Stock Analysis

- Australia

- /

- Specialty Stores

- /

- ASX:CTT

Discover Three ASX Growth Companies With High Insider Stakes

Reviewed by Simply Wall St

Amidst the fluctuating Australian market, as evidenced by recent movements in the ASX200 following the Reserve Bank of Australia's latest minutes, investors continue to navigate through varying economic signals. In such a landscape, growth companies with high insider ownership can offer an intriguing opportunity for those looking to align with management's vested interests in their company’s success. In today's uncertain market environment, stocks with significant insider stakes might be particularly compelling as they suggest confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Cettire (ASX:CTT) | 28.7% | 26.7% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Change Financial (ASX:CCA) | 26.6% | 76.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| Biome Australia (ASX:BIO) | 34.5% | 114.4% |

| Liontown Resources (ASX:LTR) | 16.4% | 52.2% |

| CardieX (ASX:CDX) | 12.2% | 115.3% |

| Argosy Minerals (ASX:AGY) | 14.5% | 129.6% |

Let's explore several standout options from the results in the screener.

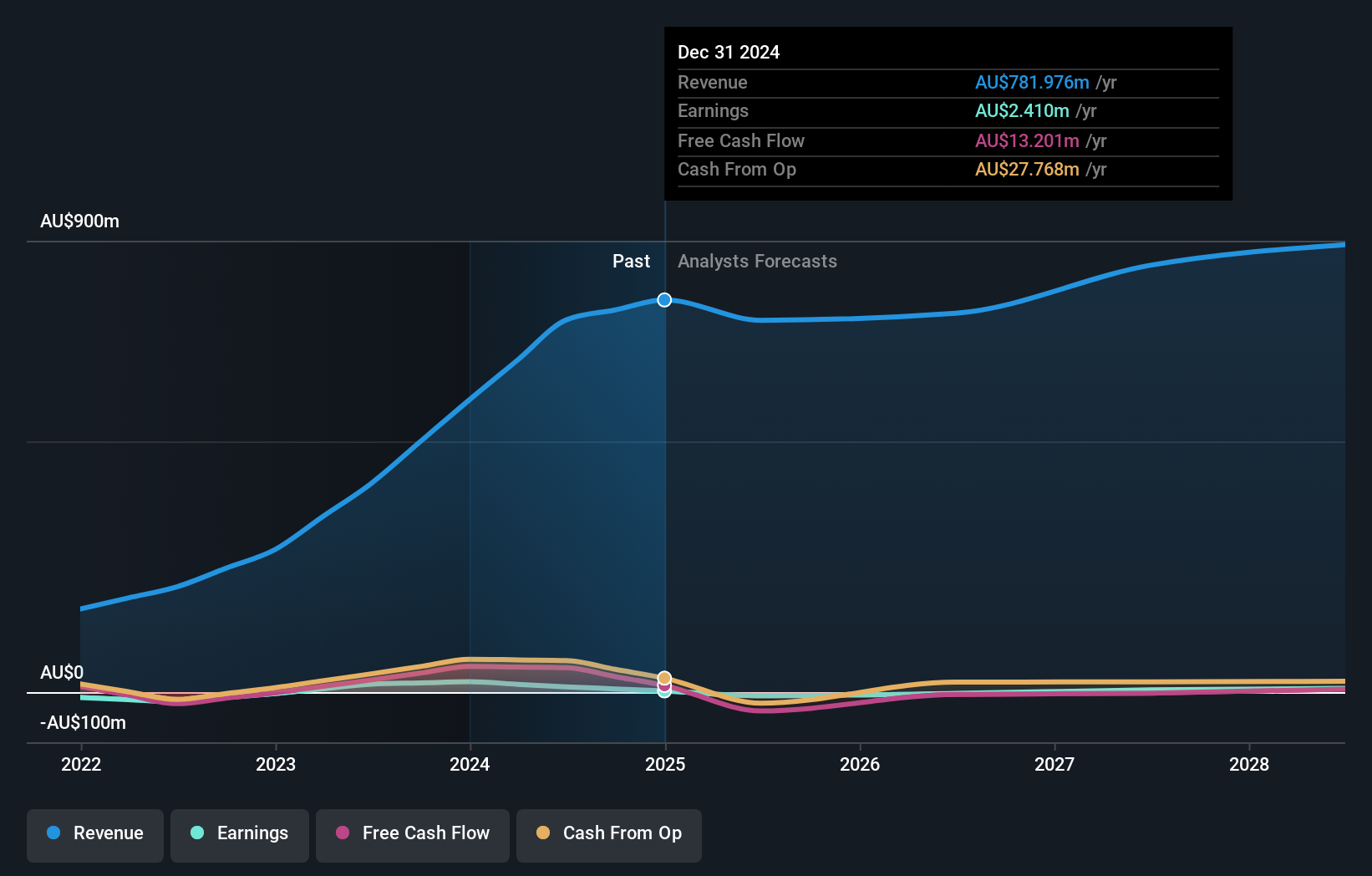

Cettire (ASX:CTT)

Simply Wall St Growth Rating: ★★★★★★

Overview: Cettire Limited operates as an online retailer of luxury goods, serving customers in Australia, the United States, and other international markets, with a market capitalization of approximately A$517.05 million.

Operations: The company generates its revenue primarily through online retail sales, totaling approximately A$582.79 million.

Insider Ownership: 28.7%

Revenue Growth Forecast: 23.6% p.a.

Cettire, an Australian growth company with high insider ownership, recently presented at the Bell Potter Emerging Leaders Conference. The company became profitable this year and is trading at A$73.3% below the estimated fair value. Despite a highly volatile share price in recent months, Cettire's earnings are expected to grow by 26.7% per year, outpacing the Australian market's 13%. Revenue growth is also projected to exceed market averages significantly at 23.6% annually.

- Click to explore a detailed breakdown of our findings in Cettire's earnings growth report.

- The valuation report we've compiled suggests that Cettire's current price could be quite moderate.

IPD Group (ASX:IPG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: IPD Group Limited, operating in Australia, specializes in the distribution of electrical equipment and has a market capitalization of approximately A$485.89 million.

Operations: The company generates revenue through its Products Division, which brought in A$215.98 million, and its Services Division, which contributed A$20.79 million.

Insider Ownership: 28.1%

Revenue Growth Forecast: 23.6% p.a.

IPD Group, an Australian growth company with significant insider ownership, is poised for robust expansion with earnings expected to increase by 25.9% annually, outstripping the market's 13%. Revenue is also set to rise significantly at 23.6% per year. Despite these strengths, concerns include a forecasted low return on equity of 19% in three years and recent shareholder dilution. The stock currently trades at A$14.6% below its fair value estimate, suggesting potential undervaluation.

- Click here and access our complete growth analysis report to understand the dynamics of IPD Group.

- The analysis detailed in our IPD Group valuation report hints at an inflated share price compared to its estimated value.

IperionX (ASX:IPX)

Simply Wall St Growth Rating: ★★★★★☆

Overview: IperionX Limited is a company focused on the exploration and development of mineral properties in the United States, with a market capitalization of approximately A$560.79 million.

Operations: The firm is primarily involved in the exploration and development of mineral properties in the United States.

Insider Ownership: 15.8%

Revenue Growth Forecast: 76.2% p.a.

IperionX, an emerging Australian company with high insider ownership, shows promising growth prospects. The firm is expected to shift into profitability within the next three years, with revenue forecasted to expand by 76.2% annually—significantly outpacing the broader market's 5.3%. Recent strategic partnerships in the U.S., focusing on advanced titanium products for defense and technology sectors, underscore its potential. However, shareholder dilution over the past year and a current valuation at 82.9% below estimated fair value present challenges.

- Get an in-depth perspective on IperionX's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that IperionX's share price might be on the expensive side.

Summing It All Up

- Delve into our full catalog of 89 Fast Growing ASX Companies With High Insider Ownership here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Cettire is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:CTT

Cettire

Engages in the online luxury goods retailing business in Australia, the United States, and internationally.

Exceptional growth potential with flawless balance sheet.