Advertisement

- Australia

- /

- Retail REITs

- /

- ASX:RGN

Should You Buy Shopping Centres Australasia Property Group (ASX:SCP) For Its Dividend?

Could Shopping Centres Australasia Property Group (ASX:SCP) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

With a goodly-sized dividend yield despite a relatively short payment history, investors might be wondering if Shopping Centres Australasia Property Group is a new dividend aristocrat in the making. It sure looks interesting on these metrics - but there's always more to the story . Some simple analysis can reduce the risk of holding Shopping Centres Australasia Property Group for its dividend, and we'll focus on the most important aspects below.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Shopping Centres Australasia Property Group paid out 84% of its profit as dividends, over the trailing twelve month period. It's paying out most of its earnings, which limits the amount that can be reinvested in the business. This may indicate limited need for further capital within the business, or highlight a commitment to paying a dividend.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. With a cash payout ratio of 102%, Shopping Centres Australasia Property Group's dividend payments are poorly covered by cash flow. Shopping Centres Australasia Property Group paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough free cash flow to cover the dividend. Cash is king, as they say, and were Shopping Centres Australasia Property Group to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

It is worth considering that Shopping Centres Australasia Property Group is a Real Estate Investment Trust (REIT). REITs have different rules governing their payments, and are often required to pay out a high portion of their earnings to investors.

Dividend Volatility

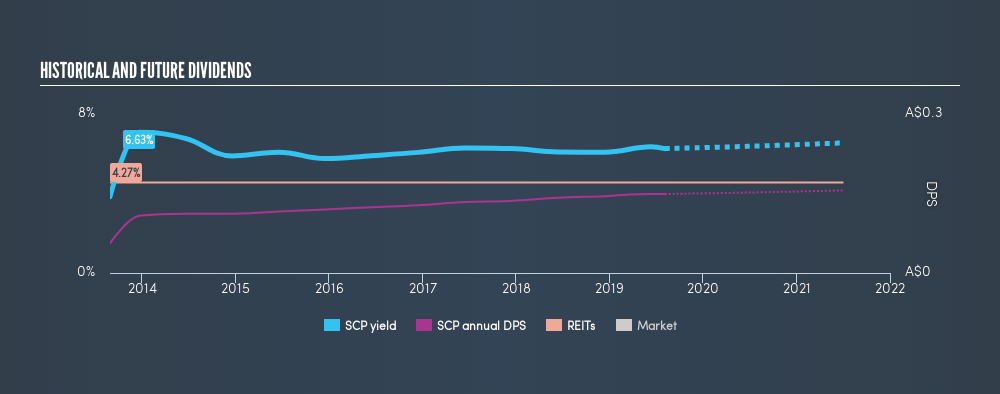

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Looking at the data, we can see that Shopping Centres Australasia Property Group has been paying a dividend for the past six years. The dividend has been quite stable over the past six years, which is great to see - although we usually like to see the dividend maintained for a decade before giving it full marks, though. During the past six-year period, the first annual payment was AU$0.056 in 2013, compared to AU$0.15 last year. This works out to be a compound annual growth rate (CAGR) of approximately 18% a year over that time.

We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

Dividend Growth Potential

Examining whether the dividend is affordable and stable is important. However, it's also important to assess if earnings per share (EPS) are growing. Growing EPS can help maintain or increase the purchasing power of the dividend over the long run. Earnings have grown at around 5.6% a year for the past five years, which is better than seeing them shrink! EPS have been growing at a reasonable rate, although with most of the profits being paid out to shareholders, we question if the company will be able to keep growing its dividends in the future.

We'd also point out that Shopping Centres Australasia Property Group issued a meaningful number of new shares in the past year. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. First, the company has a payout ratio that was within an average range for most dividend stocks, but it paid out virtually all of its generated cash flow. Unfortunately, there hasn't been any earnings growth, and the company's dividend history has been too short for us to evaluate the consistency of the dividend. In summary, Shopping Centres Australasia Property Group has a number of shortcomings that we'd find it hard to get past. Things could change, but we think there are a number of better ideas out there.

Earnings growth generally bodes well for the future value of company dividend payments. See if the 6 Shopping Centres Australasia Property Group analysts we track are forecasting continued growth with our free report on analyst estimates for the company.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:RGN

Region Group

An internally managed real estate investment trust (REIT) with 92 convenience-based retail properties, valued at $4,368 million.

Average dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor