Advertisement

- Australia

- /

- Specialty Stores

- /

- ASX:BBN

Is Baby Bunting Group Limited (ASX:BBN) A Smart Choice For Dividend Investors?

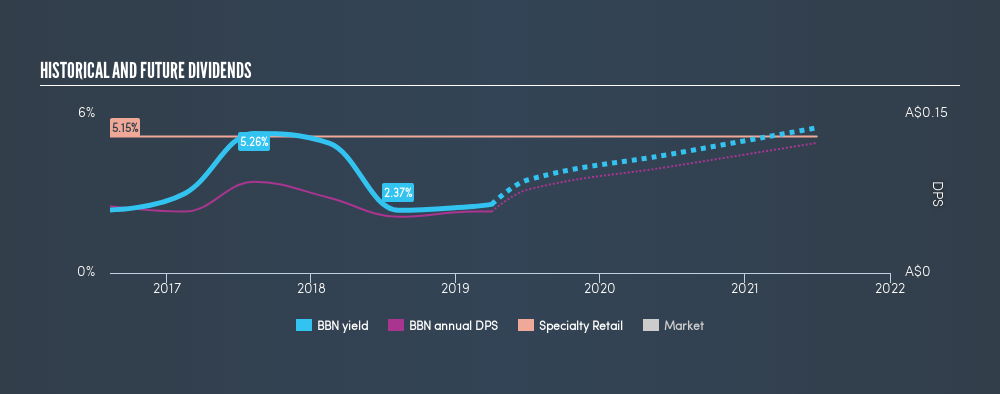

A sizeable part of portfolio returns can be produced by dividend stocks due to their contribution to compounding returns in the long run. Baby Bunting Group Limited (ASX:BBN) has paid a dividend to shareholders in the last few years. It currently yields 2.6%. Should it have a place in your portfolio? Let's take a look at Baby Bunting Group in more detail.

See our latest analysis for Baby Bunting Group

How I analyze a dividend stock

Whenever I am looking at a potential dividend stock investment, I always check these five metrics:

- Is it paying an annual yield above 75% of dividend payers?

- Does it consistently pay out dividends without missing a payment of significantly cutting payout?

- Has dividend per share amount increased over the past?

- Is is able to pay the current rate of dividends from its earnings?

- Will it have the ability to keep paying its dividends going forward?

Does Baby Bunting Group pass our checks?

The company currently pays out 74% of its earnings as a dividend, according to its trailing twelve-month data, meaning the dividend is sufficiently covered by earnings. In the near future, analysts are predicting a payout ratio of 70% which, assuming the share price stays the same, leads to a dividend yield of 4.5%. Furthermore, EPS should increase to A$0.12.

When thinking about whether a dividend is sustainable, another factor to consider is the cash flow. A company with strong cash flow, relative to earnings, can sometimes sustain a high pay out ratio.

If there is one thing that you want to be reliable in your life, it's dividend stocks and their constant income stream. The reality is that it is too early to consider Baby Bunting Group as a dividend investment. It has only been consistently paying dividends for 3 years, however, standard practice for reliable payers is to look for a 10-year minimum track record.

In terms of its peers, Baby Bunting Group has a yield of 2.6%, which is on the low-side for Specialty Retail stocks.

Next Steps:

Now you know to keep in mind the reason why investors should be careful investing in Baby Bunting Group for the dividend. But if you are not exclusively a dividend investor, the stock could still be an interesting investment opportunity. Given that this is purely a dividend analysis, you should always research extensively before deciding whether or not a stock is an appropriate investment for you. I always recommend analysing the company's fundamentals and underlying business before making an investment decision. There are three pertinent aspects you should further research:

- Future Outlook: What are well-informed industry analysts predicting for BBN’s future growth? Take a look at our free research report of analyst consensus for BBN’s outlook.

- Valuation: What is BBN worth today? Even if the stock is a cash cow, it's not worth an infinite price. The intrinsic value infographic in our free research report helps visualize whether BBN is currently mispriced by the market.

- Dividend Rockstars: Are there better dividend payers with stronger fundamentals out there? Check out our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:BBN

Baby Bunting Group

Engages in the retail of maternity and baby goods in Australia and New Zealand.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6927.9% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8148.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.3% undervalued

130 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

81 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7921.6% undervalued

918 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative