Advertisement

Want to participate in a short research study? Help shape the future of investing tools and receive a $20 prize!

Taking the occasional loss comes part and parcel with investing on the stock market. And there's no doubt that Lodestar Minerals Limited (ASX:LSR) stock has had a really bad year. The share price has slid 65% in that time. Even if you look out three years, the returns are still disappointing, with the share price down (the share price is down 65%) in that time. Shareholders have had an even rougher run lately, with the share price down 50%.

View our latest analysis for Lodestar Minerals

With just AU$87,272 worth of revenue in twelve months, we don't think the market Lodestar Minerals has proven its business plan. This state of affairs suggests that venture capitalists won't provide funds on attractive terms. So it seems that the investors more focused on would could be, than paying attention to the current revenues (or lack thereof). We'd posit some have faith that Lodestar Minerals will find or develop a valuable new mine before too long.

Companies that lack both meaningful revenue and profits are usually considered high risk. There is almost always a chance they will need to raise more capital, and their progress - and share price - will dictate how dilutive that is to current holders. While some companies like this go on to deliver on their plan, making good money for shareholders, many end in painful losses and eventual de-listing. Some Lodestar Minerals investors have already had a taste of the bitterness stocks like this can leave in the mouth.

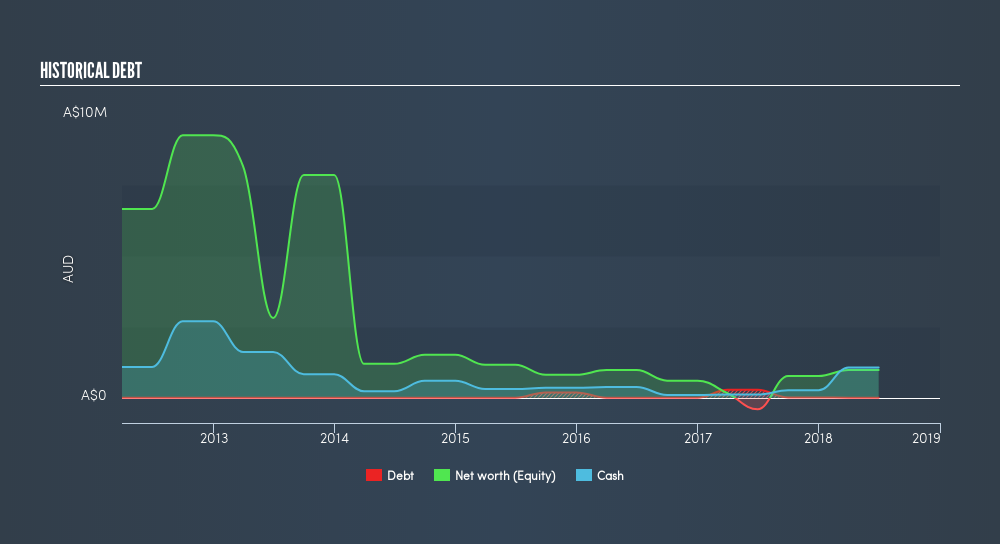

Lodestar Minerals had net cash of just AU$841k when it last reported (June 2018). So if it hasn't remedied the situation already, it will almost certainly have to raise more capital soon. That probably explains why the share price is down 65% in the last year. You can see in the image below, how Lodestar Minerals's cash and debt levels have changed over time (click to see the values).

Of course, the truth is that it is hard to value companies without much revenue or profit. What if insiders are ditching the stock hand over fist? I would not feel more nervous about the company if that were so. It only takes a moment for you to check whether we have identified any insider sales recently.

What about the Total Shareholder Return (TSR)?

Investors should note that there's a difference between Lodestar Minerals's total shareholder return (TSR) and its share price change, which we've covered above. Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. We note that Lodestar Minerals's TSR, at -65% is higher than its share price rise of -65%. When you consider it hasn't been paying a dividend, this data suggests shareholders may have had the opportunity to acquire attractively priced shares in the business.

A Different Perspective

While the broader market gained around 8.4% in the last year, Lodestar Minerals shareholders lost 65%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 4.9% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. You could get a better understanding of Lodestar Minerals's growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Of course Lodestar Minerals may not be the best stock to buy. So you may wish to see this freecollection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:LSR

Lodestar Minerals

Engages in the exploration and evaluation of mineral properties in Australia.

Medium-low with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor