Uncovering Emerald Resources And Two Other Promising Small Cap Gems In Australia

Reviewed by Simply Wall St

In the dynamic landscape of the Australian market, the ASX200 has shown modest gains with a 0.12% increase, highlighting strong performances in sectors like Real Estate and Telecommunications while Materials and Energy have lagged behind. Amidst these shifts, small-cap stocks continue to capture investor interest for their potential growth opportunities, especially as companies like Emerald Resources make significant strides by clearing debts and advancing projects. Identifying promising small-cap gems involves looking for companies that demonstrate resilience and strategic advancements in challenging market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.78% | 4.30% | ★★★★★★ |

| Schaffer | 25.47% | 6.03% | -5.20% | ★★★★★★ |

| Fiducian Group | NA | 9.97% | 7.85% | ★★★★★★ |

| Hearts and Minds Investments | NA | 47.09% | 49.82% | ★★★★★★ |

| Djerriwarrh Investments | 1.14% | 8.17% | 7.54% | ★★★★★★ |

| Red Hill Minerals | NA | 95.16% | 40.06% | ★★★★★★ |

| MFF Capital Investments | 0.69% | 28.52% | 31.31% | ★★★★★☆ |

| Lycopodium | 6.89% | 16.56% | 32.73% | ★★★★★☆ |

| Carlton Investments | 0.02% | 4.45% | 3.97% | ★★★★★☆ |

| K&S | 20.24% | 1.58% | 25.54% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

Emerald Resources (ASX:EMR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Emerald Resources NL focuses on the exploration and development of mineral reserves in Cambodia and Australia, with a market capitalization of approximately A$2.47 billion.

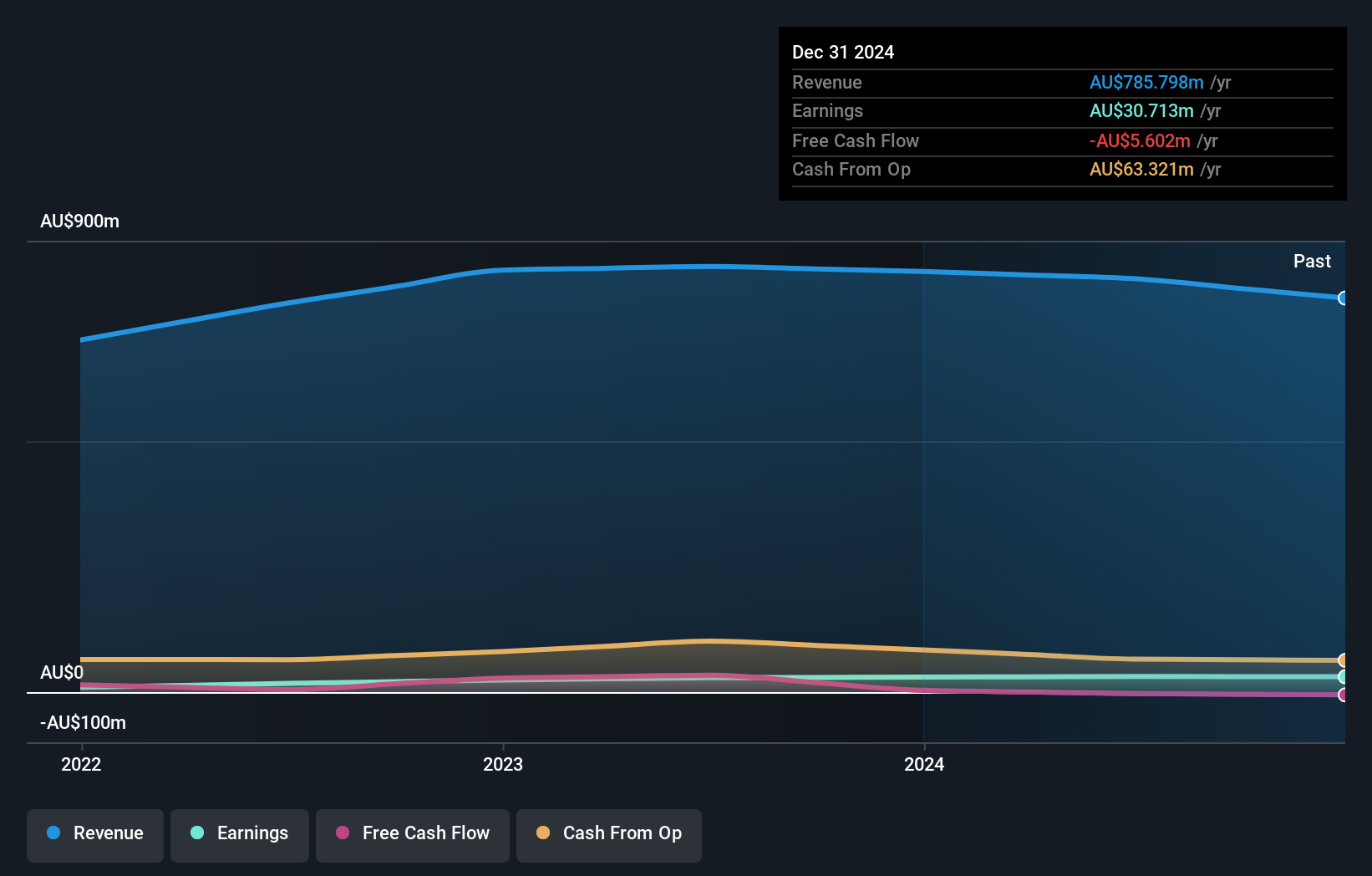

Operations: Emerald Resources generates revenue primarily from mine operations, amounting to A$427.32 million. The company has a market capitalization of approximately A$2.47 billion.

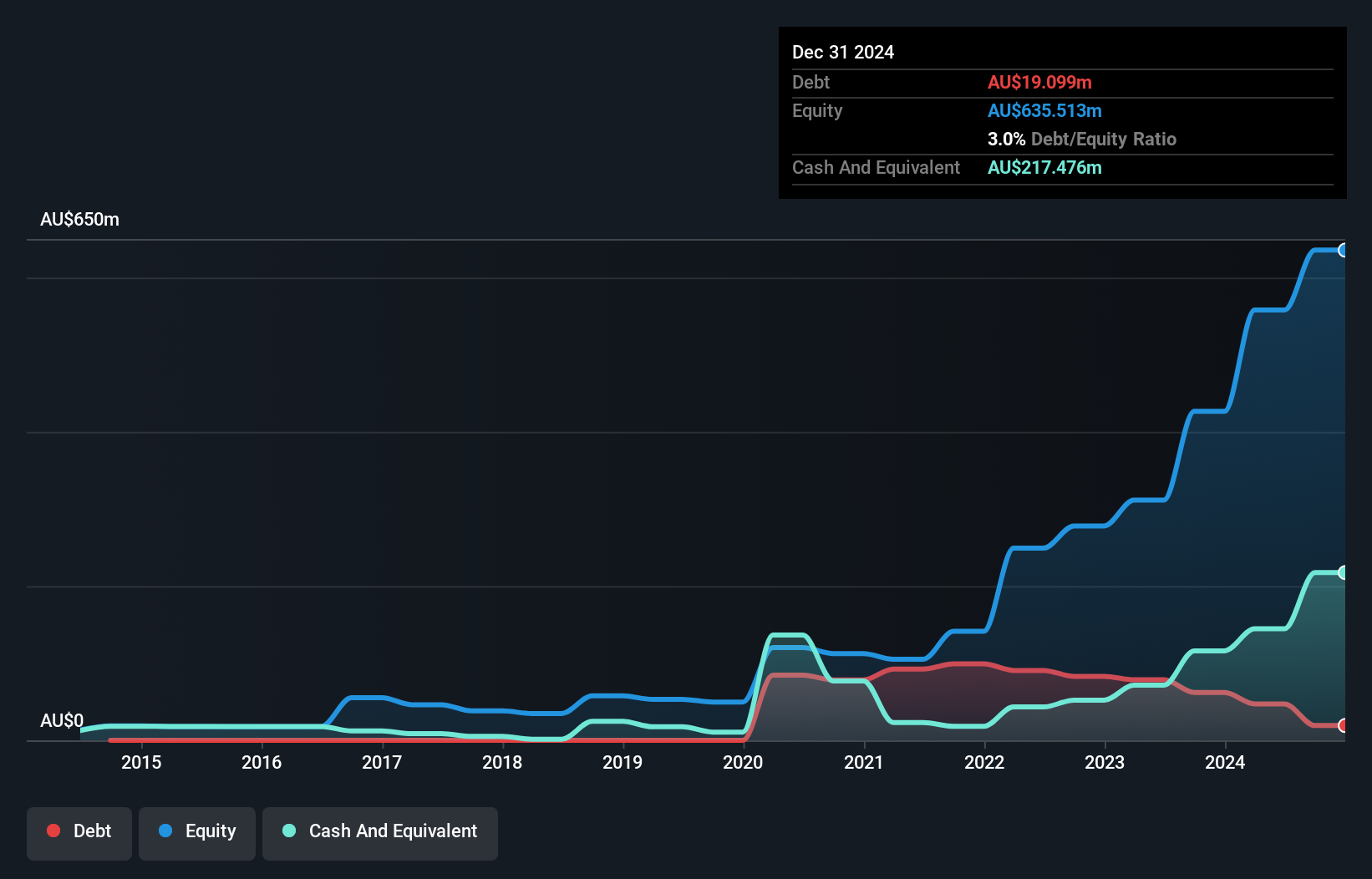

Emerald Resources, a nimble player in the mining sector, has been making waves with its impressive financial performance and strategic improvements at the Okvau Gold Mine. The company reported earnings growth of 32% last year, outpacing the industry average of 0.7%. With a debt-to-equity ratio rising to just 3% over five years and more cash than total debt, financial health seems robust. Recent quarterly gold production hit record levels at Okvau, surpassing guidance with 31,888 ounces produced. Trading at a significant discount to estimated fair value suggests potential upside for investors eyeing this dynamic miner.

- Click here and access our complete health analysis report to understand the dynamics of Emerald Resources.

Assess Emerald Resources' past performance with our detailed historical performance reports.

K&S (ASX:KSC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: K&S Corporation Limited operates in the transportation and logistics, warehousing, and fuel distribution sectors across Australia and New Zealand, with a market capitalization of approximately A$465.29 million.

Operations: K&S derives its revenue primarily from Australian Transport (A$553.12 million) and Fuel (A$213.29 million), with a smaller contribution from New Zealand Transport (A$74.99 million).

K&S Corporation, a smaller player in the logistics sector, has demonstrated high-quality earnings with a solid 25.5% annual growth over the past five years. Despite an increase in its debt to equity ratio from 9.9% to 20.2%, its interest payments are well covered by EBIT at 9.5 times, indicating strong financial health. The company is trading at about 14.8% below estimated fair value, offering potential upside for investors seeking undervalued opportunities. Recently, K&S announced a share repurchase program targeting small shareholders at A$3.60 per share and reported net income of A$16 million for the half-year ended December 2024, slightly down from A$16.6 million previously.

- Delve into the full analysis health report here for a deeper understanding of K&S.

Gain insights into K&S' past trends and performance with our Past report.

Ora Banda Mining (ASX:OBM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Ora Banda Mining Limited focuses on the exploration, operation, and development of mineral properties in Australia with a market capitalization of approximately A$1.97 billion.

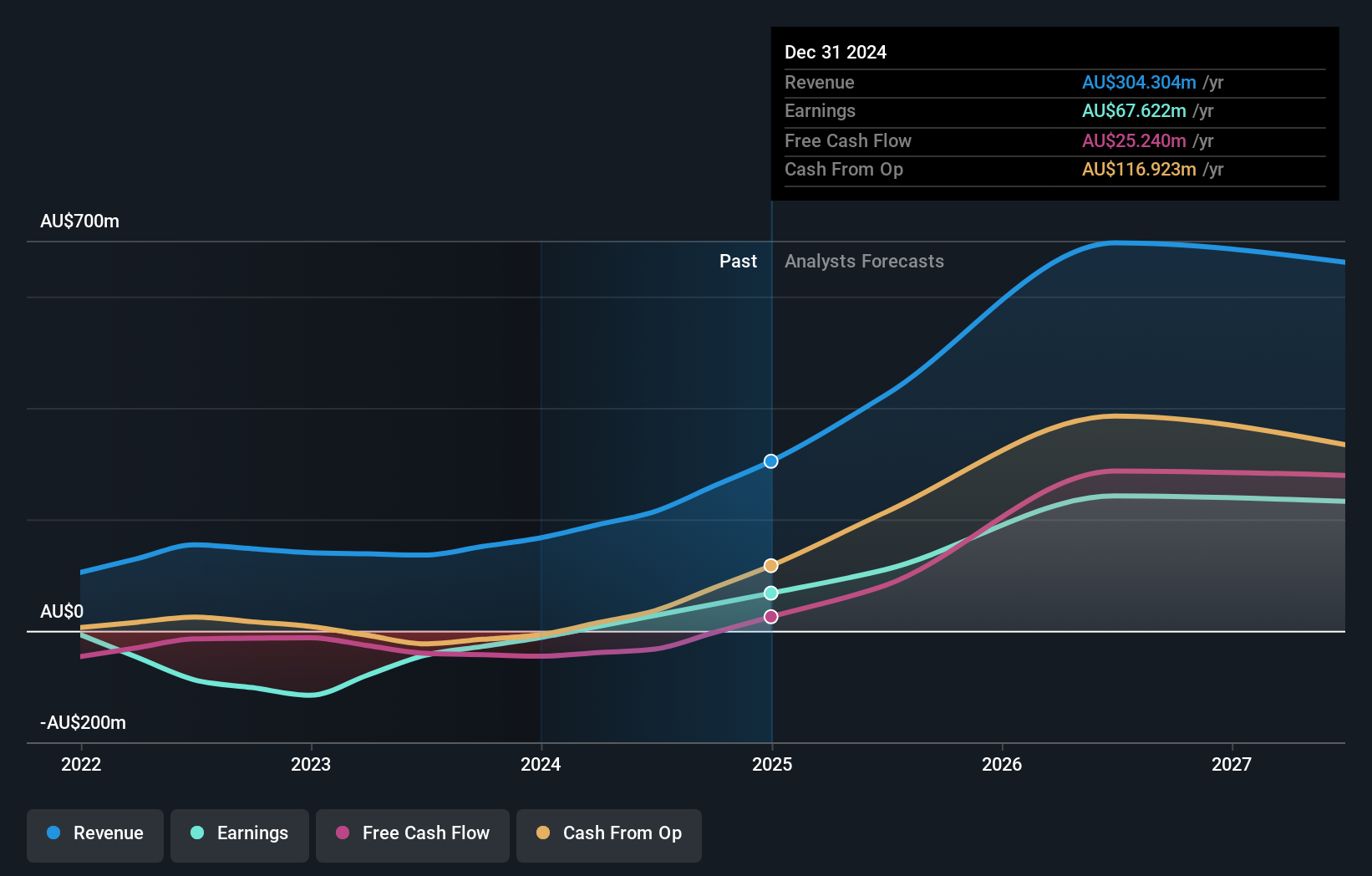

Operations: The primary revenue stream for Ora Banda Mining is gold mining, generating A$304.30 million. The company's market capitalization stands at approximately A$1.97 billion, reflecting its scale in the mineral exploration and development sector.

Ora Banda Mining, a dynamic player in the mining sector, has recently been added to the S&P/ASX 300 and Small Ordinaries Indexes, signaling its growing prominence. The company reported a significant boost in sales for the half-year ending December 2024, reaching A$186.42 million from A$96.35 million previously. Net income saw an impressive rise to A$50.84 million from A$10.79 million year-over-year. With earnings per share increasing to A$0.028 from A$0.0063, Ora Banda also secured a revolving credit facility of A$50 million with major banks, bolstering liquidity beyond A$100 million alongside existing cash reserves of $57.8 million as of December 2024.

Seize The Opportunity

- Reveal the 51 hidden gems among our ASX Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if K&S might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:KSC

K&S

Engages in the transportation and logistics, warehousing, and fuel distribution businesses in Australia and New Zealand.

Excellent balance sheet second-rate dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion