Advertisement

- Australia

- /

- Medical Equipment

- /

- ASX:NAN

IPD Group And 2 Other ASX Penny Stocks To Consider

Simply Wall St

Reviewed by Simply Wall St

As the Australian market braces for retail sales figures that could impact interest rate expectations, the ASX 200's recent rally is facing potential headwinds. In such fluctuating conditions, investors often look beyond established giants to explore opportunities in lesser-known areas like penny stocks. Although the term "penny stocks" might seem outdated, these smaller or newer companies can still offer intriguing prospects when supported by strong financials.

Top 10 Penny Stocks In Australia

| Name | Share Price | Market Cap | Financial Health Rating |

| Embark Early Education (ASX:EVO) | A$0.775 | A$142.2M | ★★★★☆☆ |

| LaserBond (ASX:LBL) | A$0.565 | A$66.23M | ★★★★★★ |

| Austin Engineering (ASX:ANG) | A$0.52 | A$322.48M | ★★★★★☆ |

| SHAPE Australia (ASX:SHA) | A$2.88 | A$238.78M | ★★★★★★ |

| Helloworld Travel (ASX:HLO) | A$2.01 | A$327.26M | ★★★★★★ |

| SKS Technologies Group (ASX:SKS) | A$1.59 | A$242.07M | ★★★★★★ |

| Vita Life Sciences (ASX:VLS) | A$1.915 | A$107.38M | ★★★★★★ |

| Big River Industries (ASX:BRI) | A$1.285 | A$109.71M | ★★★★★☆ |

| IVE Group (ASX:IGL) | A$2.08 | A$322.17M | ★★★★☆☆ |

| Servcorp (ASX:SRV) | A$4.93 | A$486.42M | ★★★★☆☆ |

Click here to see the full list of 1,050 stocks from our ASX Penny Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

IPD Group (ASX:IPG)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: IPD Group Limited is an Australian company that distributes electrical infrastructure, with a market cap of A$407.52 million.

Operations: The company generates revenue through its Products Division, contributing A$270.68 million, and its Services Division, which accounts for A$19.74 million.

Market Cap: A$407.52M

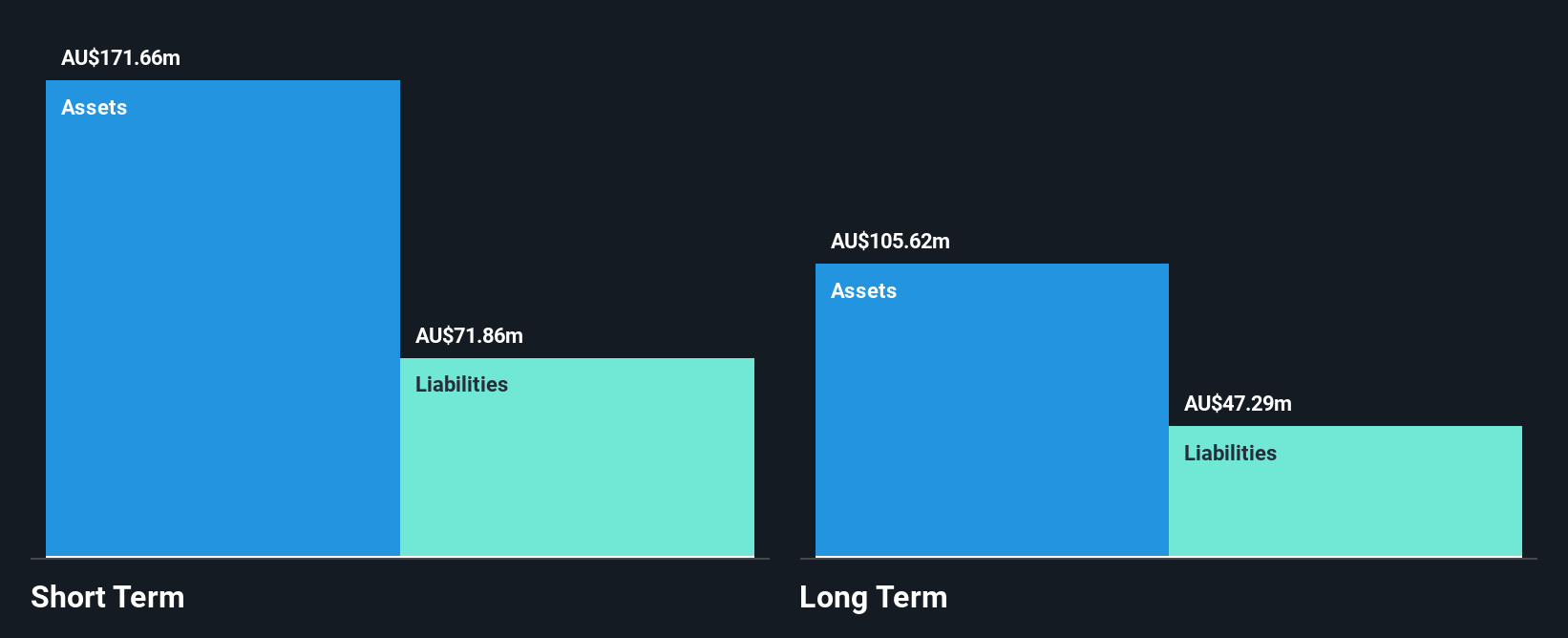

IPD Group Limited, with a market cap of A$407.52 million, has shown robust earnings growth, averaging 35.8% annually over five years and accelerating to 39.1% last year, outpacing the industry average. The company maintains high-quality earnings and its debt is well covered by operating cash flow at 75.1%. Short-term assets significantly exceed liabilities, indicating strong liquidity management. Despite trading slightly below estimated fair value, analysts expect a potential price increase of 31%. Recent guidance suggests EBIT between A$19.2 million and A$19.8 million for the half-year ending December 2024, signaling continued revenue growth prospects.

- Take a closer look at IPD Group's potential here in our financial health report.

- Assess IPD Group's future earnings estimates with our detailed growth reports.

Impact Minerals (ASX:IPT)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Impact Minerals Limited is an Australian exploration company with a market capitalization of A$36.71 million.

Operations: The company generates revenue from its mineral exploration activities, totaling A$0.12 million.

Market Cap: A$36.71M

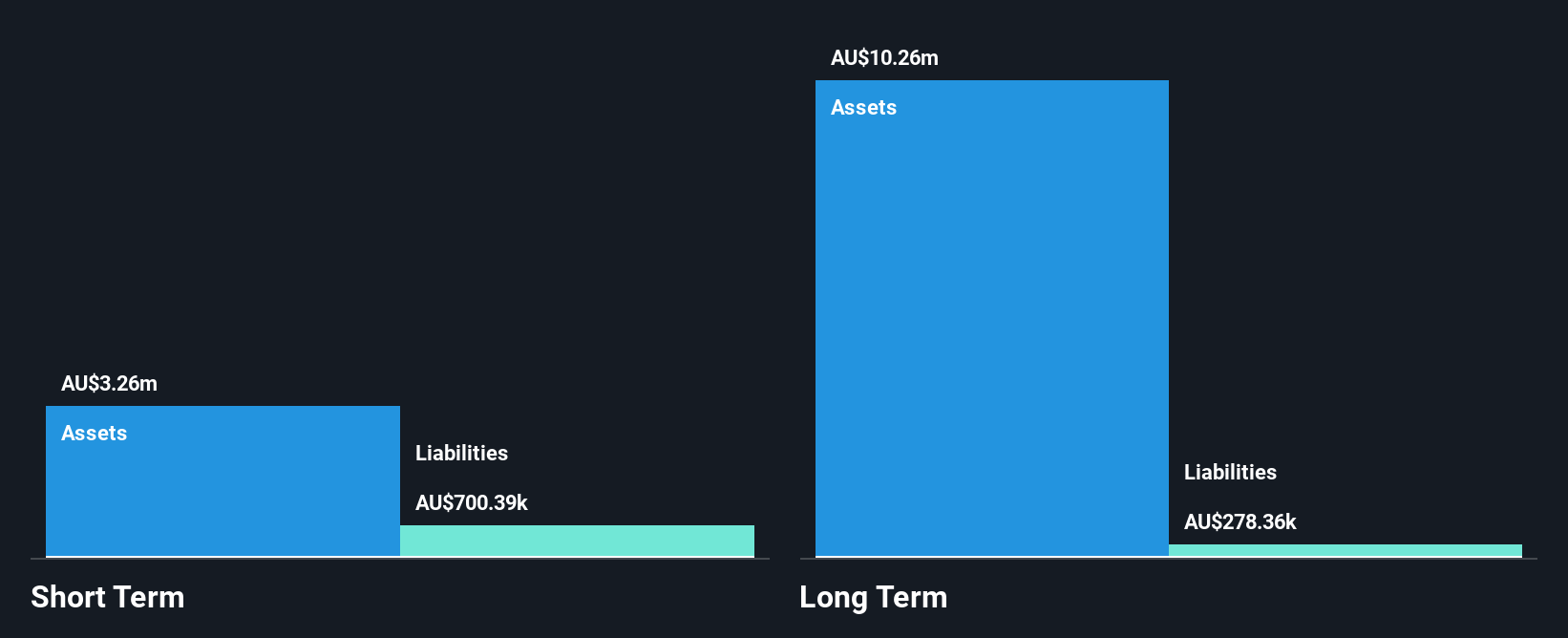

Impact Minerals Limited, with a market cap of A$36.71 million, is pre-revenue and unprofitable but has secured a A$2.87 million grant for its Lake Hope project to produce High Purity Alumina (HPA), a critical mineral. This initiative involves collaboration with CPC Engineering and Edith Cowan University to develop innovative processes with minimal environmental impact. The company aims to construct a pilot plant in 2025 as part of its research and development efforts, supported by the Federal Government's CRC-P program. Despite shareholder dilution over the past year, Impact remains debt-free with sufficient short-term assets exceeding liabilities.

- Navigate through the intricacies of Impact Minerals with our comprehensive balance sheet health report here.

- Gain insights into Impact Minerals' historical outcomes by reviewing our past performance report.

Nanosonics (ASX:NAN)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Nanosonics Limited is a global infection prevention company with a market capitalization of A$925.82 million.

Operations: The company generates revenue of A$170.01 million from its healthcare equipment segment.

Market Cap: A$925.82M

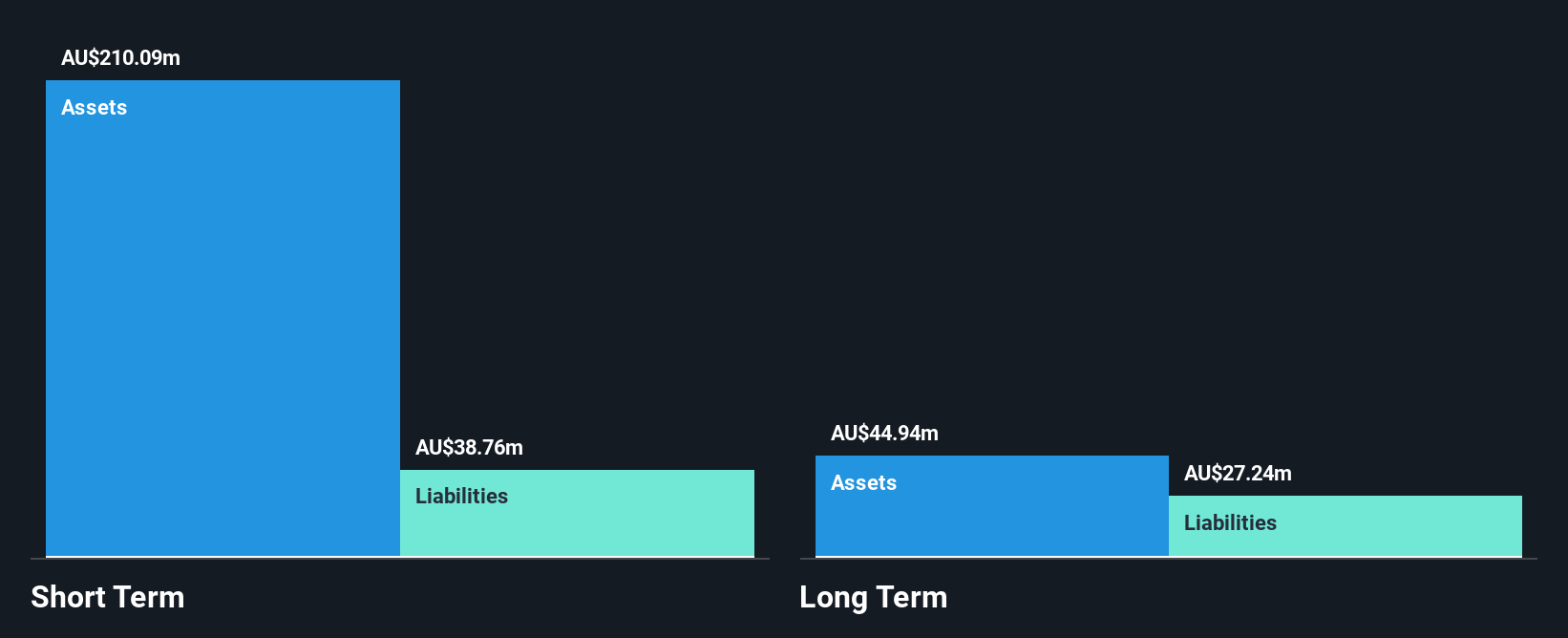

Nanosonics Limited, with a market cap of A$925.82 million, generates A$170.01 million in revenue from its healthcare equipment segment. The company maintains a stable weekly volatility of 4%, supported by strong financial health with short-term assets significantly exceeding liabilities and no debt concerns. Despite recent negative earnings growth and declining profit margins from 12% to 7.6%, Nanosonics is trading at 38.7% below estimated fair value, suggesting potential undervaluation. Management and board experience remain robust, although recent board changes may impact strategic direction as key members step down after long tenures. Earnings are forecasted to grow annually by about 23.96%.

- Dive into the specifics of Nanosonics here with our thorough balance sheet health report.

- Understand Nanosonics' earnings outlook by examining our growth report.

Key Takeaways

- Dive into all 1,050 of the ASX Penny Stocks we have identified here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nanosonics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:NAN

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor