Advertisement

- Australia

- /

- Retail REITs

- /

- ASX:DXC

APN Convenience Retail REIT (ASX:AQR) Stock Has Shown Weakness Lately But Financials Look Strong: Should Prospective Shareholders Make The Leap?

APN Convenience Retail REIT (ASX:AQR) has had a rough three months with its share price down 3.6%. However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. Particularly, we will be paying attention to APN Convenience Retail REIT's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

Check out our latest analysis for APN Convenience Retail REIT

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for APN Convenience Retail REIT is:

12% = AU$47m ÷ AU$408m (Based on the trailing twelve months to December 2020).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each A$1 of shareholders' capital it has, the company made A$0.12 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

APN Convenience Retail REIT's Earnings Growth And 12% ROE

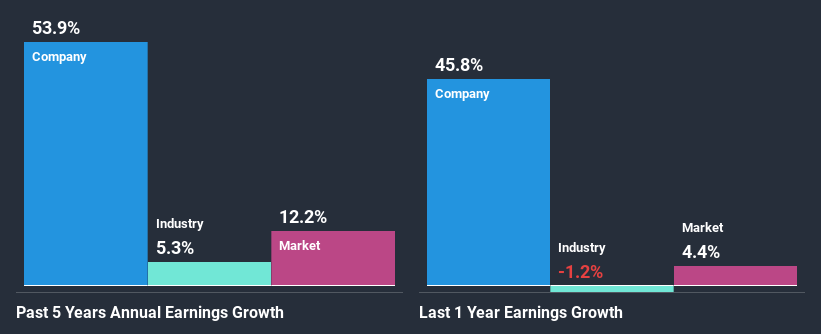

To begin with, APN Convenience Retail REIT seems to have a respectable ROE. Further, the company's ROE compares quite favorably to the industry average of 6.7%. This probably laid the ground for APN Convenience Retail REIT's significant 54% net income growth seen over the past five years. We reckon that there could also be other factors at play here. For instance, the company has a low payout ratio or is being managed efficiently.

We then compared APN Convenience Retail REIT's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 5.3% in the same period.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Has the market priced in the future outlook for AQR? You can find out in our latest intrinsic value infographic research report.

Is APN Convenience Retail REIT Making Efficient Use Of Its Profits?

APN Convenience Retail REIT seems to be paying out most of its income as dividends judging by its three-year median payout ratio of 94%, meaning the company retains only 6.1% of its income. However, this is typical for REITs as they are often required by law to distribute most of their earnings. Regardless, this hasn't hampered its ability to grow as we saw earlier.

Besides, APN Convenience Retail REIT has been paying dividends over a period of three years. This shows that the company is committed to sharing profits with its shareholders. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 101%. Regardless, APN Convenience Retail REIT's ROE is speculated to decline to 6.7% despite there being no anticipated change in its payout ratio.

Conclusion

On the whole, we feel that APN Convenience Retail REIT's performance has been quite good. Especially the high ROE, Which has contributed to the impressive growth seen in earnings. Despite the company reinvesting only a small portion of its profits, it still has managed to grow its earnings so that is appreciable. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you’re looking to trade APN Convenience Retail REIT, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:DXC

Dexus Convenience Retail REIT

Dexus Convenience Retail REIT (ASX code: DXC) is a listed Australian real estate investment trust which owns high quality Australian service stations and convenience retail assets.

Moderate growth potential with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor