cartledge stepping in as Interim CEO, show strategic adaptability. The company's current share price, while higher than analyst targets, reflects its strong market position, albeit with a high Price-To-Earnings Ratio compared to peers.

To gain deeper insights into WiseTech Global's historical performance, explore our detailed analysis of past performance.Vulnerabilities Impacting WiseTech Global

WiseTech faces challenges with a decreased net profit margin from 26% to 25.2% and a low Return on Equity at 11.9%. The board's average tenure of 2.9 years suggests limited experience, potentially impacting strategic decisions. The high Price-To-Earnings Ratio also raises concerns about overvaluation, which could deter potential investors. Operational inefficiencies, such as supply chain issues mentioned by Andrew Cartledge, COO, further highlight areas needing improvement.

To dive deeper into how WiseTech Global's valuation metrics are shaping its market position, check out our detailed analysis of WiseTech Global's Valuation.Growth Avenues Awaiting WiseTech Global

The anticipated earnings growth significantly above market averages presents opportunities for WiseTech to expand its market share. Product-related announcements, like the launch of a new compliance tool, demonstrate its commitment to innovation and customer satisfaction. The seasoned management team's average tenure of 6.6 years provides stability, crucial for navigating expansion opportunities and strategic alliances.

See what the latest analyst reports say about WiseTech Global's future prospects and potential market movements.External Factors Threatening WiseTech Global

Economic headwinds and regulatory hurdles pose risks to WiseTech's growth projections. The company is proactively monitoring regulatory changes to mitigate potential impacts on its compliance offerings. Additionally, the high Price-To-Earnings Ratio compared to industry and peer averages may indicate overvaluation risks, as noted by analysts. Supply chain vulnerabilities, acknowledged by Richard White, CEO, require strategic responses to ensure operational continuity.

Explore the current health of WiseTech Global and how it reflects on its financial stability and growth potential.Conclusion

WiseTech Global's impressive annual profit growth of 23.8% and projected revenue increase of 19.2% per year signal strong financial health and a promising future, despite its current share price being above analyst targets. However, challenges such as a reduced net profit margin and low Return on Equity could impact its ability to maintain this growth trajectory. The company's strategic adaptability, demonstrated by leadership changes and innovative product launches, positions it well to capitalize on market opportunities, but supply chain inefficiencies and regulatory risks need addressing to ensure sustained success. While the high Price-To-Earnings Ratio suggests the stock is expensive relative to peers, WiseTech's proactive management and commitment to innovation may justify this premium if they effectively navigate these vulnerabilities.

Seize The Opportunity

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if WiseTech Global might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About ASX:WTC

WiseTech Global

Engages in the development and provision of software solutions to the logistics execution industry in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Exceptional growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor