Advertisement

Undervalued Small Caps With Insider Activity In Asian Markets June 2025

Simply Wall St

Reviewed by Simply Wall St

As tensions in the Middle East have led to a surge in oil prices, global markets are experiencing heightened volatility, with smaller-cap indexes such as the S&P MidCap 400 and Russell 2000 facing notable declines. In this environment of uncertainty, identifying promising small-cap stocks in Asian markets requires careful consideration of economic indicators and market sentiment that may impact these companies' growth potential.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.3x | 1.0x | 38.61% | ★★★★★★ |

| Credit Corp Group | 8.2x | 1.9x | 41.07% | ★★★★★★ |

| Infomedia | 29.6x | 3.3x | 36.92% | ★★★★★☆ |

| East West Banking | 3.0x | 0.7x | 35.77% | ★★★★★☆ |

| Dicker Data | 18.8x | 0.6x | -15.35% | ★★★★☆☆ |

| Eureka Group Holdings | 18.2x | 5.6x | 23.24% | ★★★★☆☆ |

| Atturra | 26.9x | 1.1x | 36.52% | ★★★★☆☆ |

| Sing Investments & Finance | 7.4x | 3.7x | 38.61% | ★★★★☆☆ |

| PWR Holdings | 33.5x | 4.6x | 26.03% | ★★★☆☆☆ |

| AInnovation Technology Group | NA | 2.4x | 47.10% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

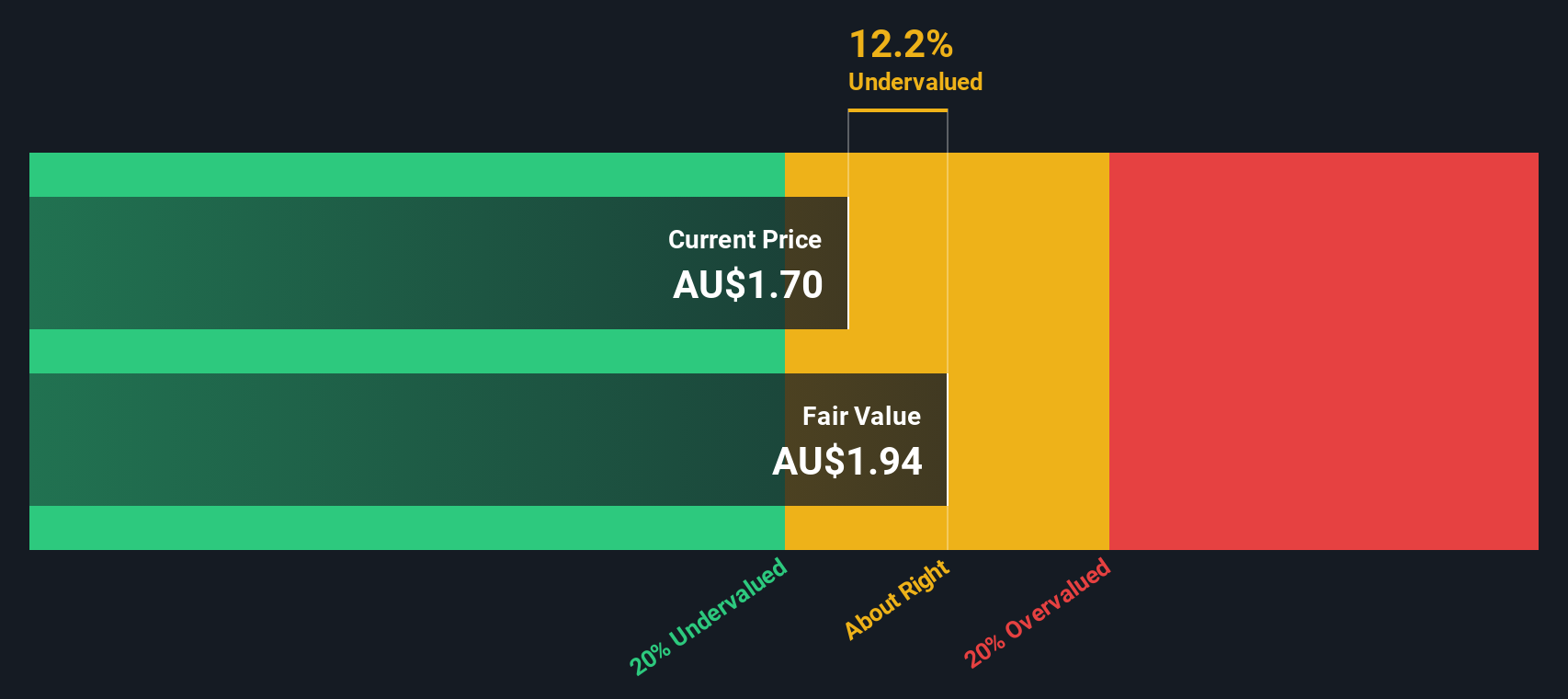

Nine Entertainment Holdings (ASX:NEC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Nine Entertainment Holdings operates as a diversified media company in Australia, engaging in broadcasting, publishing, and digital platforms with a market capitalization of approximately A$3.5 billion.

Operations: Nine Entertainment Holdings generates revenue primarily from Broadcasting, Publishing, Stan, and Domain Group segments. The company's gross profit margin has fluctuated over the years, reaching 26.43% in September 2022 before declining to 16.73% by December 2024. Operating expenses have varied but remained a significant component of overall costs alongside non-operating expenses and depreciation & amortization (D&A) expenses.

PE: 28.4x

Nine Entertainment Holdings, a small player in the Asian market, recently showcased its strategic initiatives at the Adobe Summit 2025. Despite relying on higher-risk external borrowing for funding, insider confidence is evident with recent share purchases between January and March 2025. Earnings are projected to grow by A$20 million annually over the next few years. This growth potential positions them as an interesting option for those exploring smaller companies in Asia's dynamic media landscape.

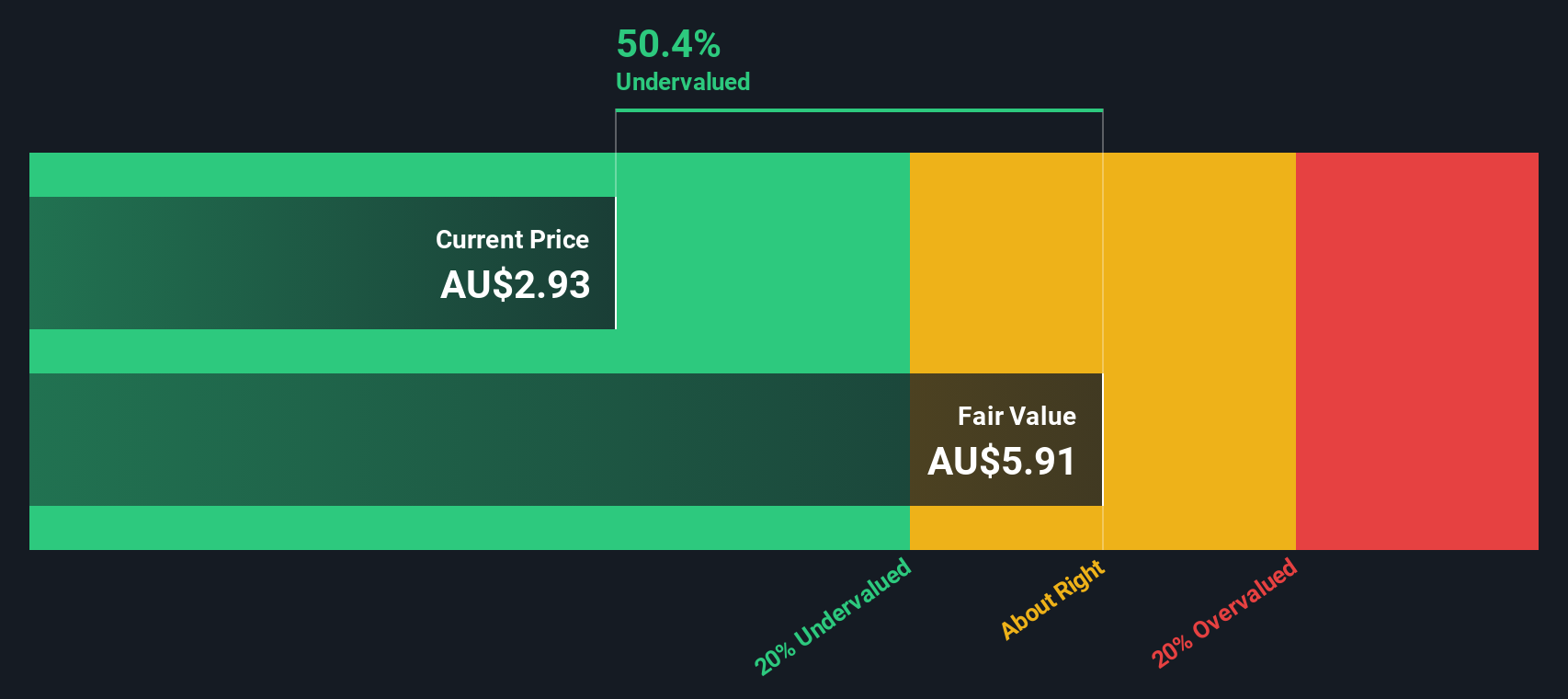

Ridley (ASX:RIC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Ridley operates in the agribusiness sector, focusing on the production and supply of bulk stockfeeds and packaged ingredients, with a market capitalization of A$0.91 billion.

Operations: The company's primary revenue streams are Bulk Stockfeeds and Packaged/Ingredients, contributing significantly to its total revenue. Over the observed periods, the gross profit margin has shown fluctuations, reaching 9.22% as of December 31, 2024. Operating expenses and non-operating expenses have also varied across different time frames, impacting net income margins which were recorded at 3.16% in the same period.

PE: 26.0x

Ridley, a small company in Asia, recently completed a A$50 million fixed-income offering and filed for an equity offering worth A$125.68 million. Insiders have shown confidence by purchasing shares, indicating potential value recognition despite past shareholder dilution. The company's funding relies entirely on external borrowing, which adds risk compared to customer deposits. However, with earnings projected to grow by 16% annually, Ridley presents an intriguing opportunity for investors eyeing growth in the region.

- Navigate through the intricacies of Ridley with our comprehensive valuation report here.

Understand Ridley's track record by examining our Past report.

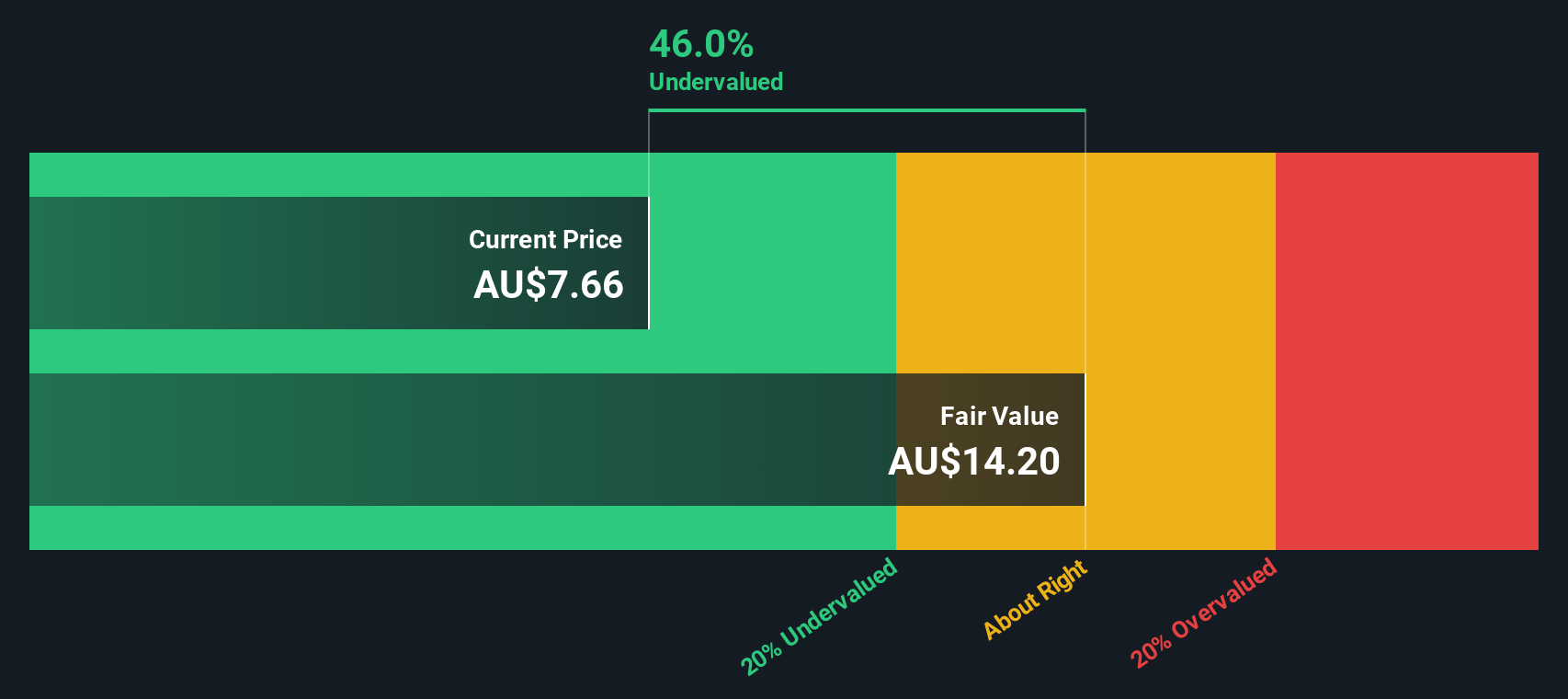

Smartgroup (ASX:SIQ)

Simply Wall St Value Rating: ★★★★★☆

Overview: Smartgroup is a company that provides outsourced administration and vehicle services, with a market cap of A$1.02 billion.

Operations: Smartgroup generates revenue primarily from Outsourced Administration (OA), which is its largest segment, alongside Vehicle Services (VS). The company's cost structure includes significant costs of goods sold and operating expenses, with a notable portion allocated to general and administrative expenses. Over the observed periods, Smartgroup's net income margin has shown an upward trend, reaching 24.72% by the end of 2024.

PE: 12.9x

Smartgroup, a notable player in the small-cap sector, shows signs of being undervalued with insider confidence reflected by their Independent Non-Executive Chairman's purchase of 25,000 shares for A$173,750 in April 2025. This move suggests potential optimism about future prospects. Despite relying on higher-risk external borrowing for funding, the company forecasts a steady earnings growth of 3.4% annually. Recent participation at the Macquarie Australia Conference and upcoming earnings release could provide further insights into its trajectory within Asia's competitive market landscape.

- Delve into the full analysis valuation report here for a deeper understanding of Smartgroup.

Assess Smartgroup's past performance with our detailed historical performance reports.

Turning Ideas Into Actions

- Dive into all 59 of the Undervalued Asian Small Caps With Insider Buying we have identified here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:RIC

Ridley

Engages in the provision of animal nutrition solutions in Australia the United States, New Zealand, and Thailand.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor