Stock Analysis

- Australia

- /

- Metals and Mining

- /

- ASX:EMR

ASX Growth Companies With High Insider Ownership In May 2024

Reviewed by Simply Wall St

As the ASX200 navigates a challenging session with a notable dip, sectors like IT and healthcare are showing resilience with positive movements. This mixed market backdrop sets an interesting stage for investors looking at growth companies with high insider ownership in Australia. In such fluctuating market conditions, companies with substantial insider ownership can be appealing as they often demonstrate alignment between management's interests and those of shareholders, potentially offering stability amidst market volatility.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Cettire (ASX:CTT) | 28.7% | 29.9% |

| Gratifii (ASX:GTI) | 15.6% | 112.4% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Doctor Care Anywhere Group (ASX:DOC) | 28.4% | 96.4% |

| Alpha HPA (ASX:A4N) | 28.3% | 95.9% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| Liontown Resources (ASX:LTR) | 16.4% | 63.9% |

| Plenti Group (ASX:PLT) | 12.6% | 68.5% |

| Chrysos (ASX:C79) | 21.4% | 57.5% |

Underneath we present a selection of stocks filtered out by our screen.

Emerald Resources (ASX:EMR)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Emerald Resources NL is a company focused on the exploration and development of mineral reserves in Cambodia and Australia, with a market capitalization of approximately A$2.57 billion.

Operations: The primary revenue segment for the company, generating A$339.32 million, comes from mine operations.

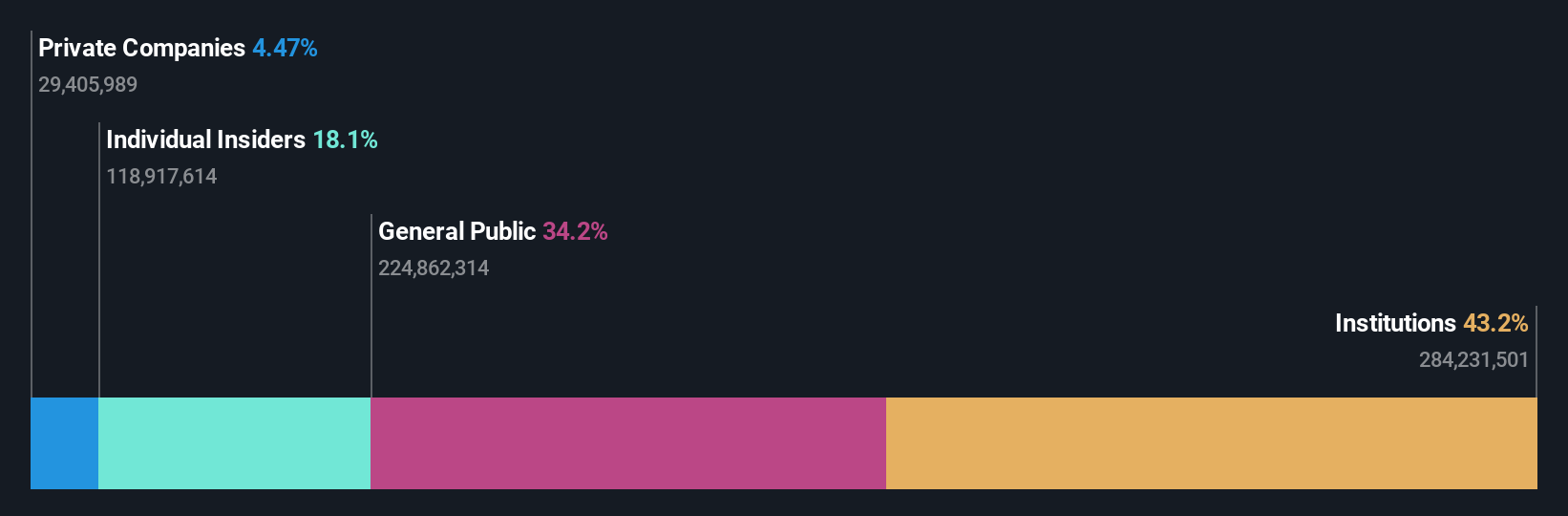

Insider Ownership: 18.5%

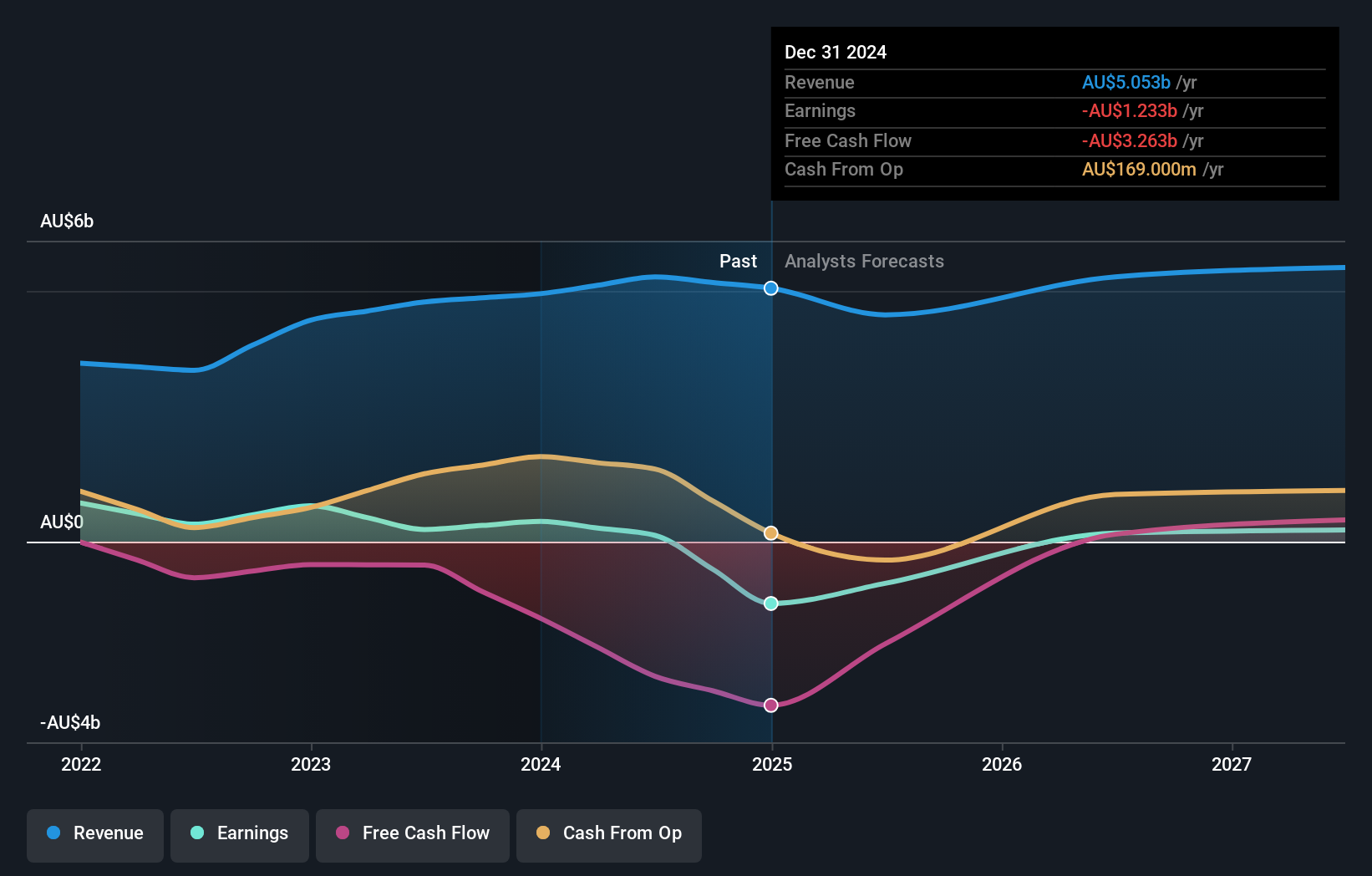

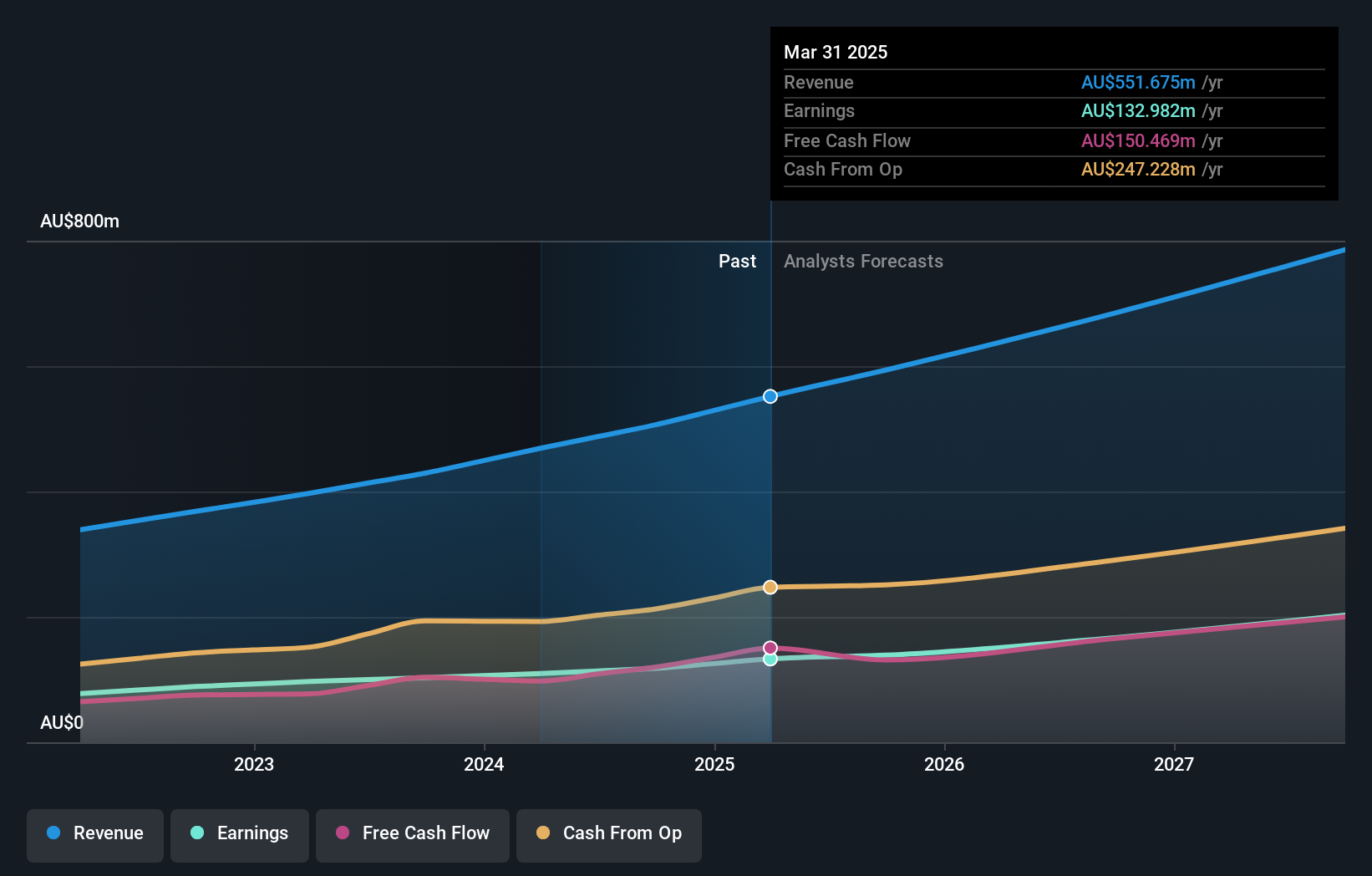

Emerald Resources is trading at a significant discount, valued 71.9% below its estimated fair value, suggesting potential for growth-oriented investors. The company's revenue and earnings are forecasted to grow by 19.4% and 22.76% per year respectively, outpacing the Australian market averages of 5% and 13.7%. Despite this promising outlook, concerns include shareholder dilution over the past year and a low projected return on equity of 17.9%. Recent financials showed strong performance with substantial increases in sales and net income compared to the previous year.

- Navigate through the intricacies of Emerald Resources with our comprehensive analyst estimates report here.

- Upon reviewing our latest valuation report, Emerald Resources' share price might be too pessimistic.

Mineral Resources (ASX:MIN)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Mineral Resources Limited, along with its subsidiaries, functions as a mining services company across Australia, Asia, and other international markets, boasting a market capitalization of approximately A$15.30 billion.

Operations: The company generates revenue from lithium (A$1.60 billion), iron ore (A$2.50 billion), and mining services (A$2.82 billion).

Insider Ownership: 11.6%

Mineral Resources Limited is poised for robust growth with revenue and earnings forecasted to expand by 10.7% and 29.2% per year, respectively, outstripping the Australian market averages. Despite trading at a substantial 28.8% below its estimated fair value, concerns linger over its profit margins which have declined from last year and interest payments that are not well covered by earnings. The high forecast return on equity of 21.7% in three years underscores potential upside amidst these challenges.

- Take a closer look at Mineral Resources' potential here in our earnings growth report.

- The valuation report we've compiled suggests that Mineral Resources' current price could be inflated.

Technology One (ASX:TNE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Technology One Limited is a company that develops, markets, sells, implements, and supports integrated enterprise business software solutions both in Australia and internationally, with a market capitalization of approximately A$5.81 billion.

Operations: The company generates revenue through three primary segments: software sales contributing A$317.24 million, corporate services at A$83.83 million, and consulting services totaling A$68.13 million.

Insider Ownership: 12.3%

Technology One Limited, an Australian software company, exhibits solid growth prospects with revenue and earnings increasing by 11.3% and 13.77% per year respectively, outpacing the broader Australian market. Despite its high price-to-earnings ratio of A$53.1x compared to the industry average of A$61.1x, it maintains a robust forecast return on equity of 32.8%. Recent financial results showed a significant rise in half-year revenue to A$240.83 million and net income to A$48 million, reflecting ongoing operational success.

- Unlock comprehensive insights into our analysis of Technology One stock in this growth report.

- In light of our recent valuation report, it seems possible that Technology One is trading beyond its estimated value.

Summing It All Up

- Delve into our full catalog of 90 Fast Growing ASX Companies With High Insider Ownership here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Emerald Resources is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:EMR

Emerald Resources

Engages in the exploration and development of mineral reserves in Cambodia and Australia.

Solid track record with excellent balance sheet.