Advertisement

Here's Why MOQ Limited's (ASX:MOQ) CEO May Not Expect A Pay Rise This Year

Performance at MOQ Limited (ASX:MOQ) has not been particularly rosy recently and shareholders will likely be holding CEO Joe D'Addio and the board accountable for this. The next AGM coming up on 08 November 2021 will be a chance for shareholders to have their concerns addressed by the board, challenge management on company strategy and vote on resolutions such as executive remuneration, which may help change the company's future prospects. From our analysis below, we think CEO compensation looks appropriate for now.

View our latest analysis for MOQ

How Does Total Compensation For Joe D'Addio Compare With Other Companies In The Industry?

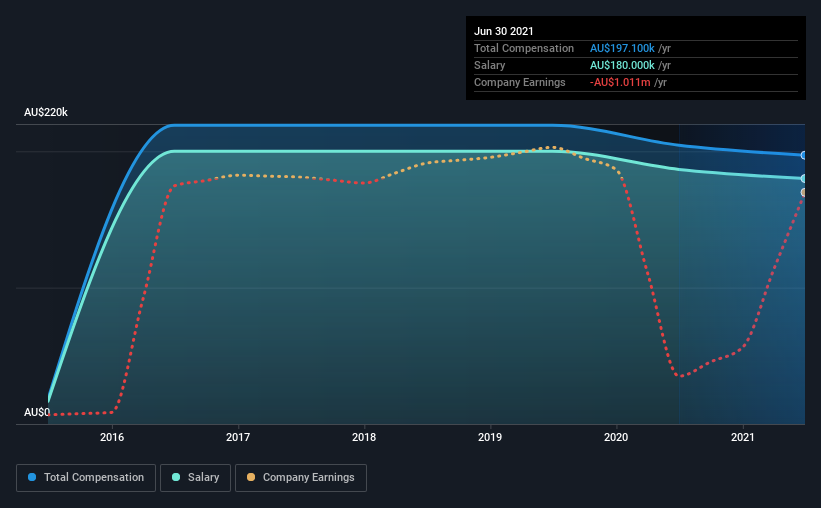

According to our data, MOQ Limited has a market capitalization of AU$40m, and paid its CEO total annual compensation worth AU$197k over the year to June 2021. We note that's a small decrease of 3.6% on last year. Notably, the salary which is AU$180.0k, represents most of the total compensation being paid.

On comparing similar-sized companies in the industry with market capitalizations below AU$266m, we found that the median total CEO compensation was AU$414k. Accordingly, MOQ pays its CEO under the industry median. Furthermore, Joe D'Addio directly owns AU$3.5m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | AU$180k | AU$187k | 91% |

| Other | AU$17k | AU$18k | 9% |

| Total Compensation | AU$197k | AU$204k | 100% |

Speaking on an industry level, nearly 63% of total compensation represents salary, while the remainder of 37% is other remuneration. It's interesting to note that MOQ pays out a greater portion of remuneration through salary, compared to the industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at MOQ Limited's Growth Numbers

MOQ Limited has reduced its earnings per share by 86% a year over the last three years. Its revenue is up 9.1% over the last year.

The decline in EPS is a bit concerning. The fairly low revenue growth fails to impress given that the EPS is down. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has MOQ Limited Been A Good Investment?

Given the total shareholder loss of 17% over three years, many shareholders in MOQ Limited are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 2 warning signs for MOQ (1 is concerning!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:MOQ

MOQ

MOQ Limited develops, builds, and acquires cloud focused technology businesses in Australia.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets