Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Lucapa Diamond Company Limited (ASX:LOM) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Lucapa Diamond

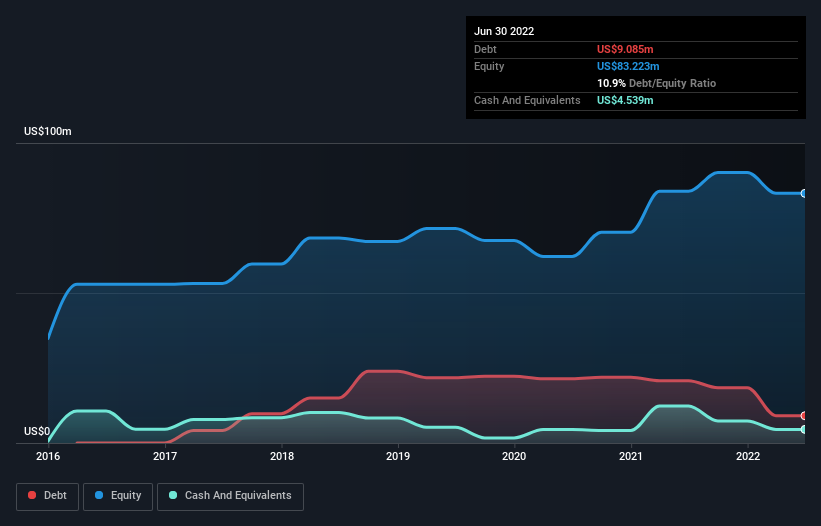

How Much Debt Does Lucapa Diamond Carry?

As you can see below, Lucapa Diamond had US$9.09m of debt at June 2022, down from US$20.7m a year prior. However, it also had US$4.54m in cash, and so its net debt is US$4.55m.

How Strong Is Lucapa Diamond's Balance Sheet?

According to the last reported balance sheet, Lucapa Diamond had liabilities of US$14.4m due within 12 months, and liabilities of US$3.83m due beyond 12 months. Offsetting these obligations, it had cash of US$4.54m as well as receivables valued at US$13.5m due within 12 months. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that Lucapa Diamond's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the US$50.9m company is struggling for cash, we still think it's worth monitoring its balance sheet. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Lucapa Diamond will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Lucapa Diamond wasn't profitable at an EBIT level, but managed to grow its revenue by 33%, to US$23m. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

While we can certainly appreciate Lucapa Diamond's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. Its EBIT loss was a whopping US$16m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$19m in negative free cash flow over the last twelve months. So in short it's a really risky stock. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Lucapa Diamond (of which 1 makes us a bit uncomfortable!) you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:LOM

Lucapa Diamond

Engages in the exploration, evaluation, mining, and development of diamond projects in Africa and Australia.

Excellent balance sheet moderate.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor