Advertisement

Discover 3 Global Undervalued Small Caps With Insider Action

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, global markets have experienced a positive shift, with U.S. equities advancing amid easing trade tensions and constructive economic indicators. Small-cap stocks, in particular, have shown resilience as they posted gains for the third consecutive week despite broader economic uncertainties such as slowing business activity growth and rising consumer prices. In this context of fluctuating market conditions, identifying promising small-cap stocks often involves looking for companies that demonstrate strong fundamentals and are potentially positioned to benefit from insider actions or strategic developments.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Morgan Advanced Materials | 10.9x | 0.5x | 41.54% | ★★★★★★ |

| Chorus Aviation | NA | 0.4x | 20.41% | ★★★★★★ |

| Tristel | 27.2x | 3.8x | 27.82% | ★★★★★☆ |

| Nexus Industrial REIT | 5.3x | 2.7x | 24.09% | ★★★★★☆ |

| Sing Investments & Finance | 7.0x | 3.6x | 43.98% | ★★★★☆☆ |

| Norcros | 23.9x | 0.6x | 28.80% | ★★★☆☆☆ |

| Westshore Terminals Investment | 13.5x | 3.9x | 36.95% | ★★★☆☆☆ |

| Calfrac Well Services | 34.2x | 0.2x | 27.79% | ★★★☆☆☆ |

| Arendals Fossekompani | NA | 1.6x | 43.16% | ★★★☆☆☆ |

| European Residential Real Estate Investment Trust | NA | 1.6x | -140.67% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

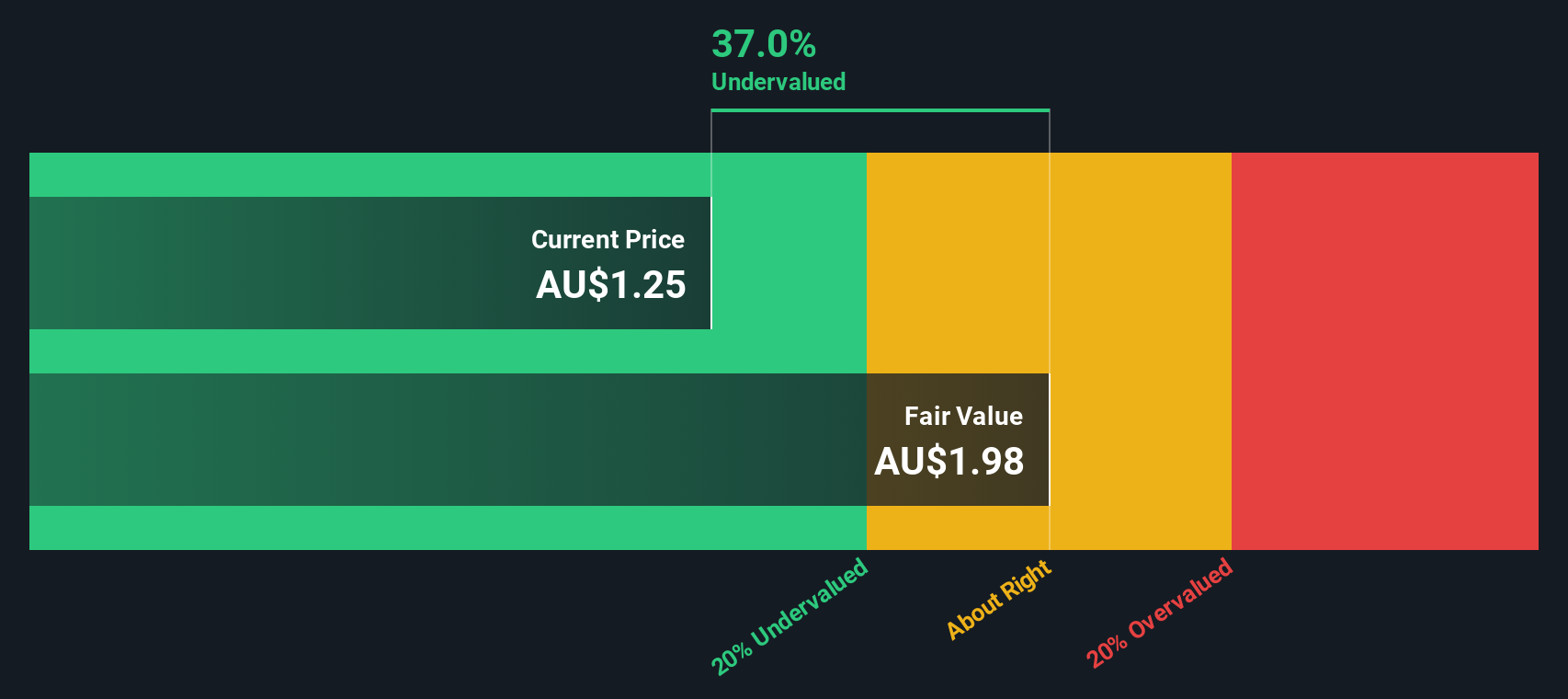

Infomedia (ASX:IFM)

Simply Wall St Value Rating: ★★★★★★

Overview: Infomedia is a company that specializes in providing software solutions for the automotive industry, with a market capitalization of A$ 0.50 billion.

Operations: Infomedia generates revenue primarily from publishing periodicals, with a recent figure of A$142.41 million. The company's gross profit margin has consistently been around 95%, indicating strong profitability before accounting for operating expenses. Operating expenses are significant, with general and administrative costs being the largest component, recently at A$71.36 million. Net income margin has shown variability, reaching 11.16% in the latest period, reflecting the impact of both operational and non-operational costs on overall profitability.

PE: 29.4x

Infomedia, a smaller company in its sector, recently reported a rise in net income to A$8.33 million for the half-year ending December 2024, up from A$5.12 million the previous year. Despite relying solely on external borrowing for funding, which carries higher risk than customer deposits, they maintain high-quality earnings with minimal one-off items affecting results. Insider confidence is evident with share repurchase plans announced in February 2025 to buy back up to 18.79 million shares by March 2026.

- Navigate through the intricacies of Infomedia with our comprehensive valuation report here.

Evaluate Infomedia's historical performance by accessing our past performance report.

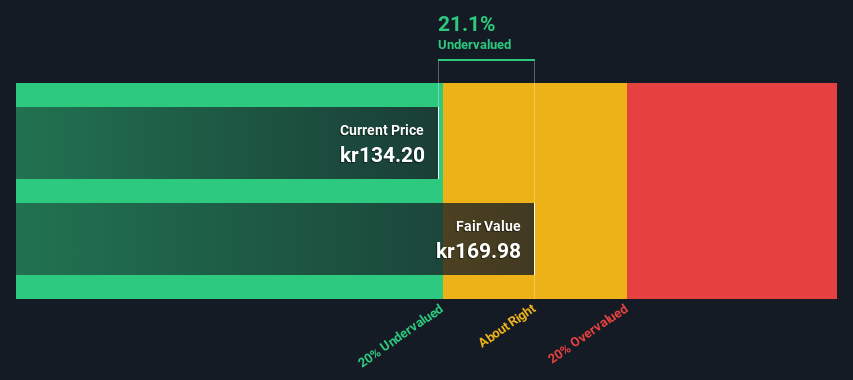

Troax Group (OM:TROAX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Troax Group specializes in manufacturing and supplying mesh panel solutions for industrial applications, with a market cap of €2.3 billion.

Operations: The company's primary revenue stream is derived from mesh panels, with recent quarterly revenues reaching €275.94 million. Over the observed periods, gross profit margin has shown fluctuations, most recently recorded at 37.30%. Operating expenses are significant, driven primarily by sales and marketing expenses which have increased to €40.43 million in the latest quarter.

PE: 24.3x

Troax Group, a security solutions provider, recently reported a slight dip in Q1 2025 sales to €68.3 million from €70.9 million last year, with net income also decreasing to €5.3 million from €6.7 million. Despite these declines, insider confidence is evident as they have increased their shareholdings over the past six months. The company maintains a dividend of €0.34 per share and forecasts earnings growth at 18% annually, although its funding relies entirely on external borrowing, which carries higher risk.

- Take a closer look at Troax Group's potential here in our valuation report.

Gain insights into Troax Group's past trends and performance with our Past report.

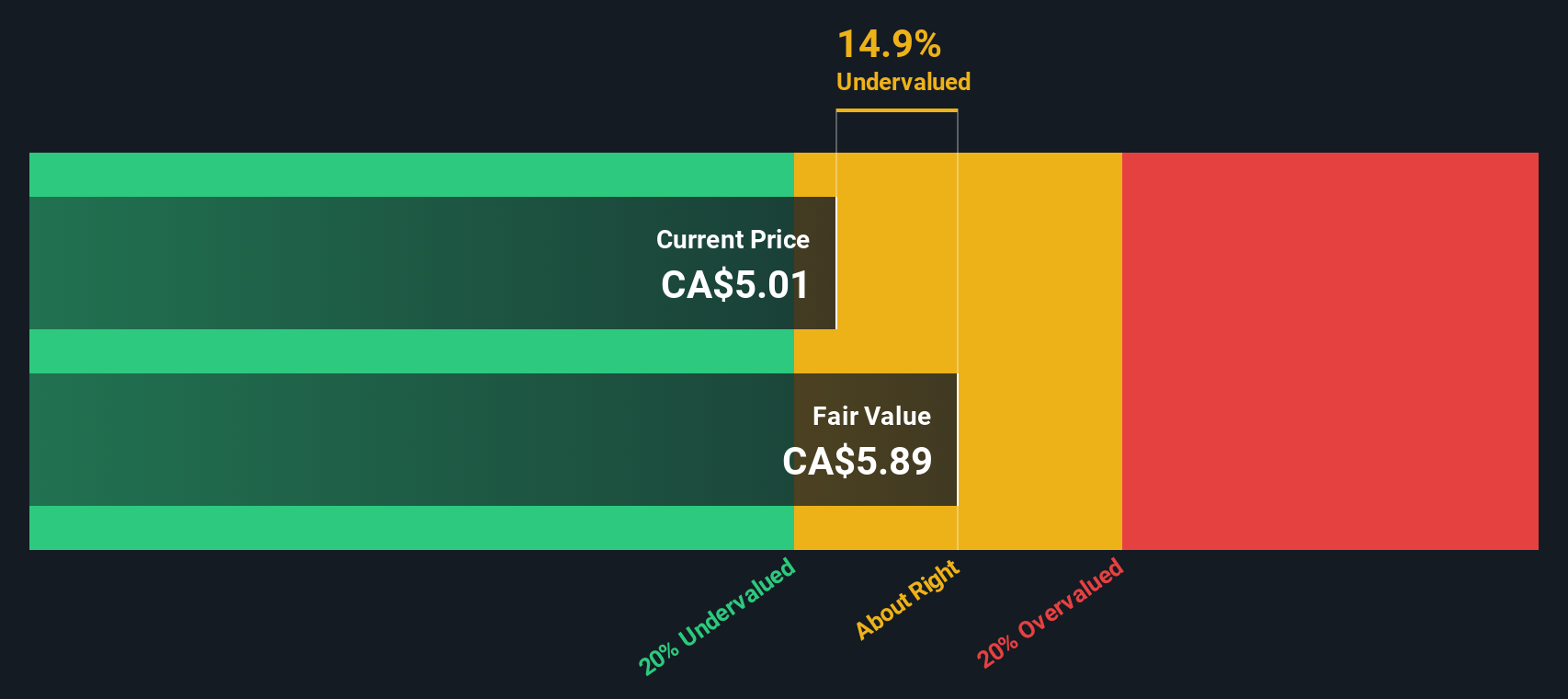

NorthWest Healthcare Properties Real Estate Investment Trust (TSX:NWH.UN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: NorthWest Healthcare Properties Real Estate Investment Trust operates as a global owner and manager of healthcare real estate, with a market capitalization of approximately CA$2.50 billion.

Operations: The company generates revenue primarily from the healthcare real estate industry, with a recent figure of CA$465.67 million. The gross profit margin has shown variability, reaching 82.39% in September 2021 before decreasing to 75.73% by December 2024. Operating expenses have fluctuated around CA$50-55 million in recent periods, while non-operating expenses have significantly impacted net income margins, leading to negative figures such as -64.37% in December 2024.

PE: -4.1x

NorthWest Healthcare Properties REIT, a smaller player in the real estate sector, shows potential for growth despite recent financial challenges. For the full year ending December 2024, sales dropped to C$462.4 million from C$508 million the previous year, with a net loss of C$299.76 million. However, insider confidence is evident as an independent trustee acquired 600,000 shares for approximately C$2.72 million recently. The company completed a significant debt refinancing with a C$500 million debenture offering to manage its liabilities better and maintain stability while continuing monthly dividends of C$0.03 per unit through April 2025.

Key Takeaways

- Reveal the 156 hidden gems among our Undervalued Global Small Caps With Insider Buying screener with a single click here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Troax Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:TROAX

Troax Group

Through its subsidiaries, produces and sells mesh panels in the Nordic region, the United Kingdom, North America, Europe, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor