Shareholders May Not Be So Generous With Iress Limited's (ASX:IRE) CEO Compensation And Here's Why

Key Insights

- Iress will host its Annual General Meeting on 2nd of May

- Salary of AU$779.1k is part of CEO Marcus Price's total remuneration

- Total compensation is 52% above industry average

- Iress' three-year loss to shareholders was 24% while its EPS grew by 7.4% over the past three years

Shareholders of Iress Limited (ASX:IRE) will have been dismayed by the negative share price return over the last three years. What is concerning is that despite positive EPS growth, the share price has not tracked the trend in fundamentals. The AGM coming up on the 2nd of May could be an opportunity for shareholders to bring these concerns to the board's attention. They could also try to influence management and firm direction through voting on resolutions such as executive remuneration and other company matters. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

Check out our latest analysis for Iress

How Does Total Compensation For Marcus Price Compare With Other Companies In The Industry?

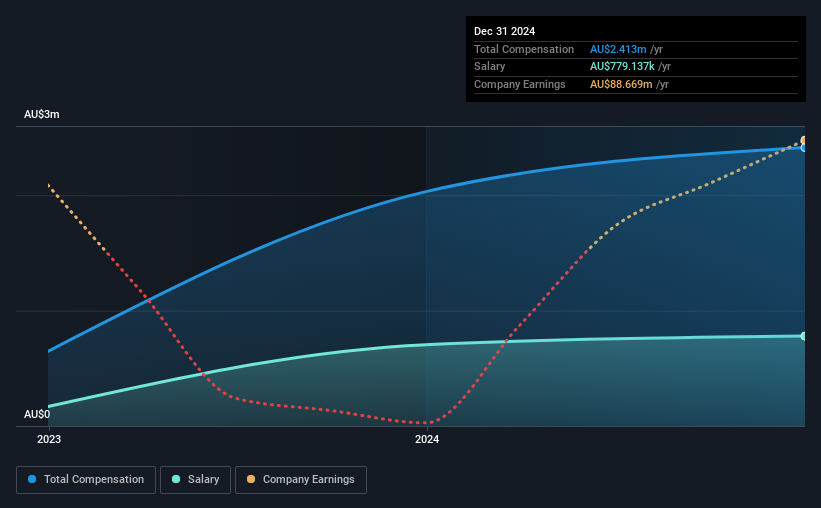

Our data indicates that Iress Limited has a market capitalization of AU$1.5b, and total annual CEO compensation was reported as AU$2.4m for the year to December 2024. That's a notable increase of 19% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at AU$779k.

For comparison, other companies in the Australian Software industry with market capitalizations ranging between AU$626m and AU$2.5b had a median total CEO compensation of AU$1.6m. Hence, we can conclude that Marcus Price is remunerated higher than the industry median. What's more, Marcus Price holds AU$904k worth of shares in the company in their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | AU$779k | AU$705k | 32% |

| Other | AU$1.6m | AU$1.3m | 68% |

| Total Compensation | AU$2.4m | AU$2.0m | 100% |

Speaking on an industry level, nearly 61% of total compensation represents salary, while the remainder of 39% is other remuneration. Iress pays a modest slice of remuneration through salary, as compared to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Iress Limited's Growth Numbers

Over the past three years, Iress Limited has seen its earnings per share (EPS) grow by 7.4% per year. It saw its revenue drop 3.4% over the last year.

We would argue that the lack of revenue growth in the last year is less than ideal, but the modest improvement in EPS is good. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Iress Limited Been A Good Investment?

With a three year total loss of 24% for the shareholders, Iress Limited would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. A huge lag in share price growth when earnings have grown may indicate there could be other issues that are affecting the company at the moment that the market is focused on. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. The upcoming AGM will be a chance for shareholders to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 1 warning sign for Iress that you should be aware of before investing.

Important note: Iress is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:IRE

Iress

Engages in the designing and developing software and services for the financial services industry in the Asia Pacific, the United Kingdom and Europe, Africa, and North America.

Good value with proven track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion