Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:PLL

We Think Piedmont Lithium (ASX:PLL) Can Easily Afford To Drive Business Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

Given this risk, we thought we'd take a look at whether Piedmont Lithium (ASX:PLL) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

View our latest analysis for Piedmont Lithium

SWOT Analysis for Piedmont Lithium

Strength

- Debt is well covered by earnings.

Weakness

- Shareholders have been diluted in the past year.

Opportunity

- Expected to breakeven next year.

Threat

- Debt is not well covered by operating cash flow.

- Has less than 3 years of cash runway based on current free cash flow.

How Long Is Piedmont Lithium's Cash Runway?

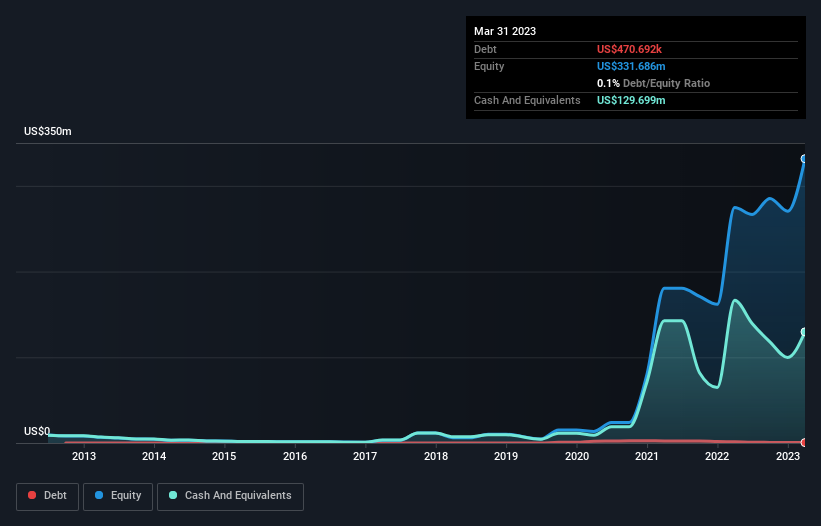

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at March 2023, Piedmont Lithium had cash of US$130m and such minimal debt that we can ignore it for the purposes of this analysis. Importantly, its cash burn was US$66m over the trailing twelve months. So it had a cash runway of about 2.0 years from March 2023. Notably, however, analysts think that Piedmont Lithium will break even (at a free cash flow level) before then. In that case, it may never reach the end of its cash runway. You can see how its cash balance has changed over time in the image below.

How Is Piedmont Lithium's Cash Burn Changing Over Time?

Because Piedmont Lithium isn't currently generating revenue, we consider it an early-stage business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. With the cash burn rate up 5.7% in the last year, it seems that the company is ratcheting up investment in the business over time. That's not necessarily a bad thing, but investors should be mindful of the fact that will shorten the cash runway. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Piedmont Lithium Raise More Cash Easily?

Since its cash burn is increasing (albeit only slightly), Piedmont Lithium shareholders should still be mindful of the possibility it will require more cash in the future. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$1.2b, Piedmont Lithium's US$66m in cash burn equates to about 5.5% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

How Risky Is Piedmont Lithium's Cash Burn Situation?

It may already be apparent to you that we're relatively comfortable with the way Piedmont Lithium is burning through its cash. In particular, we think its cash burn relative to its market cap stands out as evidence that the company is well on top of its spending. Although its increasing cash burn does give us reason for pause, the other metrics we discussed in this article form a positive picture overall. There's no doubt that shareholders can take a lot of heart from the fact that analysts are forecasting it will reach breakeven before too long. Taking all the factors in this report into account, we're not at all worried about its cash burn, as the business appears well capitalized to spend as needs be. On another note, we conducted an in-depth investigation of the company, and identified 2 warning signs for Piedmont Lithium (1 is potentially serious!) that you should be aware of before investing here.

Of course Piedmont Lithium may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:PLL

Piedmont Lithium

A development stage company, engages in the exploration and development of resource projects in the United States.

Adequate balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor